HOCHWERTIG | 650 m² HALLE | 800 m² AUSSTELLUNG

ID: 998947DetailsGarching, repräsentatives Produktionsgebäude mit hochwertigen Büroflächen

ID: 93135Detailsca. 400 m² große, ebenerdige Lager-Produktionshalle mit Meisterbüro in Top Lage

ID: 1036679DetailsDirekt am Autobahnkreuz Ulm/Elchingen - Neubau multifunktionaler Logistik- und Produktionsflächen

ID: 994300DetailsLOGISTIK | RAMPEN | FREIFLÄCHE

ID: 1008605DetailsLager-/Logistik | Neubau | Rampen | teilbar | ebenerdig

ID: 1016255DetailsGEWERBEPARK | ERSTBEZUG | TOP-LAGE

ID: 996681DetailsBremen, ca. 1.300 m² Lager-/ Logistikfläche zu vermieten

ID: 1032273DetailsMünchen - Nord, Hallen- und Freiflächen in Bestlage zu vermieten

ID: 101077DetailsPROVISIONSFREI | GEWERBEPARK | FLEXIBEL

ID: 1000973DetailsArnsdorf | ca. 9.000 m² | Lager & Logistik | Betonrampe & ebenerdig | teilbar ab 2.000

ID: 1009874DetailsRepräsentativer Gewerbepark

ID: 1005086Detailsca. 1.350 m² große, ebenerdige Hallenfläche mit Büro

ID: 1035432DetailsPRODUKTION | LAGER | RAMPE

ID: 991522DetailsGarching, Neubau von ca. 8.000 m² Lager-,Forschungs- und Bürofläche

ID: 1030576DetailsMunich-North, warehouse and office spaces for rent

ID: 1033335DetailsMunich-North, warehouse and office spaces for rent

ID: 1024609DetailsMunich-North, warehouse and office spaces for rent

ID: 1034331DetailsMunich-North, warehouse and office spaces for rent

ID: 1002692DetailsMunich-North, warehouse and office spaces for rent

ID: 1034768DetailsMunich-North, warehouse and office spaces for rent

ID: 1034670DetailsMunich-North, warehouse and office spaces for rent

ID: 1034767DetailsMunich-North, warehouse and office spaces for rent

ID: 1025539DetailsMunich-North, warehouse and office spaces for rent

ID: 1010949DetailsMunich-North, warehouse and office spaces for rent

ID: 1032598DetailsAugsburg, site with about 2.500 sqm for rent

ID: 9040DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031912DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031769DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031836DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1028145DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030724DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030615DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1023871DetailsGladback, warehousing space for wholesale or retail for rent

ID: 95769DetailsGladback, warehousing space for wholesale or retail for rent

ID: 1013489DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1025426DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1026621DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1022435DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1023380DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1014315DetailsNeuss, approx. 1,295 sqm warehouse space in a business park for rent

ID: 997156DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1017665DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1019585Details

Do you have a question? Leave your contact details here and we will call you back!

