HOCHWERTIG | 650 m² HALLE | 800 m² AUSSTELLUNG

ID: 998947DetailsGarching, repräsentatives Produktionsgebäude mit hochwertigen Büroflächen

ID: 93135Detailsca. 400 m² große, ebenerdige Lager-Produktionshalle mit Meisterbüro in Top Lage

ID: 1036679DetailsDirekt am Autobahnkreuz Ulm/Elchingen - Neubau multifunktionaler Logistik- und Produktionsflächen

ID: 994300DetailsLOGISTIK | RAMPEN | FREIFLÄCHE

ID: 1008605DetailsLager-/Logistik | Neubau | Rampen | teilbar | ebenerdig

ID: 1016255DetailsGEWERBEPARK | ERSTBEZUG | TOP-LAGE

ID: 996681DetailsBremen, ca. 1.300 m² Lager-/ Logistikfläche zu vermieten

ID: 1032273DetailsMünchen - Nord, Hallen- und Freiflächen in Bestlage zu vermieten

ID: 101077DetailsPROVISIONSFREI | GEWERBEPARK | FLEXIBEL

ID: 1000973DetailsArnsdorf | ca. 9.000 m² | Lager & Logistik | Betonrampe & ebenerdig | teilbar ab 2.000

ID: 1009874DetailsRepräsentativer Gewerbepark

ID: 1005086Detailsca. 1.350 m² große, ebenerdige Hallenfläche mit Büro

ID: 1035432DetailsPRODUKTION | LAGER | RAMPE

ID: 991522DetailsGarching, Neubau von ca. 8.000 m² Lager-,Forschungs- und Bürofläche

ID: 1030576DetailsMunich-North, warehouse and office spaces for rent

ID: 1033335DetailsMunich-North, warehouse and office spaces for rent

ID: 1024609DetailsMunich-North, warehouse and office spaces for rent

ID: 1034331DetailsMunich-North, warehouse and office spaces for rent

ID: 1002692DetailsMunich-North, warehouse and office spaces for rent

ID: 1034768DetailsMunich-North, warehouse and office spaces for rent

ID: 1034670DetailsMunich-North, warehouse and office spaces for rent

ID: 1034767DetailsMunich-North, warehouse and office spaces for rent

ID: 1025539DetailsMunich-North, warehouse and office spaces for rent

ID: 1010949DetailsMunich-North, warehouse and office spaces for rent

ID: 1032598DetailsAugsburg, site with about 2.500 sqm for rent

ID: 9040DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031912DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031769DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031836DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1028145DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030724DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030615DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1023871DetailsGladback, warehousing space for wholesale or retail for rent

ID: 95769DetailsGladback, warehousing space for wholesale or retail for rent

ID: 1013489DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1025426DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1026621DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1022435DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1023380DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1014315DetailsNeuss, approx. 1,295 sqm warehouse space in a business park for rent

ID: 997156DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1017665DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1019585Details

Do you have a question? Leave your contact details here and we will call you back!

