HOCHWERTIG | 650 m² HALLE | 800 m² AUSSTELLUNG

ID: 998947DetailsGarching, repräsentatives Produktionsgebäude mit hochwertigen Büroflächen

ID: 93135Detailsca. 400 m² große, ebenerdige Lager-Produktionshalle mit Meisterbüro in Top Lage

ID: 1036679DetailsDirekt am Autobahnkreuz Ulm/Elchingen - Neubau multifunktionaler Logistik- und Produktionsflächen

ID: 994300DetailsLOGISTIK | RAMPEN | FREIFLÄCHE

ID: 1008605DetailsLager-/Logistik | Neubau | Rampen | teilbar | ebenerdig

ID: 1016255DetailsGEWERBEPARK | ERSTBEZUG | TOP-LAGE

ID: 996681DetailsBremen, ca. 1.300 m² Lager-/ Logistikfläche zu vermieten

ID: 1032273DetailsMünchen - Nord, Hallen- und Freiflächen in Bestlage zu vermieten

ID: 101077DetailsPROVISIONSFREI | GEWERBEPARK | FLEXIBEL

ID: 1000973DetailsArnsdorf | ca. 9.000 m² | Lager & Logistik | Betonrampe & ebenerdig | teilbar ab 2.000

ID: 1009874DetailsRepräsentativer Gewerbepark

ID: 1005086Detailsca. 1.350 m² große, ebenerdige Hallenfläche mit Büro

ID: 1035432DetailsPRODUKTION | LAGER | RAMPE

ID: 991522DetailsGarching, Neubau von ca. 8.000 m² Lager-,Forschungs- und Bürofläche

ID: 1030576DetailsMunich-North, warehouse and office spaces for rent

ID: 1033335DetailsMunich-North, warehouse and office spaces for rent

ID: 1024609DetailsMunich-North, warehouse and office spaces for rent

ID: 1034331DetailsMunich-North, warehouse and office spaces for rent

ID: 1002692DetailsMunich-North, warehouse and office spaces for rent

ID: 1034768DetailsMunich-North, warehouse and office spaces for rent

ID: 1034670DetailsMunich-North, warehouse and office spaces for rent

ID: 1034767DetailsMunich-North, warehouse and office spaces for rent

ID: 1025539DetailsMunich-North, warehouse and office spaces for rent

ID: 1010949DetailsMunich-North, warehouse and office spaces for rent

ID: 1032598DetailsAugsburg, site with about 2.500 sqm for rent

ID: 9040DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031912DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031769DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031836DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1028145DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030724DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030615DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1023871DetailsGladback, warehousing space for wholesale or retail for rent

ID: 95769DetailsGladback, warehousing space for wholesale or retail for rent

ID: 1013489DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1025426DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1026621DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1022435DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1023380DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1014315DetailsNeuss, approx. 1,295 sqm warehouse space in a business park for rent

ID: 997156DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1017665DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1019585Details

Do you have a question? Leave your contact details here and we will call you back!

Market report Berlin full year 2022

- About the logistics market in the economic region

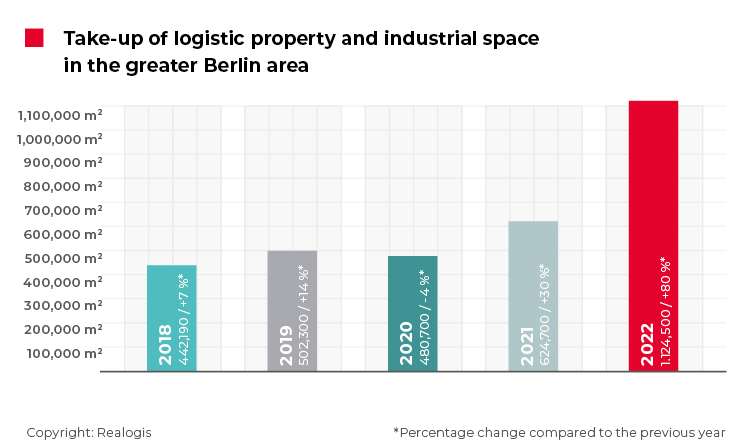

Berlin breaks past 1,000,000 m² mark for first time

According to our latest analysis, the Berlin market for rental and owner-occupied warehousing, logistics and industrial properties* reached a new record in 2022 as a whole. In the months from January to December, all market participants – such as project developers, portfolio holders, and estate agents – together generated take-up of 1,124,500 m², including the major Tesla deal with 327,000 m². According to our data, a similar record result has only ever been achieved in Germany before by the industrial and logistics property market in the Ruhr region in 2016.