Market report North Rhine-Westphalia full-year 2023

- About the logistics market in the economic region

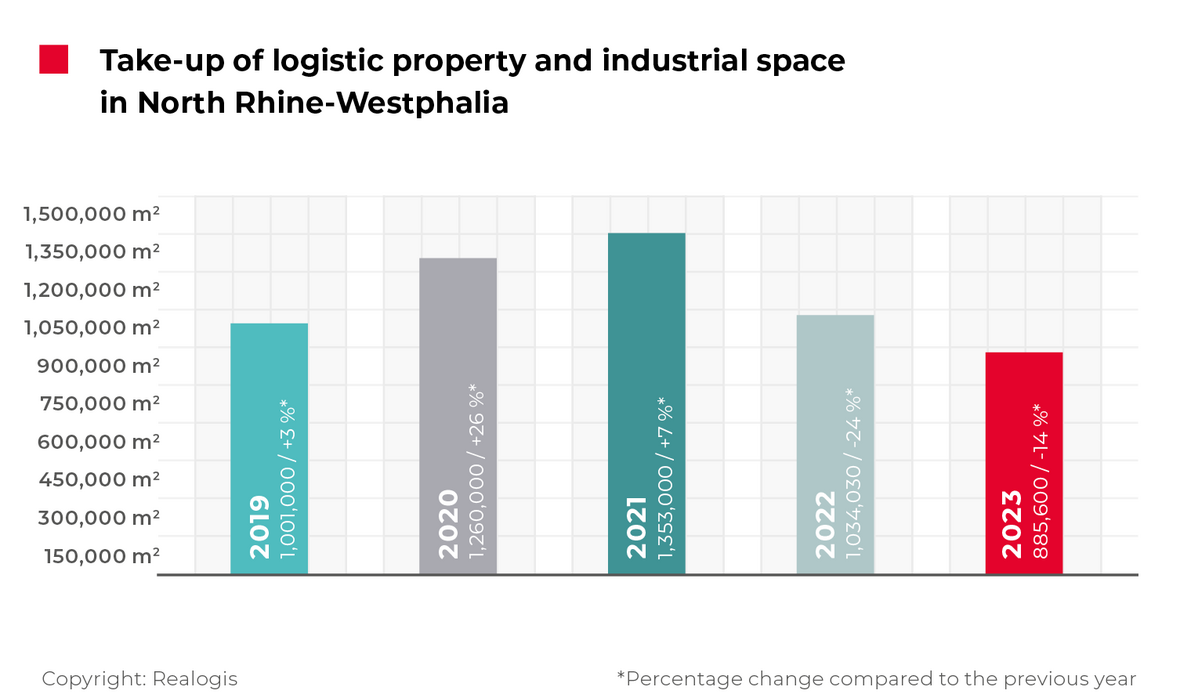

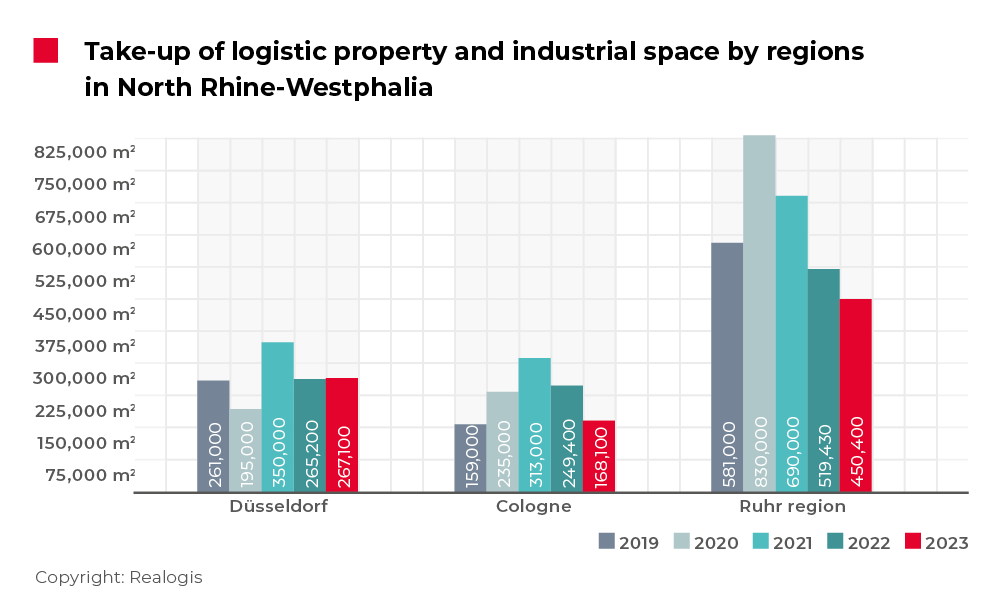

The market for rental and owner-occupied industrial and logistics properties in North Rhine-Westphalia continued the downward trend of the previous year, albeit at a slower rate. Take-up by all market participants amounted to 885,600 m² in 2023.

This is down by 14.4% compared to the previous year of 2022, which had total take-up of 1 million m² (down by 23.6% from 1.35 million m² in 2021). 2023 is also below the current five-year average of 1.1 million m² by a significant 20%.

Facts

- Slower decline in take-up

- Drop in new-build utilisation of approximately 30%

- Sub-market rankings: Ruhr area still number 1

- Sector ranking: Logistics/distribution claims half of take-up

- Large areas continue to dominate

- Prime rent in Düsseldorf increases by 15.4%

The market does not have any large-scale new-build developments – in either the speculative or the built-to-suit segment. This is also hampering the ongoing development of companies in the retail, manufacturing and logistics sectors that want to expand or consolidate in ESG-compliant properties. The last time that take-up by all market participants fell below the 1 million m² mark was in 2018 (971,000 m²). After 753,000 m² in 2017, 2023 was the second-lowest year as a whole on our records.

Decline in new-build utilisation of approximately 30%

Lettings of existing properties took the lead in 2023, accounting for take-up of 505,600 m² or 57.1% (2022: 555,688 m² or 53.7%), a year-on-year decrease of around 50,000 m² (down 9%). Rentals and owner-occupancy in new-builds accounted for just 261,800 m² or 29.6% overall (2022: 370,900 m² or 35.9%) and, down by around 110,000 m² or 29.4%, were largely responsible for what was a weak year overall on the NRW market. Brownfields accounted for 118,200 m² or 13.3% (2022: 107,440 m²), making them the only category to achieve growth with an increase of 10,760 m² or 10%.

Sub-market rankings: Ruhr area still number 1

The NRW sub-market with the highest take-up was once again the Ruhrarea with 450,440 m² or 50.9% (2022: 519,430 m² or 50.2%). One in every two square metres of take-up on the three top NRW logistics and commercial property sub-markets was located in this region in 2023. Take-up in Düsseldorf amounted to 267,100 m² or 30.2% in 2023 (2022: 265,200 m² or 25.6%), followed by the Cologne sub-market at 168,100 m² or 19%.

Big box properties accounted for more than two thirds of total take-up, i.e. 597,000 m² or 67.4% (2022: 720,000 m² or 69.6%). Properties not allocated to either big box or business parks came in second at 216,100 m² or 24.4% (2022: 234,000 m² or 22.6%). Business parks again ranked third at 72,500 m² or 8.2% (2022: 79,895 m² or 7.7%). The biggest year-on-year difference is the lack of lettings or owner-occupancy in big box properties, which declined by 123,000 m². Other properties were down by just 7,395 m² and business parks by 17,938 m².

At 853,400 m² or 96.4%, the logistics and commercial property market in NRW was once again predominantly a tenants’ market (2022: 895,130 m² or 86.6%). Owner-occupier contracts remained rare, representing just 32,200 m² or 3.6% of the market. This is also true of the 2022 comparative period, when owner-occupiers accounted for 138,900 m² or 13.4% of market share.