Market report Berlin full-year 2023

- About the logistics market in the economic region

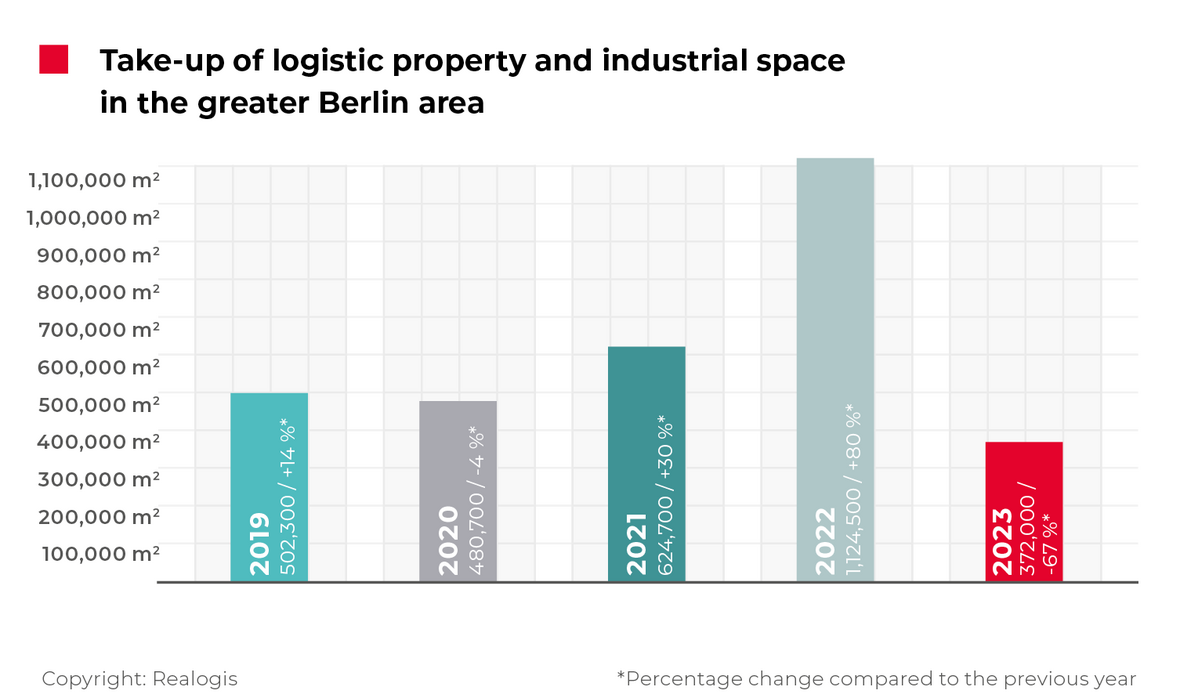

After a record year, the Berlin owner-occupier and rental market for logistics and industrial properties experienced a significant slump in take-up in 2023 as a whole. This is the conclusion of our latest analysis. After 1,124,500 m² in the previous year, take-up by all market participants in 2023 slumped by 752,500 m² to 372,000 m² or only around one-third of the previous year's level (-66.9%). Even excluding the massive Tesla deal for 327,000 m², the change is 425,500 m², i.e. a drop of more than half (-53.4%).

Take-up was a significant 40% lower than the five-year average, which currently stands at 620,840 m² (excluding Tesla: -33%, average: 555,400 m²). The main drivers were deals for existing properties, which accounted for 64% or 238,200 m². In 2022, this figure amounted to 265,800 m² or 23.6%.

Facts

- Significant decline in take-up

- Major slump in new builds

- Building types: Big boxes and business parks almost on a par

- Regional ranking: City of Berlin leads the way

- Sector ranking: 67% attributable to logistics/distribution

- Large spaces account for one-third of take-up

- Prime rent close to EUR 10 per square metre

New builds declined by around -725,000 m² or -84.4% to 133,800 m² or 36% (having led the way in 2022 with 858,700 m² or 76.4%). Even without Tesla, however, new builds would have fallen more sharply than existing properties in absolute terms at -397,900 m². 42% of all lettings and new uses in 2023 were attributable to the "big box" building class (156,400 m²). In absolute terms, its take-up of all building types (big box, business parks, other properties) saw the second biggest fall of -316,500 m² (2022: 472,900 m² or 42%).

Business parks are currently close behind with a share of 39.4% or 146,700 m². At -10,900 m², they saw the smallest decline in absolute terms and are the most stable (coming from third place with 157,600 m² or 14% in 2022). "Other properties", currently in last place, recorded the highest overall absolute decline of -425,100 m² (-86%) to 68,900 m² or a share of 18.5% (2022: 494,000 m² or 43.9%). Without the Tesla deal, however, other properties would also have fallen significantly by around -100,000 m² or -60%.

