HOCHWERTIG | 650 m² HALLE | 800 m² AUSSTELLUNG

ID: 998947DetailsGarching, repräsentatives Produktionsgebäude mit hochwertigen Büroflächen

ID: 93135Detailsca. 400 m² große, ebenerdige Lager-Produktionshalle mit Meisterbüro in Top Lage

ID: 1036679DetailsDirekt am Autobahnkreuz Ulm/Elchingen - Neubau multifunktionaler Logistik- und Produktionsflächen

ID: 994300DetailsLOGISTIK | RAMPEN | FREIFLÄCHE

ID: 1008605DetailsLager-/Logistik | Neubau | Rampen | teilbar | ebenerdig

ID: 1016255DetailsGEWERBEPARK | ERSTBEZUG | TOP-LAGE

ID: 996681DetailsBremen, ca. 1.300 m² Lager-/ Logistikfläche zu vermieten

ID: 1032273DetailsMünchen - Nord, Hallen- und Freiflächen in Bestlage zu vermieten

ID: 101077DetailsPROVISIONSFREI | GEWERBEPARK | FLEXIBEL

ID: 1000973DetailsArnsdorf | ca. 9.000 m² | Lager & Logistik | Betonrampe & ebenerdig | teilbar ab 2.000

ID: 1009874DetailsRepräsentativer Gewerbepark

ID: 1005086Detailsca. 1.350 m² große, ebenerdige Hallenfläche mit Büro

ID: 1035432DetailsPRODUKTION | LAGER | RAMPE

ID: 991522DetailsGarching, Neubau von ca. 8.000 m² Lager-,Forschungs- und Bürofläche

ID: 1030576DetailsMunich-North, warehouse and office spaces for rent

ID: 1033335DetailsMunich-North, warehouse and office spaces for rent

ID: 1024609DetailsMunich-North, warehouse and office spaces for rent

ID: 1034331DetailsMunich-North, warehouse and office spaces for rent

ID: 1002692DetailsMunich-North, warehouse and office spaces for rent

ID: 1034768DetailsMunich-North, warehouse and office spaces for rent

ID: 1034670DetailsMunich-North, warehouse and office spaces for rent

ID: 1034767DetailsMunich-North, warehouse and office spaces for rent

ID: 1025539DetailsMunich-North, warehouse and office spaces for rent

ID: 1010949DetailsMunich-North, warehouse and office spaces for rent

ID: 1032598DetailsAugsburg, site with about 2.500 sqm for rent

ID: 9040DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031912DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031769DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031836DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1028145DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030724DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030615DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1023871DetailsGladback, warehousing space for wholesale or retail for rent

ID: 95769DetailsGladback, warehousing space for wholesale or retail for rent

ID: 1013489DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1025426DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1026621DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1022435DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1023380DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1014315DetailsNeuss, approx. 1,295 sqm warehouse space in a business park for rent

ID: 997156DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1017665DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1019585Details

Do you have a question? Leave your contact details here and we will call you back!

Market report Frankfurt full-year 2023

- About the logistics market in the economic region

Take-up of warehouse, logistics and industrial space in the greater Frankfurt am Main area in 2023 was up significantly on the previous year's weak result and is once again close to the five-year average for the full year. According to our market report, 458,300 m² of rental and owner-occupied space was taken up by all market participants in 2023. This equates to significant growth of around 140,000 m² or 44.3% compared with the same period of the previous year (2022: 317,700 m²). The latest figure is just 3.6% short of the current five-year average of 475,600 m².

Facts

- Take-up increases by 44.3% YOY

- Rhine-Main South and East sub-markets account for almost 90%

- Sector ranking: Logistics/distribution in first place again

- Further concentration on large spaces of 5,001 m² or more

- Record growth in prime rents

To put this into perspective, the record years of 2020 and 2021 were more robust with total annual take-up of 492,300 m² and 655,700 m² respectively, while 2019 and 2022 were very modest at 454,000 m² and 317,700 m² respectively.

Recorded for the first time: Subleases make a significant contribution

At 56,700 m², subleases account for around 12% of the current total annual take-up. Without this, the annual result would have been much weaker at 401,600 m.² As in the same period of the previous year, the majority of transactions involved existing properties. In 2023, existing properties accounted for four out of every five square metres of take-up on the Frankfurt rental and owner-occupied market, or 366,700 m². Compared with 238,800 m² in 2022, this is an increase of 127,900 m² or 54%. By contrast, lettings of new builds accounted for 17.6% or 80,600 m², which represents an absolute increase of 27,500 m² or 51.8%. Brownfield sites, i.e. developed derelict land, halved with a delta of 14,800 m² and now account for 11,000 m² (2022: 25,800m², -57.4%).