The previous year’s figure of 624,700 m² was already considered an outlier but has now been topped by another 80%. Even without the Tesla deal, the previous year’s figure would still have been exceeded significantly by 26% at 787,690 m².

In addition, the five-year average of 634,878 m² was surpassed by a substantial 77%; without Tesla, the average would be 567,516 m² and would have been topped by 39%.

Facts

- 80% increase on previous year

- Significant shift towards new construction

- Big boxes and business parks responsible for only half of total take-up

- Over 700,000 m² was let, while more than 400,000 m² was attributable to owner-occupiers

- Regional ranking: Eastern vicinity of Berlin moves up to No. 1 spot

- Strong year for the manufacturing sector

- Almost three quarters of all deals were for large spaces

- Average rents rising faster than prime rents

Significant shift towards new construction

At 858,700 m², three quarters of the leases concluded related to new-builds (2021: 313,400 m²), while 265,800 m² or 23.6% related to existing properties, representing a decrease of 14.6%. 2022 is the first year since 2018 in which new construction of warehousing, logistics and industrial space accounted for the majority of take-up in Greater Berlin.

Not including the Tesla deal, there would still be a shift towards new construction, but in a slightly weaker form: New-builds would be in the lead with 521,890 m² or two thirds of take-up, followed by existing properties with one third (265,800 m²).

Top lessees in full-year 2022 in Greater Berlin

Tesla, eastern vicinity of Berlin, approx. 327,000 m² (new business), manufacturing

Sonepar, western vicinity of Berlin, approx. 41,250 m² (new business), retail

Tesla, southern vicinity of Berlin, approx. 38,887 m² (expansion), manufacturing

Lidl, western vicinity of Berlin, approx. 32,738 m² (expansion), retail

Schnellecke, southern vicinity of Berlin, approx. 30,800 m² (new business), logistics

Picnic, southern vicinity of Berlin, approx. 30,345 m² (new business), e-commerce

VAH, northern vicinity of Berlin, approx. 30,320 m² (expansion), logistics

Big boxes and business parks responsible for only half of total take-up

Lettings in big-box properties accounted for 472,900 m² or 42.1%, while those in business parks came to 157,600 m² or 14%. Other properties (neither big boxes nor business parks) accumulated 43.9% of take-up or 494,000 m² (also including the major Tesla deal in a production property).

Excluding Tesla’s outlier deal, it can be seen that take-up in Berlin was dominated by big boxes, which contributed 60% of take-up, while business parks and other deals each accounted for 20%.

Take-up of more than 700,000 m²

711,900 m² of newly leased space was attributable to properties that were not owned by their users. Owner-occupied space accounted for 412,600 m², particularly including the major Tesla deal. Without Tesla, only one in ten square metres or 75,790 m² was taken up in owner-occupied properties.

We observed a total of 143 deals by all market participants on the Berlin market in 2022, which is 11 fewer than the previous year’s figure of 154. However this decrease is attributable to the smallest size category of less than 1,000 m² due to lower supply (14 deals fewer than in the previous year). This is also reflected in the average amount of space taken up, which came to 4,050 m² in 2021 and 7,900 m² or 5,500 m² (not including Tesla) in 2022.

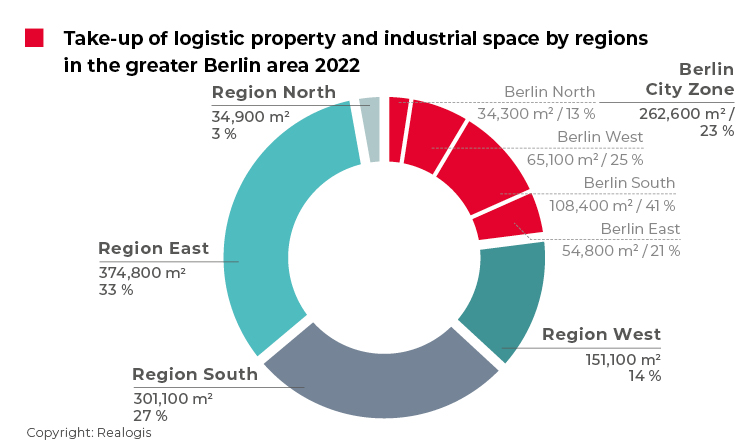

Regional ranking: Eastern vicinity of Berlin moves up to No. 1 spot

The area where the most space was taken up was the eastern vicinityof Berlin, with 378,800 m² or one third of take-up for the year as a whole. Coming from last place in the previous year with 55,000 m² or 9%, this market area moved up four spots and displayed the most significant growth out of all regions in terms of both relative share (+24.5 percentage points) and absolute take-up (almost sevenfold increase compared to 2021). The Tesla deal was the key factor, accounting for a share of 87%. Without the Tesla deal, the eastern vicinity would thus have been second to last with take-up of around 47,800 m².