Sector ranking: Logistics/distribution claims half of take-up

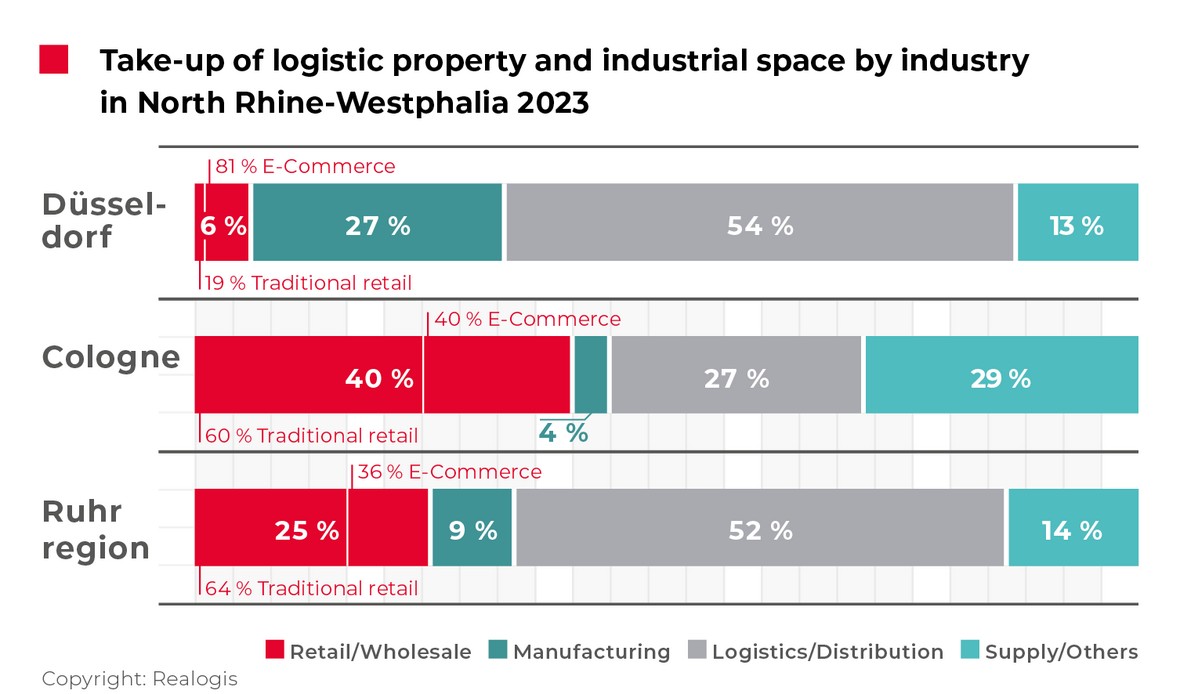

In the top sub-markets of NRW – Cologne, the Ruhr area and Düsseldorf – the logistics/distribution industry once again accounted for the lion’s share of all new leases with 420,900 m² or 47.5% (2022: 466,820 m² or 45.1%, down 10%). Out of all sectors, the retail sector saw the sharpest decline with a drop of 205,000 m² or 51.1% to 196,000 m² or 22.1%, after 400,474 m² or 38.7% in 2022.

This means that take-up was only around half of the previous year’s level, and the shortfall on the average for the past five years of 55.6% also reflects the high level of restraint in the sector. The biggest contribution to take-up within the retail category was made by traditional retail with 114,700 m² or 58.5% (2022: 177,300 m² or 44.3%, down 35%). Companies in the e-commerce sector accounted for just 81,300 m² or 41.5% (2022: 223,170 m² or 55.7%, down 64%).

In thirdplace and therefore moving up one place was the miscellaneous “Other” category at 146,200 m² or 16.5%, up from 50,610 m² or 4.9%. Virtually tripling to 95,500 m², this was the most significant increase of all sectors. Manufacturing is currently in last place at 122,500 m² or 13.8% (2022: 116,110 m² or 11.2%).

Large areas continue to dominate

The commercial and logistics property owner-occupier and rental market in NRW is still dominated by large properties. Almost 70% of take up, or 598,800 m², is accounted for by the category of 10,001 m² and above. However, this size category – as already outlined in the building classification – has seen by far the sharpest decline, falling by around 200,000 m² from 797,600 m² or 77.1% in 2022. Take-up in 2023 was around a quarter lower.

The category of larger to large spaces between 5,001 and 10,000 m² accounts for the second-largest share at 138,800 m² or 15.7%. Up from around 100,000 m² in 2022, this marks an increase of around 38,800 m² or 38%. Spaces between 3,001 and 5,000 m² are in thirdplace at 73,000 m² or 8.2% (2022: 52,000 m² or 5%). Small to medium-sized properties of between 1,000 and 3,000 m² are in fourthplace with 67,800 m² or 7.7% (2022: 61,760 m² or 6%), while micro spaces of less than 1,000 m² remain in lastplace with 7,200 m² or 0.8% (2022: 21,930 m² or 2.1%).

This might also be interesting for you:

To the market report Germany

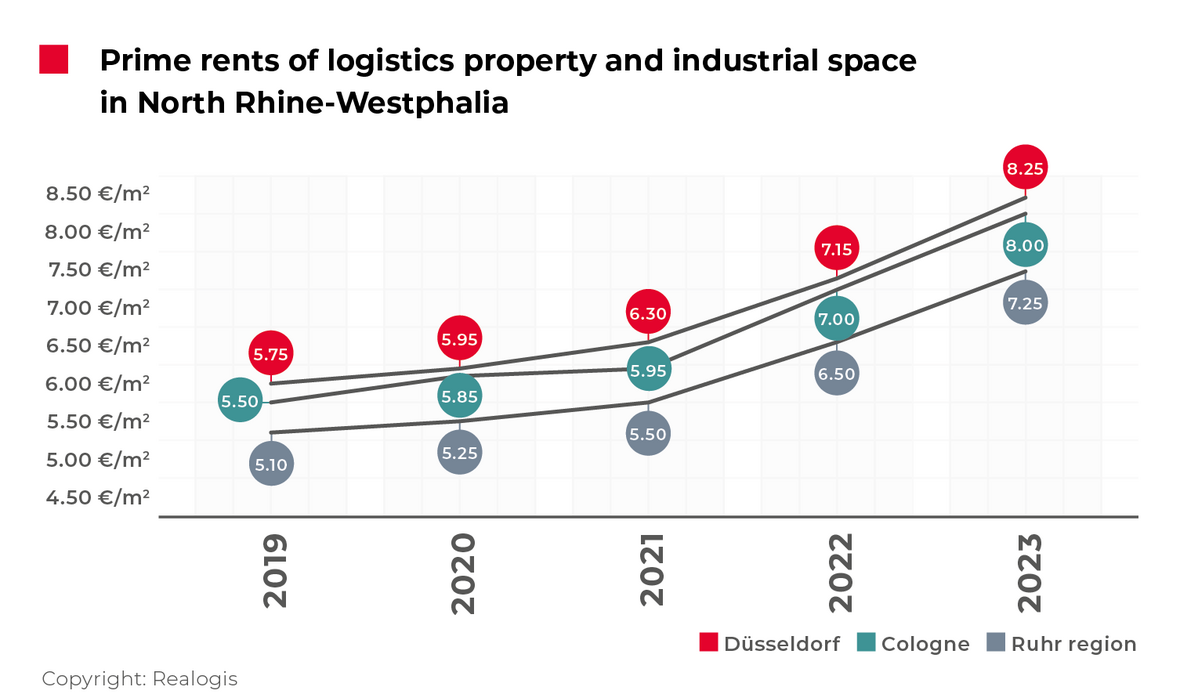

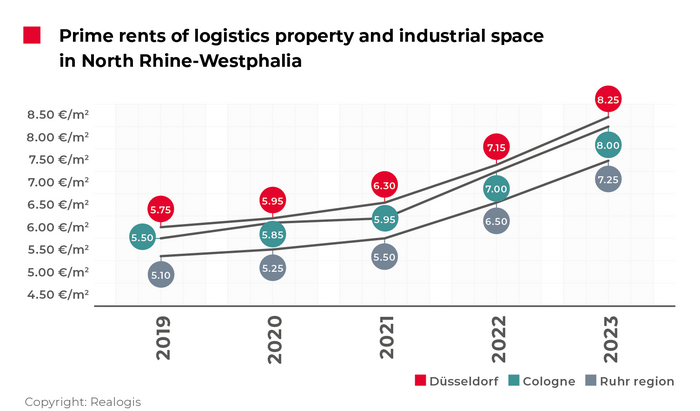

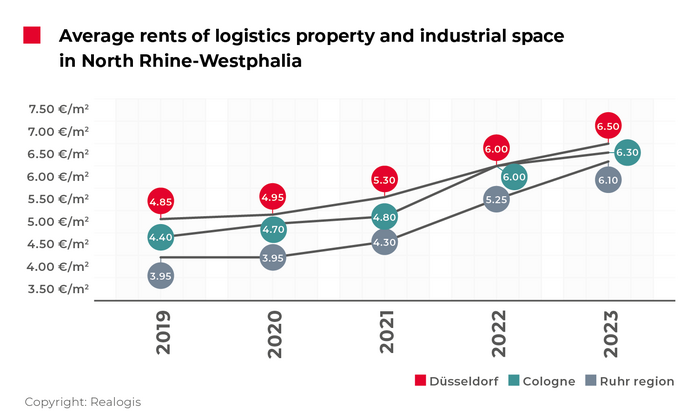

Prime rent in Düsseldorf increases by 15.4%

Düsseldorf continues to be the most expensive sub-market for prime rents, with a new high of EUR 8.25/m² (up 15.4% from EUR 7.15/m²). This is followed by Cologne at EUR 8.00/m² (up 14.3% from EUR 7.00/m²) and the Ruhr area at EUR 7.25/m² (up 11.5% from EUR 6.50/m²). The Düsseldorf market area has the highest average rent at EUR 6.50/m² (up 8.3% from EUR 6.00/m²). Close behind are Cologne at EUR 6.30/m² (up 5% from EUR 6.00/m²) and the Ruhr area at EUR 6.10/m² (up 16.2% from EUR 5.25/m²).

Market report on the letting of logistics properties and industrial spaces Düsseldorf for full year 2023

With a take-up of 267,100 m² of logistics and industrial property space for rent and owner-occupancy achieved by all market participants, the NRW submarket Düsseldorf nearly maintained its result in 2023 at the same level compared to the previous year (2022: 265,200 m²).

Only 2021 was significantly higher with a record take-up of 350,000 m². Looking at the five-year average of 267,660 m² of take-up in the Düsseldorf region, the market had a precisely average year in 2023.

Facts

- Second-best result after record take-up in 2021

- +64.2%: Brownfields see significant growth

- Building type: Big-box properties responsible for three out of four m²

- Sector ranking: Logistics/distribution with significant gains

- Areas of 5001 m² or more account for over 80%

- Prime rent increases to EUR 8.25/m²

The main contribution was made by lettings in existing properties with 148,900 m² or 55.7%, similar to the previous year's period in 2022 with 154,500 m² or 58.3%. Lease agreements or owner-occupancy of new buildings on former brownfield sites account for 118,200 m² or 44.3% and grew their results compared to 2022 with +46,200 m² or +64.2% (2022: 72,000 m² or 27.1%). We did not register any lettings or owner-occupancy of new buildings on greenfield sites last year; in 2022, they still accounted for 38,700 m² or 14.6%.

The main contribution by building type was again made by big-box properties with 206,300 m² or 77.2% (2022: 153,100 m² or 57.7%). They were the only category to record a substantial increase of 53,200 m² or 34.7%. Properties that were not allocated to either the big box or business park category remained in second place with 47,000 m² or 17.6% (2022: 66,500 m² or 25.1%). In third place in 2023 are business parks with only 13,800 m² or 5.2%. Coming from 45,600 m² or 17.2%, this is a decrease of 19,500 m² or 29%.

While big-box properties increased their importance for the Düsseldorf market by around 20 percentage points to more than three quarters of annual take-up, business parks fell by 12 percentage points and other properties by 8 percentage points. The logistics and industrial property market continues to be an almost complete lessor's market, with a share of 98.1% or 261,900 m² in 2023 (2022: 265,200 m² or 100%).