Top lessees in full-year 2023 in Greater Berlin

WeLog, approx. 38,700 m² (Expansion), Logistics, Surrounding area west of Berlin

Fiege, approx. 31,500 m² (Expansion), Logistics, Surrounding area south of Berlin

LGI, approx. 30,000 m² (Expansion), Logistics, Surrounding area west of Berlin

Bär und Ollenroth, approx. 15,300 m² (Relocation), Retail, Berlin North

BLG, approx. 10,350 m² (New business), Logistics, Surrounding area west of Berlin

With a share of 95.5% or 355,300 m² (2022: 711,900 m² or 63.3%), the Berlin logistics and industrial property market in 2023 was clearly predominantly a lessor's market. Owner-occupiers accounted for 8,700 m² or 2.3% (2022: 412,600 m² or 36.7%; Tesla was the driving force here, as this figure would have been only 7.6% or 85,600 m² without the major deal).

2.2% or 8,000 m² of take-up was attributable to properties of unknown ownership. We registered a total of 114 deals by all market participants in 2023, 29 fewer than in the same period of 2022. This is 22% below the average number of contracts concluded in the last five years, which is 147.

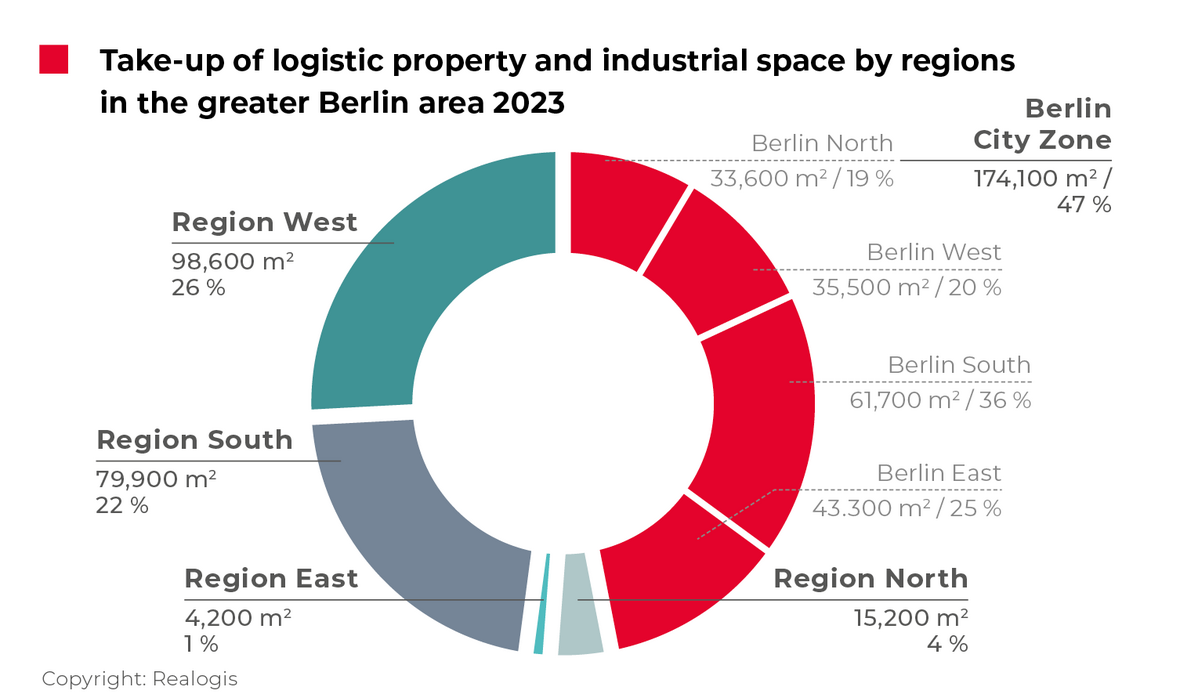

Regional ranking: City of Berlin leads the way – deals in surrounding area east of Berlin almost non-existent

According to our analysis, all regions saw lower take-up in absolute terms compared to 2022. The region with the highest take-up in 2023 was the city of Berlin, which leads the regional ranking at 174,100 m² or 46.8% (2022: 262,600 m² or 23.4%). Although the sub-market fell by -88,500 m² or -33.7% in terms of absolute take-up, it achieved the biggest increase in its relative share at +23.4 percentage points. One of the top deals of 2023 as a whole – by the retail company Bär und Ollenroth for 15,300 m² – is in the city of Berlin and accounts for around 8.8% of take-up across all city regions.