In second place was the southern vicinity of Berlin with 301,100 m² or 26.8%, which had been in first place in 2021 with 247,100 m² or 39.6%. Despite an absolute increase of 21.9%, its share decreased the most out of all regions, falling by 12.8 percentage points. Three of the top lessees – Tesla, Schnellecke and Picnic – together contributed around 100,000 m² or one third of this region’s take-up.

Third place was taken by the city of Berlin at 262,600 m² or 23.4%, compared with second place in 2021 at 178,000 m² or 28.5%. At first glance, the city of Berlin did not seem to benefit from the strong annual result and saw a decline in its relative share of 5.1 percentage points, continuing the negative trend of the previous years since 2020. But despite this slight loss of ground in relative terms, the city increased its absolute take-up by a significant 47.5% and last year recorded its highest take-up since 2018.

Within Berlin, the Berlin South area was in the lead with 108,400 m² or 41.3%. This corresponds to an increase of 74.8% compared to 62,000 m² in 2021. Berlin West accounted for 65,100 m² or 24.8% (-20.2 percentage points, 2021: 78,900 m²), Berlin East for 54,800 m² or 20.9% (+10 percentage points; 2021: 18,600 m²) and Berlin North for 34,300 m² or 13.1% (+85.4%, compared to 8,500 m²).

Second to last was the western vicinity of Berlin with 151,100 m² or 13.4% (2021: 64,600 m² or 10.3%). It more than doubled its take-up, partly thanks to two top deals by Sonepar and LIDL, which contributed roughly half of take-up at 74,000 m².

In last place was the northern vicinity of Berlin with 34,900 m² or 3.1%, which was previously in fourth place with 80,000 m² or 12.8%. Out of all regions, it saw the biggest decrease in absolute take-up at -56.4% and the second-biggest decrease in its share at -9.7 percentage points.

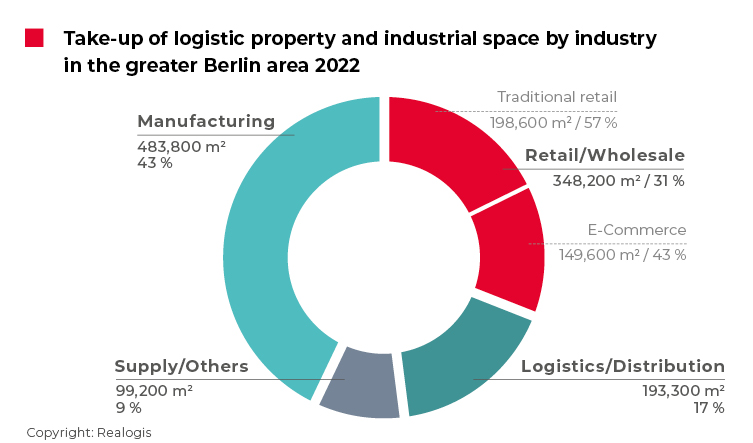

Sector ranking: Strong year for manufacturing

Due to the Tesla deal, the manufacturing sectorwas in the lead on the Berlin rental market for industrial and logistics properties in 2022 as a whole, accounting for 483,800 m² or 43%. This is a first since our records began. In the previous year, manufacturing was still in third place at 109,700 m² or 17%. The sector’s take-up thus more than quadrupled year-on-year, and its relative share also increased significantly by 26 percentage points.

Not including the Tesla deal, take-up here would have come to 146,990 m², putting the sector in third place (as in the previous year). However, take-up would still have been up by around a third year-on-year at 146,990 m² (2021: 109,700 m²), showing that the manufacturing sector is increasingly becoming a major lessee.