Big box properties provide the largest share of total take-up

Deals involving big box properties totalled 211,900 m², accounting for the largest share of total take-up at 46.2% after this category took second place with 98,700 m² or 31.1% in the previous year. Of all three space categories, they saw the most significant growth in absolute terms at +113,200 m² or +46.2% and were the only category to increase their share of take-up (+15.2 percentage points). All of the five top deals were concluded in big box logistics properties. Business parks accounted for 139,400 m² or 30.4%. Compared with 130,300 m² or 41% in 2022, this represents a slight increase of 9,100 m² in absolute terms. At 10.6 percentage points, however, this category saw the biggest decrease in its share of the Frankfurt market. Space not allocated to either the big box or business park categories increased by 18,300 m² or 20.6% to 107,000 m² or 23.3%.

Top deals

Automotive company, Rhine-Main East, approx. 23,000 m² (Existing property), Manufacturing

Dealer Tire, Rhine-Main South, approx. 22,700 m²(Existing property), Retail

Mercedes-Benz Group, Rhine-Main South, approx. 21,000 m² (Existing property), Manufacturing

Nagel Group, Rhine-Main South, approx. 18,000 m² (Existing property), Logistics

Müller-Lila Logistik, Rhine-Main South, approx. 16,580 m² (Existing property), Logistics

Rhine-Main South and Rhine-Main East sub-markets account for almost 90% of all newly occupied space

Properties in the Rhine-Main South region remained the most sought-after with take-up totalling 274,000 m², which corresponds to a share of 59.9%. This sub-market therefore accounts for more than half of all square metres let, an increase of 62.4% or +105,500 m² compared to the same period of the previous year. The Rhine-Main South region thus achieved the strongest absolute growth among all the sub-markets, and is also the only market area that is above its long-term average. The five-year average for take-up in Rhine-Main South is 232,533 m², representing an increase of +18.1%.

Almost all of the top deals – four out of every five – were conducted in the Rhine-Main-South region. Together, they make up around 78,300 m² or 28.5% of take-up in the region. The breakdown is as follows: Dealer Tire with 22,700 m², Daimler/Mercedes-Benz with 21,000 m², Nagel Group with 18,000 m² and Müller-Lila Logistik with 16,580 m².

At 129,000 m² or 28.1%, the Rhine-Main East market area again posted the second-highest take-up (2022: 76,800 m² or 24.2%). In absolute terms, this corresponds to growth of 52,200 m² or a significant increase of 68%. The top deal for 23,000 m² by a company from the automotive sector contributed 17.8% of take-up in the sub-market. The two sub-markets of Rhine-Main Eastand Southcontinue to dominate and are expanding their leading role. While these two sub-markets accounted for 77.4% or 246,000 m² in 2022, this figure rose to 88.1% or 403,700 m² by the end of 2023.

This leaves just 11.9% or 54,600 m² for the other sub-markets. Rhine-Main Northranks third in terms of take-up in the sub-markets with 17,700 m² or 3.9% (FY 2022: 15,700 m² or 4.9%). It is followed by Mainz/Wiesbaden with 15,100 m² or 3.3% (FY 2022: 24,500 m² or 7.7%), Rhine-Main West with 14,100 m² or 3.1% (FY 2022: 11,300 m² or 3.6%) and the city of Frankfurt with 7,700 m² or 1.7% (FY 2022: 20,200 m² or 6.4%).