Berlin South again made the highest contribution to take-up in the city of Berlin at 61,700 m² or 35.4% (2022: 108,400 m² or 41.3%). The surrounding area west of Berlin takes second place among all five regions with 98,600 m² or 26.5% (coming from fourth place in 2022 with 151,100 m² or 13.4%). The region was down -52,500 m², or -34.7% in absolute terms compared to 2022, but its relative share increased by +13.1 percentage points in 2023. 79,050 m² or 80% of take-up was attributable to three companies with top deals: the full-service provider WeLog (38,700 m²), the logistics company LGI (30,000 m²) and the logistics company BLG (10,350 m²).

The surrounding area south of Berlin follows in third place with 79,900 m² or 21.5%, which is only around a quarter of the annual take-up in 2022 (2022: 301,100 m² or 26.8%). The main contributor to this figure was the logistics company Fiege with 31,500 m², accounting for a total of 39.4% of take-up in the market.

The penultimateplace is taken by the surrounding area north of Berlin with 15,200 m² or 4.1% (2022: 34,900 m² or 3.1%; a drop of more than half in absolute terms at -19,700 m² or -56.4%). Finally, lastplace goes to the surrounding area to the east with just 4,200 m² or 1.1% (2022: 374,800 m² or 33.3%). This area took first place in 2022 and recorded a decline of 98.9%. The fact that the past year was a weak one for the surrounding area east of Berlin is not exclusively due to the Tesla deal, which took place in this region. Take-up was also a considerable 96% lower than the five-year average for the market, which is 97,840 m².