Retail came second again with 348,200 m² or 31%. Compared to the previous figure of 193,000 m² and a share of likewise 31%, take-up thus increased by a significant 80%. Three of the top deals – with Sonepar, LIDL and Picnic – contributed around 104,000 m² or 30% here. Traditional retail accounted for 198,600 m² or 57%, while e-commerce accounted for 149,600 m² or 43%.

In third place was the logistics/distribution sector with 193,300 m² or 17.2% (2021: 242,600 m² or 38.8%). It thus moved down two spots year-on-year and saw the biggest decrease in its share at 22 percentage points and the biggest decrease in absolute take-up at -20.3% since 2021. A total of 61,120 m² or 31.6% of the sector’s take-up was generated by the two top deals Schnellecke and VAH.

As in the previous year, last place goes to the “Other” category with 99,200 m² or 8.8% (2021: 79,400 m², 12.7%).

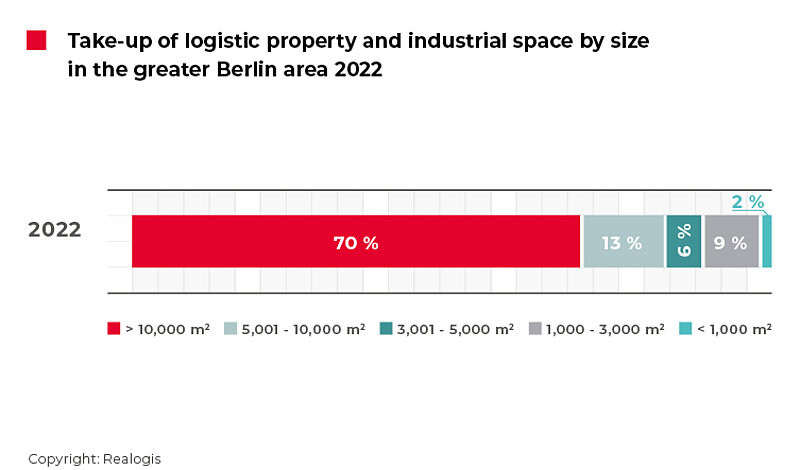

Size categories: Almost three quarters of all deals were for large spaces

As in the previous year, the largest share of space was contributed by the category of large spaces of 10,001 m² or more, which currently account for 70.1% or 788,200 m². The seven top deals alone accumulated 531,340 m² or two thirds of take-up in this size category. Not including Tesla, this category would still be in first place at 57.3% or 451,390 m².

The size category between 5,001 and 10,000 m²came second again in 2022 at 142,200 m² or 12.6% (2021: 173,700 m² or 27.8%). However, it lost the most ground year-on-year out of all categories in terms of its share of take-up, which fell by 15.2 percentage points.

This might also be interesting for you:

To the market report Germany

The size category of 3,001 to 5,000 m² ranked fourth again with 64,500 m² or 5.7% (2021: 76,500 m² or 12.2%). Small to medium-sized spaces of between 1,000 and 3,000 m² were in third place again in 2022 with 106,400 m² or 9.5% (2021: 93,100 m² or 14.9%), while the smallest spaces of less than 1,000 m² still came last with 23,200 m² or 2.1% (2021: 34,900 m² or 5.6%).

Even without the Tesla deal, there would be a similar picture: All size categories would see a decrease in their share except that of large spaces of 10,001 m² or more, whose share would grow significantly. Likewise, only the biggest size category and the 1,000 to 3,000 m² category would post an increase in take-up.

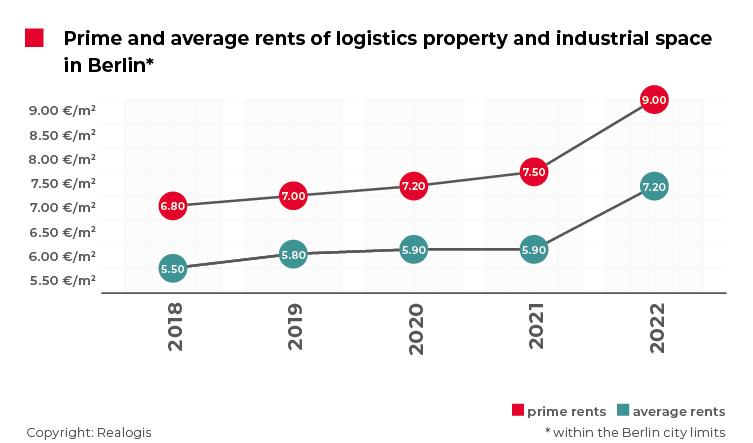

Average rents rising faster than prime rents

Prime rentcontinued the positive trend of the previous years. Starting from the highest level so far of EUR 7.50/m² in 2021, it increased another 20% or EUR 1.50/m² to reach a new record of EUR 9.00/m². This development represents the highest absolute year-on-year difference since our records began. The current prime rent is 20% above the five-year average of EUR 7.50/m².