Lessors with highest take-up

Vorwerk, approx. 45,600 m² (Manufacturing), New build

GXO/Clipper, approx. 32,200 m² (Logistics/distribution), New build

HW Inox, approx. 20,000 m² (Manufacturing), Existing property

Advanced Supply Chain Group, approx. 18,580 m² (Logistics/distribution), New build

DB Schenker, approx. 15,000 m² (Logistics/distribution), Existing property

Sector ranking: Logistics/distribution with significant gains

Logistics/distribution is once again the leading sector in terms of take-up. At 143,200 m² or 53.6%, up from 103,800 m² or 39.1% in 2022, it accounts for more than half of the market's total take-up. The result also represents the most significant year-on-year increase in take-up in absolute terms, totalling 39,400 m² or +38%. Manufacturing moved up one place year-on-year to second rank with 72,800 m² or 27.3% (2022: third place with 52,500 m² or 19.8%). This means that the sector is already taking up one in four square metres of total take-up, compared to just one in five in 2022 (growth of 20,300 m² or 38.7%).

The collective category "Other" came in thirdplace with 34,400 m² or 12.9% (2022: 7,400 m² or 2.8%). Retail deals are in last place. In 2023, it plummeted by -84,800 m² or -83.5% and was only almost a fifth of the previous year's figure (2022: 101,500 m² or 38.3%). Retail is also the only sector to rank far below its own five-year average of currently 76,000 m², which was missed by a significant 78% in 2023. Within the industry, e-commerce leads with 13,600 m² or 81.4% (2022: 56,100 m² or 55.3%), ahead of traditional retail with 3,100 m² or 18.6% (2022: 45,400 m² or 44.7%). The significant drop in retail (-84,800 m²) was compensated for by the increase in demand for space from other sectors (86,700 m²), resulting in a small increase of 1,900 m².

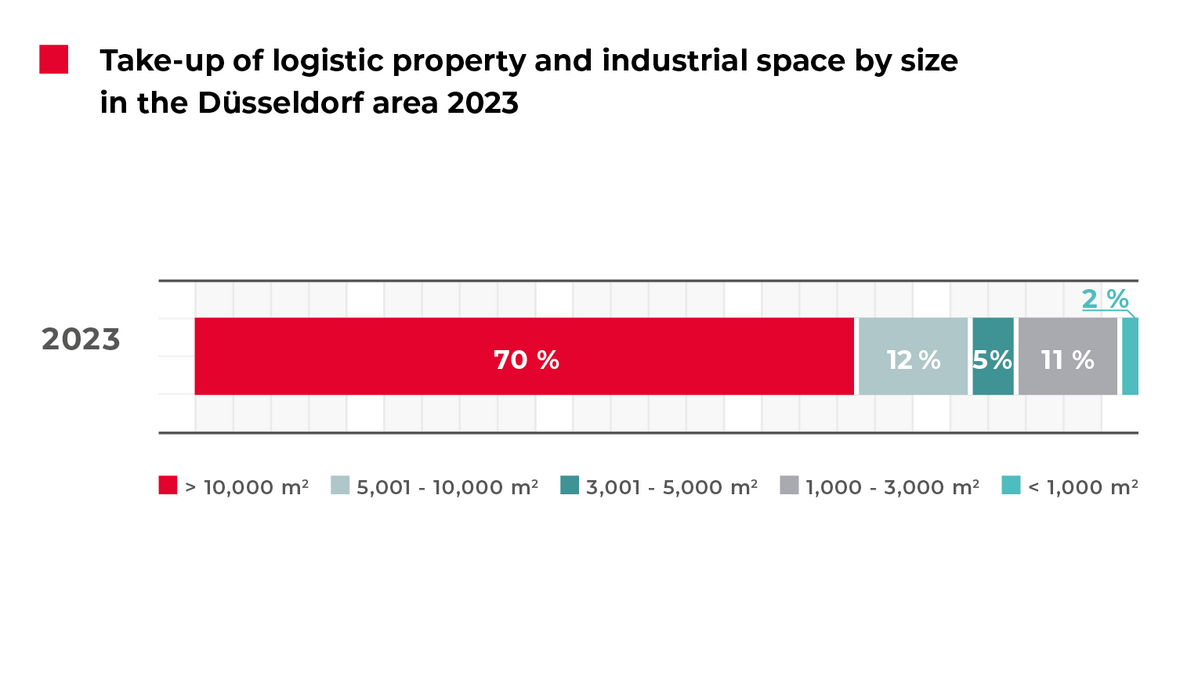

Areas of 5,001 m² or more account for over 80%

Large areas of 10,001 m² and above were dominant for the Düsseldorf market with 69.6% or 186,000 m². The leading role was maintained, coming from 167,800 m² or 63.3% in 2022. All of the top revenue generators fall into this category and, with 131,380 m², contribute around 70% of the revenue in this size class. Medium to large spaces between 5,001 and 10,000 m² occupy second place with 33,300 m² or 12.5% (2022: 22,400 m² or 8.4%).

The space category between 3,001 and 5,000 m² is in fourth place with 14,100 m² or 5.3% (2022: 28,900 m² or 10.9%). Smaller to medium-sized spaces between 1,000 and 3,001 m² rank third with 28,600 m² or 10.7% (2022: 29,500 m² or 11.1%). The smallest spaces of less than 1,000 m² are still in last place with 1.9% or 5,100 m², coming from 16,600 m² or 6.3% in 2022.

Overall, we observed a concentration on large spaces of 5,001 m² or more on the Düsseldorf market in the past year, which accounted for 82.1% or 219,300 m² of total take-up and increased by 29,100 m² in absolute terms compared to the same period of the previous year.

Prime rent rises to EUR 8.25/m² and exceeds five-year average by 23.5%

The prime rent has risen by 15.4% to a new provisional high of EUR 8.25/m², up from EUR 7.15/m² in 2022. This is the most significant increase in prime rent in the market area since we have been keeping records over the last 10 years. The five-year average of EUR 6.68/m² was exceeded by 23.5%. At 8.3%, the average rent rose less than the prime rent and also reached its provisional high of €6.50/m² at the end of 2023, up from EUR 6.00/m².