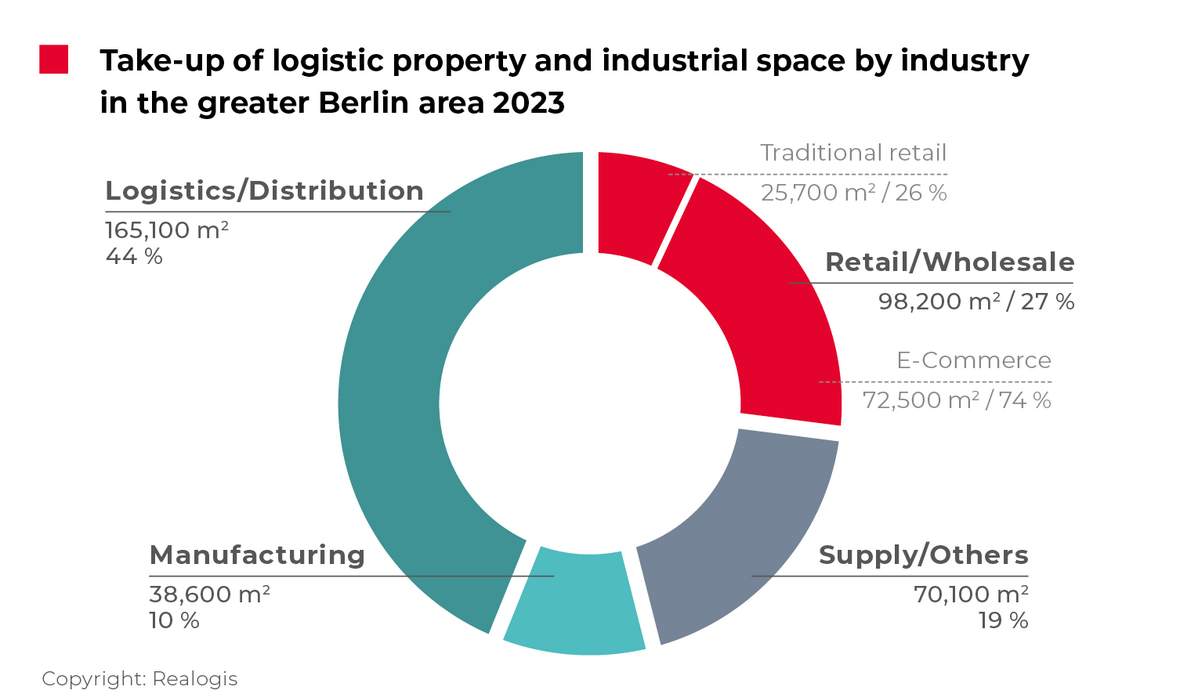

Sector ranking: 67% attributable to logistics/distribution

The logistics/distribution sector climbed two places to first for 2023 as a whole with take-up of 165,100 m² or 44.4% (2022: 193,300 m² or 17.2%; +27 percentage points in relative terms). Although all sectors reported a year-on-year decline in take-up, logistics/distribution was the least affected with a drop of 28,200 m² or -14.6%. Four of the top five deals in 2023 come from this sector and collectively account for 110,550 m² or 67% of sector take-up. Its role as a catalyst in 2023 is also confirmed by the fact that, of all sectors, logistics/distribution is closest to its five-year average of 171,500 m² (-4%).

Retail again took in second place in 2023 with 98,200 m² or 26.4% (348,200 m² or 31%) despite the significant slump in take-up of -250,000 m² or -71.8% in absolute terms. The sector fell below its five-year average of 196,780 m² by 50% in 2023. The top lease was concluded by the retail company Bär und Ollenroth, which relocated within Berlin and contributed 15,300 m² or 16% of the take-up in the retail sector. Within the retail sector, e-commerce set the pace with 72,500 m² or 73.8% (2022: 149,600 m² or 43%), significantly increasing its relative share in the process (+31 percentage points).

The traditionalretail sector saw a sharp fall to 25,700 m² or 26.2% (2022: 198,600 m² or 57%), which corresponds to a decline in traditional retail of -172,900 m² or -87.1%. Coming from last place in the previous year with 99,200 m² or 8.8%, the miscellaneous category"Other" took third place with 70,100 m² or 18.8%. Currently in last place is the manufacturing sector, which came first in the previous year. Take-up amounted to just 38,600 m² or 10.4%, down from 483,800 m² or 43%. The slump of 445,200 m² or 92% shows that the sector all but ceased to play a role last year. Even without the major Tesla deal from 2022, the change would still be 118,200 m² or -75%. The sector also fell below the five-year average of 171,600 m² by a significant 78%.

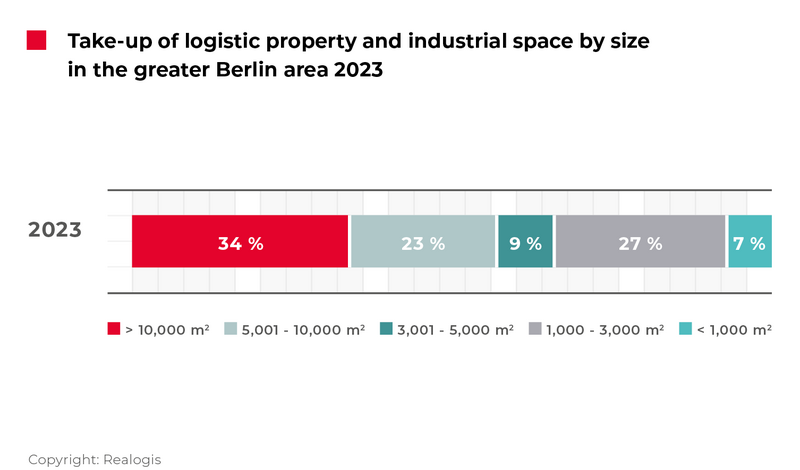

Large spaces account for one-third of take-up

Although large spaces of 10,001 m² or more made the biggest contribution to total annual take-up in 2023 with 125,860 m² or 33.8% (2022: 788,200 m² or 70.1%), they underperformed by -36.3 percentage points or -662,340 m² (-84%) in absolute terms. In total, the five largest deals in 2023 as a whole account for all of the take-up in this size category.