The average rent has risen by 22%, thus outpacing the increase in the prime rent. At the end of 2022, it came to EUR 7.20/m² – close to the previous year’s level for prime rent – after EUR 5.90/m² in 2021. It thus exceeded the current five-year average of EUR 6.06/m² by 18.8%.

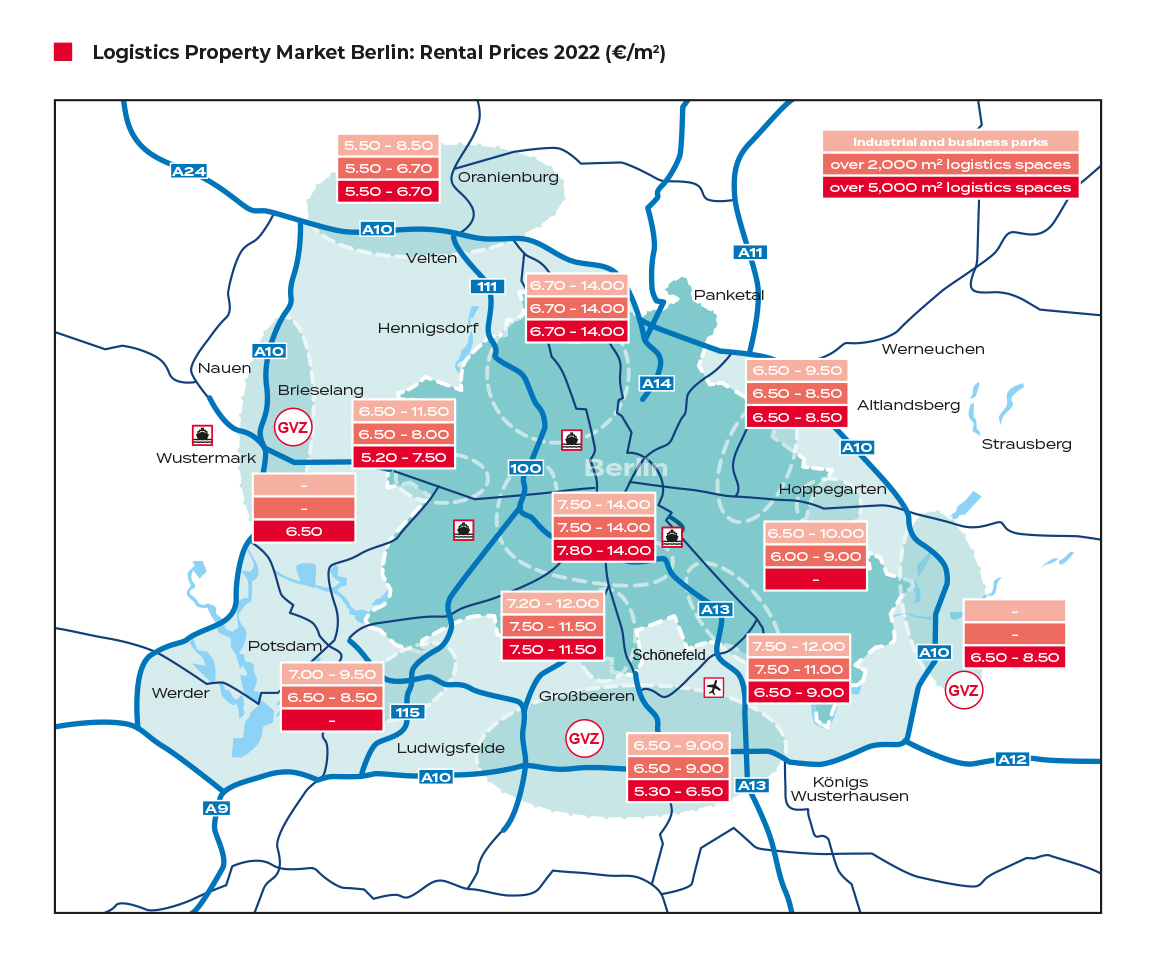

To the rent price maps:

Order the complete market report as PDF