This development represents the second most significant increase in the last five years. In the previous year, the increase was 13.2% to EUR 6.00/m², up from EUR 5.30/m². The five-year average of EUR 5.52/m² was exceeded by 17.8% in 2023.

Market report on the letting of logistics properties and industrial spaces Cologne for full year 2023

The Cologne market for owner-occupied and rented industrial and logistics properties continued the negative trend of the previous year. Recording a drop of 32.6%, the total take-up of 168,100 m² achieved by all market participants in 2023 was lower than the previous year's result of 249,400 m², which was in turn around 20% lower than 2021 (2021: take-up of 313,300 m²). The five-year average, which currently stands at 224,900 m², was missed by a significant 25.3%.

Facts

- Clear downward trend in take-up confirmed

- Slump in new construction activity, no brownfield developments

- Industry rankings: retail dominates

- Size segment from 3,001 m² still in high demand

- Prime rents climb to EUR 8.00/m²

Existing properties dominate the market, accounting for 154,900 m² or 92.1%, up from 155,700 m² and 62.4% in 2022. They thus increased their share of total take-up by 29.7 percentage points.According to our analysis, the reason for the further increase in the importance of existing space can be found in the significant slump in new construction activity. With take-up of just 13,200 m² or 7.9%, the slump in rentals of space in new builds is -80,500 m² or -86% (2022: 93,700 m² or 37.6% of market activity). Brownfield developments once again played no role on the Cologne market.

In terms of building type, big-box properties accounted for 63,900 m² or 38% (2022: 163,800 m² or 65.7%), ranking first and well ahead of rentals of space in business parks in third place, which recorded figures of 40,500 m² or 24.1% (2022: 17,700 m² or 7.1%). Properties that are neither big-box properties nor business parks remained in second place with 63,700 m² or 37.9% (2022: 67,900 m² or 27.2%). While big boxes saw take-up decline by around 100,000 m² or 61% and thus experienced the most significant loss in importance of all building types year-on-year in both absolute and relative terms (-27.7 percentage points), business parks were the only category to increase in absolute terms – by 22,800 m² or 128%. In terms of users, Cologne was exclusively a lessor's market in 2023. We did not register a single contract for owner-occupancy.

Lessors with highest take-up

Centershop, approx. 34,300 m² (Traditional retail), Existing property

E-Rocket, approx. 19,500 m² (E-commerce), Existing property

Computacenter, approx. 26,500 m² (Other), Existing property

Industry rankings: Retail dominates – logistics/distribution only in third place

Retail regained the top spot for the first time since 2021, accounting for 67,500 m² or 40.2% and moving up from the second place it held in 2022 when it recorded 80,200 m² or 32.2%. With the exception of the "Other" category, all sectors saw a decline in take-up, with retail falling the least (-12,700 m² or -15.8%). Within the retail sector, traditional retail dominated with 59.7% or 40,300 m². Moving up from second place where it had recorded 33,200 m² or 41.4%, the sub-category grew by 7,100 m² and overtook e-commerce in the past full year. This sub-category accounted for 27,200 m² of accumulated take-up, or 40.3%, within the retail category (2022: 47,000 m² or 58.6%) at the end of 2023.

The collective category "Other" came in second place with 49,100 m² or 29.2% (2022: 31,300 m² or 12.6%). In third place is the logistics/distribution sector, which typically ranks first or second on the Cologne market, with 44,900 m² or 26.7%, down from 95,400 m² or 38.3%, and which thus recorded the most significant absolute decline of all sectors, falling 50,500 m² or -52.9%. The sector's five-year average of around 80,000 m² was missed by a significant 44%. Manufacturing brought up the rear with 6,600 m² or 3.9% (2022: 42,500 m² or 17%). This comparatively low level was last seen in 2016 when it stood at around 3% or 6,450 m². The sector fell 82% short of its own five-year average (36,000 m²), the largest margin of all.