This might also be interesting for you:

To the market report Germany

The second-largest size segment, units between 5,001 and 10,000 m², achieved take-up of 86,000 m² or 23.1% in the past year, thereby taking third place (2022: 142,200 m² or 12.6%). Although it declined by -56,200 m² (-39.5%) in absolute terms compared to the previous year, its relative share increased by gain +10.5 percentage points in 2023. As in 2022, the category of medium-sized spaces between 3,001 and 5,000 m² was ranked second to last with 32,900 m² or 8.8% (2022: 64,500 m² or 5.7%). Small spaces between 1,000 and 3,000 m² took secondplace with 99,800 m² or 26.8% (2022: 106,400 m² or 9.5%) and saw the biggest gain in their relative share of the market for rental and owner-occupied industrial and logistics properties at +17.4 percentage points, although take-up declined by 6,600 m² in absolute terms.

This was the only size category that has performed above average and is 2.3% above its five-year average of around 98,000 m². The smallest spaces of less than 1,000 m² remained in last place with 27,450 m² or 7.4%, after 23,200 m² or 2.1% in the previous year.

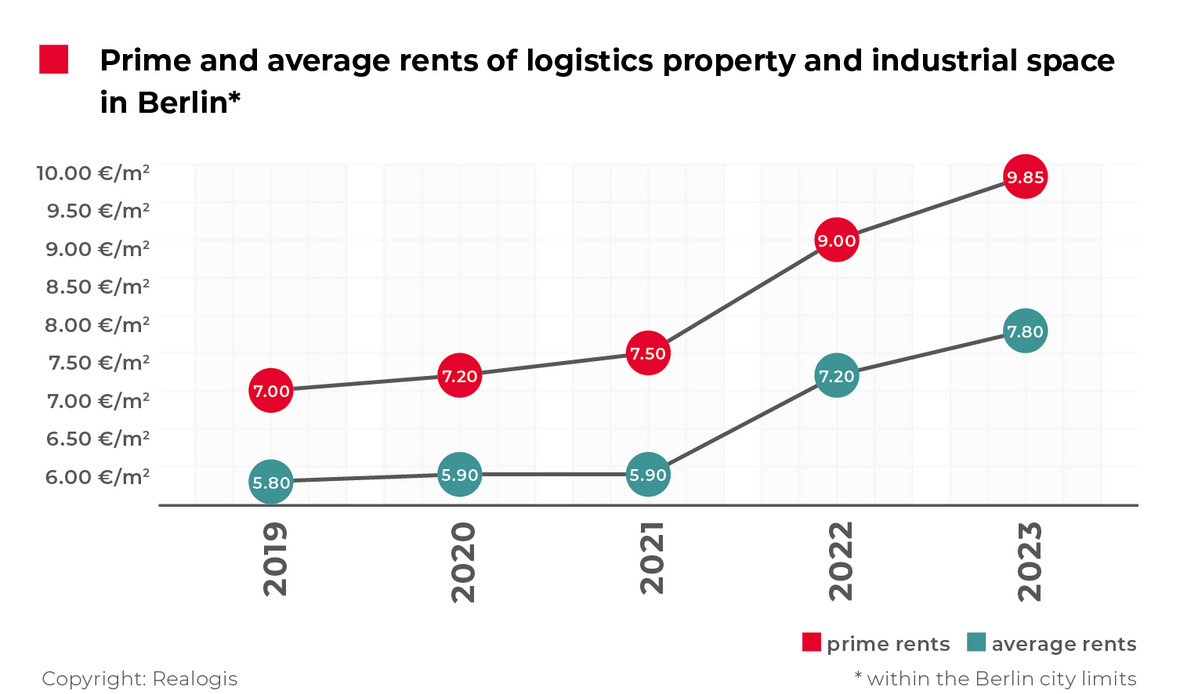

Prime rent close to EUR 10 per square metre

Prime rents in the Berlin industrial and logistics property market continued the positive trend seen in previous years and enjoyed the second strongest increase in the last five years, rising by +9.4% to EUR 9.85/m². This puts the prime rent close to EUR 10 per square metre. The prime rent rose by +20% in the previous year from EUR 7.50/m² to EUR 9.00/m².The current prime rent is 21.5% above the five-year average of EUR 8.11/m².