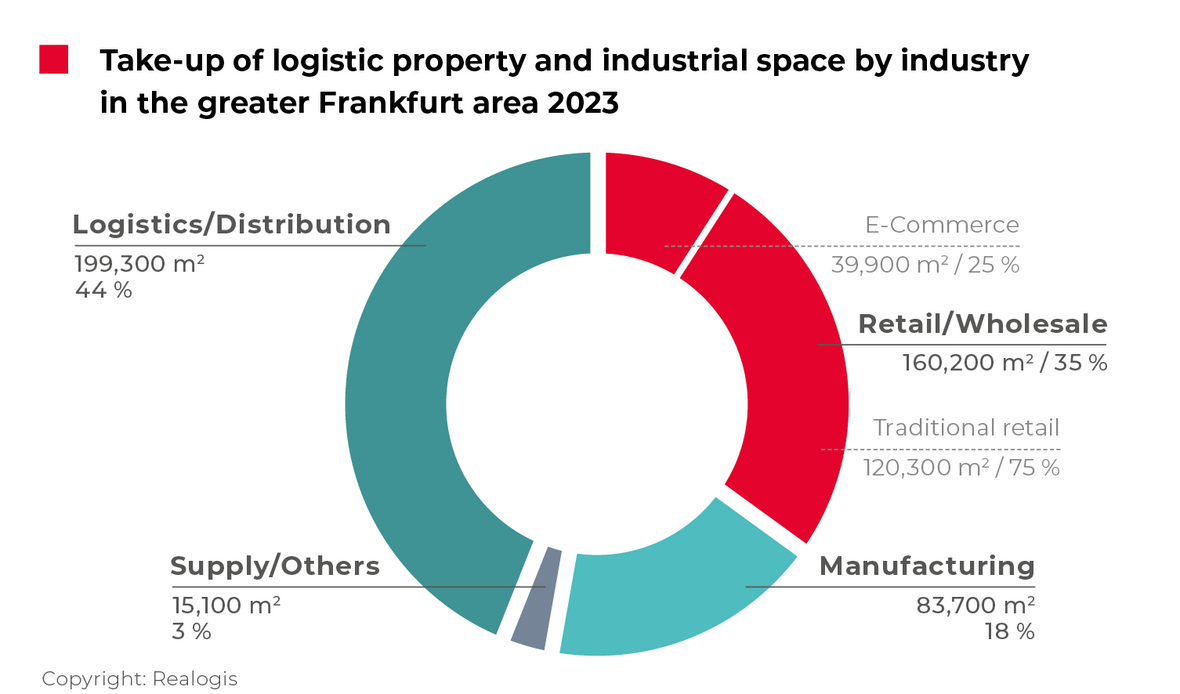

Industry ranking: Logistics/distribution back in first place since 2021

As it did in 2021 and 2022, logistics/distribution led the way in 2023 with 199,300 m² or 43.5%, compared with 152,700 m² or 48.1% in the previous year. In absolute terms, this represents an increase of 46,600 m² (+30.5%). However, the relative share of the logistics/distribution sector for the Frankfurt market is declining slightly: from 50% in 2021 (or 327,800 m²) to 48% in 2022 and currently 43.5%.

With the Nagel Group (18,000 m²) and Müller-Lila Logistik (16,580 m²), two of the top deals came from this sector, contributing 34,580 m² or 17.4% of the sector's total take-up. Retail remains in second place with 160,200 m² or 35% (FY 2022: 110,000 m² or 34.6%). In absolute terms, there has been a significant increase of 50,200 m² or 45.6% in this sector, but its relative share remains almost unchanged. Retail last topped the podium in 2020 with 47.8% or 235,200 m².

Within the sector, traditional retail led the way with a share of 75.1% or 120,300 m² (FY 2022: 99,500 m² or 90.5%). Lettings by e-commerce companies totalled 39,900 m² or 24.9% (FY: 10,500 m² or 9.5%, corresponding to near-fourfold growth of 29,400 m²). With Dealer Tire's top deal for 22,700 m², the second-largest letting of the year was in the retail sector, contributing 14.2% of take-up.

Manufacturing climbed to third place with 83,700 m² or 18.3% and posted the strongest year-on-year growth of all sectors in absolute terms at +68,300 m². This is more than five times the prior-year figure of 15,400 m² (+443%).

As a result, the sector also recorded the highest increase in share at +13.4 percentage points (from 4.8% in FY 2022 to the current figure of 18.3%).

The largest and third-largest deals of the year – by a company from the automotive sector (23,000 m²) and the Mercedes-Benz Group (21,000 m²) – were in the manufacturing sector and contributed a combined 44,000 m² or 52.6% of the sector's take-up.

The "Other" category took last place with 15,100 m² or 3.3% (FY 2022: 39,600 m² or 12.5%).

Further concentration on large spaces of 5,001 m² or more

At 180,000 m², 39.3% of new deals were concluded in the segment of large spaces of 10,001 m² or more. This category already took first place in 2022 with 98,700 m² and almost doubled its take-up in 2023 (+82.4% or +81,300 m²), while its share of total take-up increased by 8.2 percentage points from 31.1% to 39.3%. At 116,900 m² or 25.5% (FY 2022: 41,200 m² or 13%), spaces between 5,001 and 10,000 m² recorded the second-strongest absolute growth of 75,700 m², meaning that take-up almost tripled (+183.7%).

This might also be interesting for you:

To the market report Germany

Medium-sized to large spaces between 3,001 and 5,000 m² move down one place to fourth with 52,800 m² or 11.5%, having previously totalled 63,500 m² or 20%.

Small to medium-sized spaces between 1,000 and 3,000 m² also move down one position and are currently in third place with 100,700 m² or 22% (FY 2022: 93,700 m² or 29.5%). The smallest spaces of less than 1,000 m² are still in last place, accounting for 7,900 m² or 1.7% (FY 2022: 20,600 m² or 6.5%).

Compared with the previous year, the concentration on large spaces of 5,001 m² or more is intensifying. The share attributable to these properties was 64.8% or 296,900 m² in 2023 compared to 44% or just 139,900 m² in the previous year.

Record growth in prime rents

Prime rents rose by EUR 0.60/m² or 8.2% year-on-year from EUR 7.30/m² in 2022 to EUR 7.90/m² at the end of 2023, their highest level to date. This marks the highest rental growth in both percentage and absolute terms since we began keeping records. Previously, the highest rate of increase was observed in 2019 at 7.7% (from EUR 6.50/m² in 2018 to EUR 7.00/m², or EUR +0.50/m²). Prime rents are 8.8% above the five-year average of EUR 7.26/m².

To the rent price maps:

Order the complete market report as PDF