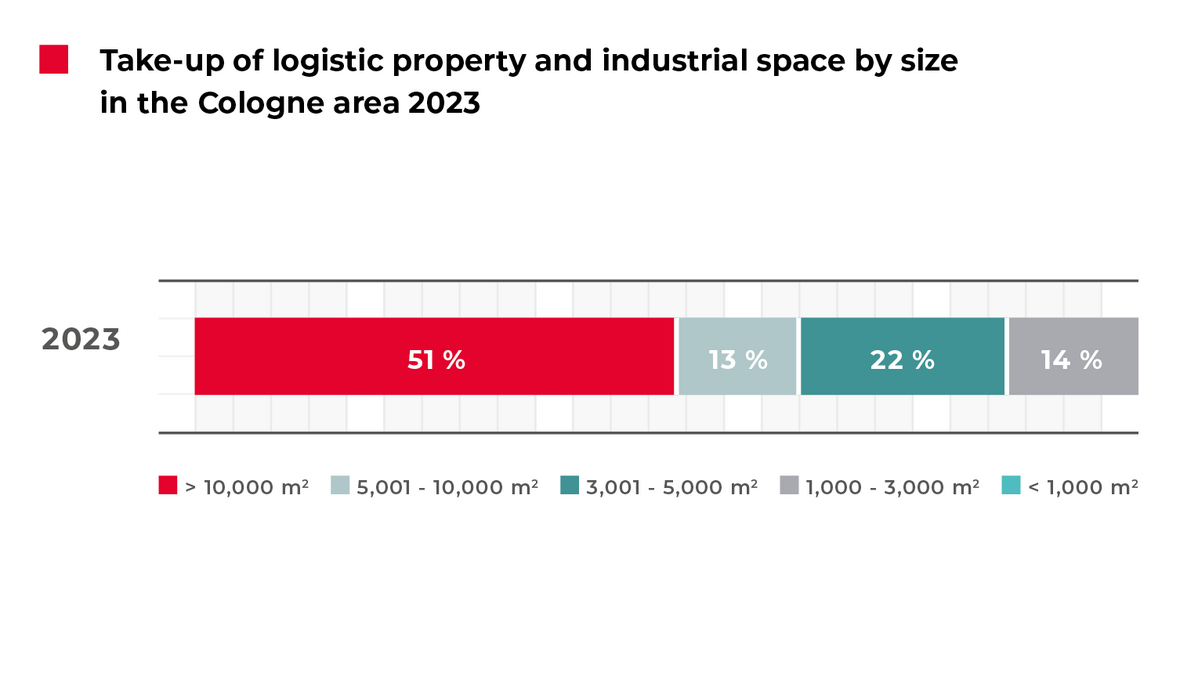

Size segment from 3,001 m² still in high demand

Just over half of take-up in 2023 was accounted for by large spaces of 10,001 m² or more. Accounting for 85,900 m² or 51.1%, the segment continues to lead the other space categories, but lost 100,100 m² or 53.8% in absolute terms and 23.5% in relative terms (2022: 186,000 m² or 74.6%).

With 21,600 m² or 12.8%, the size category between 5,001 and 10,000 m² only ranks fourth (it still occupied second place in 2022 when it totalled 36,200 m² or 14.5%). As a result, large spaces of 5,001 m² or more have lost a total of 114,700 m² of take-up over the year as a whole and currently only account for 64% of total take-up. This means that the concentration of large spaces continued to weaken in 2023.

In 2022, almost nine out of ten square metres taken up were in spaces of 5,001 m² or more, whereas the current figure is just over six out of ten. We recorded take-up of 37,500 m² or a share of 22.3% for the category of medium-sized properties between 3,001 and 5,000 m². Coming from fourth place, this category has risen to second place with the largest absolute increase of all size categories – 25,200 m² or +200% – and thus tripling take-up.

Small to medium-sized spaces of between 1,000 and 3,000 m² accounted for the third highest take-up of space at 23,100 m² or 13.7% (2022: 13,700 m² or 5.5%). No deals were registered for the smallest spaces of less than 1,000 m².

Prime rents climb to EUR 8.00/m²

In the logistics property segment, the Cologne market has seen the second most significant increase in rents in the last five years, with prime rents rising by a whopping 14.3% to EUR 8.00/m² by the end of 2023. Up from EUR 7.00/m² at the end of 2022, this figure represents the highest value to date. The rate of price increases in the previous year was even higher, however, at 17.6 % after starting out at EUR 5.95/m². The current five-year average of EUR 6.46/m² was exceeded by 24% in 2023.

Average rents rose by 5%, thus seeing a more moderate increase than prime rents, and recorded a new high to date of EUR 6.30/m², up from EUR 6.00/m². The five-year average of EUR 6.68/m² was exceeded by 20%.

Market report on the letting of logistics properties and industrial spaces Ruhr region for full year 2023

The market for rental and owner-occupied industrial and logistics properties in the Ruhr area continued the negative trend of the previous year, albeit at a slower rate. According to our analysis, take-up of 450,400 m² was achieved by all market participants as a whole in 2023. This represents a decrease of 13.3% year-on-year and of 69,030 m² to 519,430 m² in absolute terms (2022: drop of 24.7% or 170,570 m² in absolute terms).

Facts

- Down 13.3%: Decline in take-up continues

- New builds continue success with leases signed for 250,000 m²

- No brownfield developments

- Bix box category responsible for approximately three quarters of all new deals

- Sector ranking: Logistics/distribution accounts for more than half

- Take-up of large spaces down by more than 26%

- Significant increase in average rents

The past year ranks last in a five-year comparison. In a 10-year comparison, only the 2015 result of 257,000 m² and the 2014 result of 210,000 m² were lower. The long-term average of 614,166 m² was missed by a significant 26.7%. One piece of good news from the Ruhr area is that deals for new builds were at a similarly high level compared to the previous year and, despite the general reluctance on the part of project developers, were even up year-on-year in absolute terms. Since it was founded in 2007, the consulting firm has served the top three logistics markets in NRW, including the Ruhr area, with a team of 11 based in Düsseldorf. In 2023, new buildings contributed 248,600 m² or a share of 55.2% (2022: 238,502 m² or 45.9%), achieving absolute year-on-year growth of 10,098 m² or 4%.

In second place are lettings in existing properties, which accounted for 201,800 m² or 44.8%, down from 245,488 m² or 47.3% in 2022, which marks the most significant absolute decline across all categories (new build, existing property, brownfield) with a drop of 43,688 m² or 18%. Brownfields played no role in the past year as a whole after achieving 35,440 m² or 6.8% in the previous year. Deals in big box properties dominated the market in 2023, accounting for 72.6% of the market at 326,800 m² (2022: 403,197 m² or 77.6%). Although they were the only category to experience an absolute decline, they still held on to the top position with 76,397 m² (down 18.9%).Deals in properties that are neither big boxes nor business parks are in second place, accounting for 105,400 m² or 23.4% (2022: 99,638 m² or 19.2%) and thus achieving a slight increase (up 5,762 m² or 5.8%).

In last place are deals in business parks, which continue to play the least important role in the Ruhr area with a contribution of 18,200 m² or 4%, up from 16,595 m² or 3.2% (slight growth of 1,605 m² or 9.7%). The Ruhr area continues to be predominantly a lessor’s market, with 423,400 m² or 94% of take-up almost entirely accounted for by leases (2022: 419,430 m² or 80.7%). At 27,000 m² or 6%, owner-occupier leases fell by 73,000 m² or 73% in absolute terms and by 13.3 percentage points in relative terms compared to the previous year, when they still accounted for 100,000 m² or 19.3%.

Lessors with highest take-up

Thalia, approx. 56,000 m² (Traditional retail), New building

Yusen Logistics, approx. 50,000 m² (Logistics/distribution), New build

Pfenning Logistics, approx. 30,080 m² (Logistics/distribution), New build

Rhenus, approx. 30,000 m² (Logistics/distribution), New build

Euziel International, approx. 24,500 m² (E-commerce), Existing property

Sector ranking: Logistics/distribution accounts for more than half

Logistics/distribution was again the strongest sector in 2023. Contributing 232,800 m² or 51.7%, this sector accounts for more than half of take-up in the Ruhr area (2022: 267,623 m² or 51.5%), meaning that its importance remains at the same high level despite a decline of around 35,000 m² or 13% in absolute terms.