The averagerent rose by 8.3% from EUR 7.20/m² to EUR 7.80/m², having previously increased by +22% from EUR 5.90/m² to EUR 7.20/m² as of the end of 2022. This means that the significant upward trend in average rents is also continuing. The current five-year average of EUR 6.52/m² was thus exceeded by 19.6% in 2023.

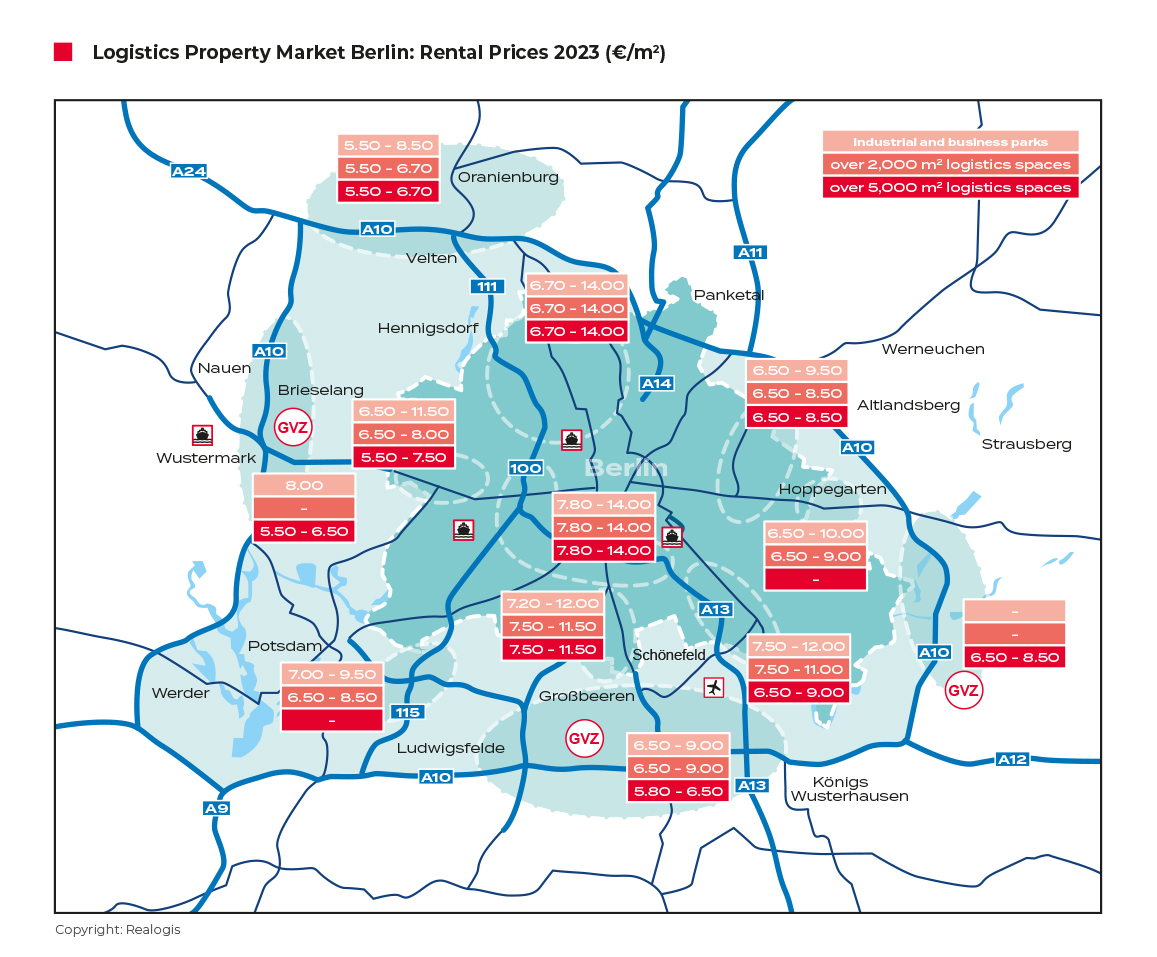

To the rent price maps:

Order the complete market report as PDF