Retail takes second place with 111,800 m² or 24.8%, occupying the same position in the rankings as in the previous year when it contributed 218,774 m² or 42.1%. With a delta of 106,974 m² or 48.9%, the retail sector accounted for only slightly more than half of the previous year’s take-up and lost the most space of all sectors in absolute terms. The shortfall of 59.7% on the retail sector’s five-year average of 277,000 m² was the largest across all sectors.

Within the sector, the sub-categories of traditional retail and e-commerce swapped places in the Ruhr area in the year-on-year comparison. In 2023, traditional retail led the way with 71,300 m² or 63.8% (2022: 98,702 m² or 45.1%). E-commerce achieved take-up of only 40,500 m² or 36.2% (2022: 120,000 m² or 54.9%). The delta here is around 80,000 m² or 66.3%, meaning that the result constitutes only a third of the previous year’s take-up.

In third place is the miscellaneous “Other” category with a contribution of 62,700 m² or 13.9% (2022: 11,916 m² or 2.3%) and the largest growth of all the sectors in absolute terms with an increase of 50,784 m² or 426% (corresponding to a more than five-fold increase). After occupying third place in 2022, manufacturing brings up the rear, accounting for 43,100 m² or 9.6%, but can boast absolute growth of 21,983 m² or 104.1%, up from 21,117 m² or 4.1%.

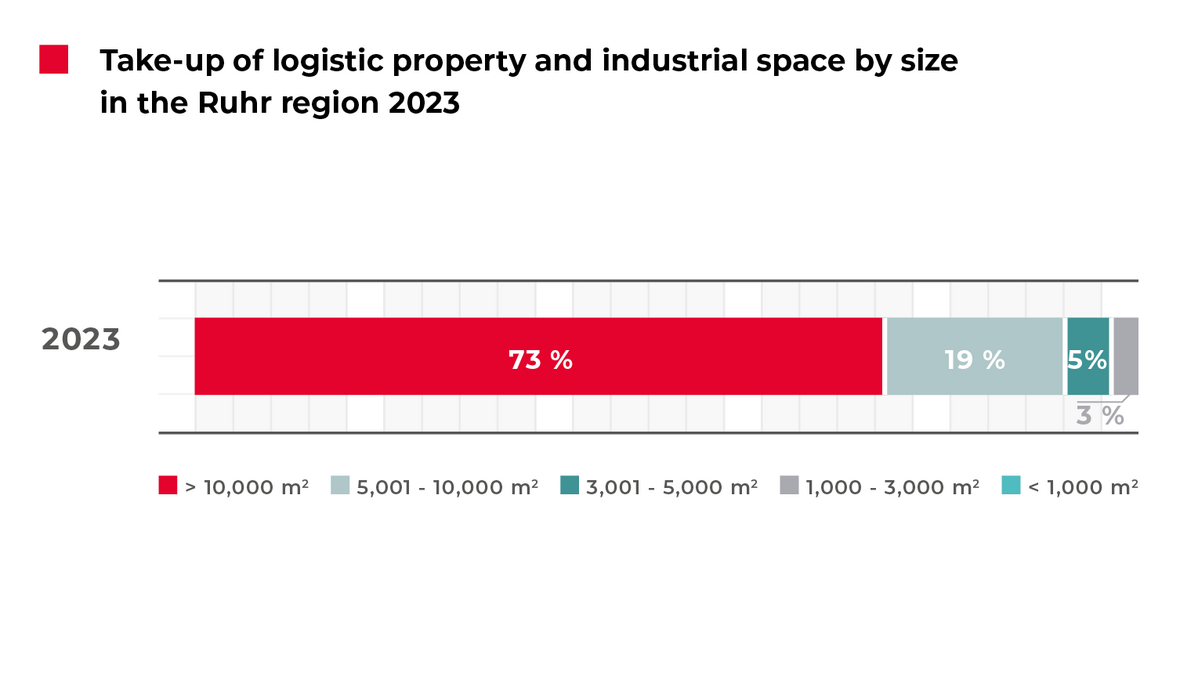

Take-up of large spaces down by more than 26%

In 2023, the Ruhr area continued to be dominated by new leases for large spaces of 10,001 m² or more, which accounted for 326,900 m² or almost three out of every four square metres of take up, after 443,836 m² or 85.4% in the previous year. Despite their leading role, large spaces lost the most take-up out of all categories. The year-on-year decline was 116,936 m² or 26.3%. The size category between 5,001 and 10,000 m² accounted for 83,900 m² or 18.6%, once again putting it in secondplace.

Coming from 41,978 m² or 8.1%, this development marks a significant absolute increase of around 42,000 m², which is double the previous year’s figure. The category of medium-sized space between 3,001 and 5,000 m² is in third place with take-up of 21,400 m² or 4.8% (2022: 10,926 m² or 2.1%). Smaller to medium-sized spaces between 1,000 and 3,000 m² accounted for 16,100 m² or 3.6% of take-up (2022: 18,560 m² or also 3.6%). Small areas of less than 1,000 m² contributed only 2,100 m², equivalent to a share of 0.5%.

Significant increase in average rents

The rise in prime rents continued with an increase of 11.5% to EUR 7.25/m² compared to EUR 6.50/m² at the end of 2022. The five-year average of EUR 5.92/m² was thus exceeded by 22.5%.

Average rents also rose with a much more dynamic increase than in prime rents but of 16.2% to EUR 6.10/m², up from EUR 5.25/m² in 2022. The five-year average of EUR 4.71/m² was exceeded by 29.5%.

To the rent price maps:

Order the complete market report as PDF