HOCHWERTIG | 650 m² HALLE | 800 m² AUSSTELLUNG

ID: 998947DetailsGarching, repräsentatives Produktionsgebäude mit hochwertigen Büroflächen

ID: 93135Detailsca. 400 m² große, ebenerdige Lager-Produktionshalle mit Meisterbüro in Top Lage

ID: 1036679DetailsDirekt am Autobahnkreuz Ulm/Elchingen - Neubau multifunktionaler Logistik- und Produktionsflächen

ID: 994300DetailsLOGISTIK | RAMPEN | FREIFLÄCHE

ID: 1008605DetailsLager-/Logistik | Neubau | Rampen | teilbar | ebenerdig

ID: 1016255DetailsGEWERBEPARK | ERSTBEZUG | TOP-LAGE

ID: 996681DetailsBremen, ca. 1.300 m² Lager-/ Logistikfläche zu vermieten

ID: 1032273DetailsMünchen - Nord, Hallen- und Freiflächen in Bestlage zu vermieten

ID: 101077DetailsPROVISIONSFREI | GEWERBEPARK | FLEXIBEL

ID: 1000973DetailsArnsdorf | ca. 9.000 m² | Lager & Logistik | Betonrampe & ebenerdig | teilbar ab 2.000

ID: 1009874DetailsRepräsentativer Gewerbepark

ID: 1005086Detailsca. 1.350 m² große, ebenerdige Hallenfläche mit Büro

ID: 1035432DetailsPRODUKTION | LAGER | RAMPE

ID: 991522DetailsGarching, Neubau von ca. 8.000 m² Lager-,Forschungs- und Bürofläche

ID: 1030576DetailsMunich-North, warehouse and office spaces for rent

ID: 1033335DetailsMunich-North, warehouse and office spaces for rent

ID: 1024609DetailsMunich-North, warehouse and office spaces for rent

ID: 1034331DetailsMunich-North, warehouse and office spaces for rent

ID: 1002692DetailsMunich-North, warehouse and office spaces for rent

ID: 1034768DetailsMunich-North, warehouse and office spaces for rent

ID: 1034670DetailsMunich-North, warehouse and office spaces for rent

ID: 1034767DetailsMunich-North, warehouse and office spaces for rent

ID: 1025539DetailsMunich-North, warehouse and office spaces for rent

ID: 1010949DetailsMunich-North, warehouse and office spaces for rent

ID: 1032598DetailsAugsburg, site with about 2.500 sqm for rent

ID: 9040DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031912DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031769DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031836DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1028145DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030724DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030615DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1023871DetailsGladback, warehousing space for wholesale or retail for rent

ID: 95769DetailsGladback, warehousing space for wholesale or retail for rent

ID: 1013489DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1025426DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1026621DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1022435DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1023380DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1014315DetailsNeuss, approx. 1,295 sqm warehouse space in a business park for rent

ID: 997156DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1017665DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1019585Details

Do you have a question? Leave your contact details here and we will call you back!

Market report Stuttgart half year 2023

- About the logistics market in the economic region

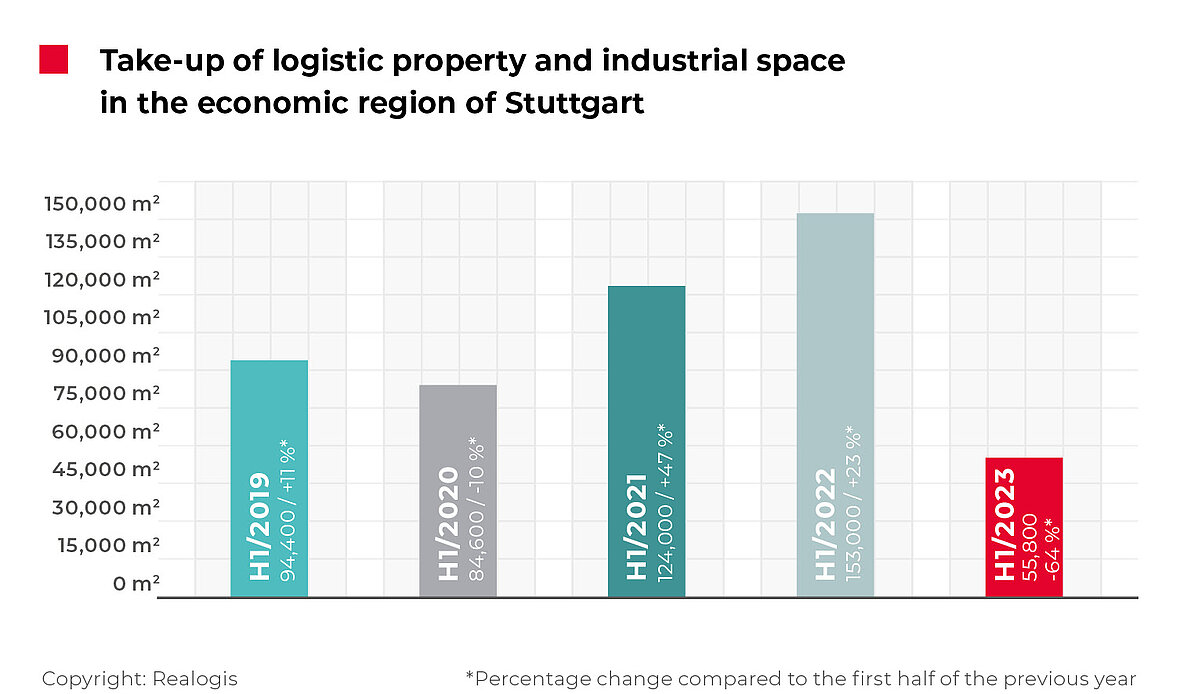

Take-up of industrial and logistics properties in Stuttgart declines by over 60%

The rental and owner-occupied market for industrial and logistics properties in the Stuttgart metropolitan region set a new negative record in the first half of 2023. The take-up across all market participants amounted to 55,800 m². Compared with 153,000 m² in H1 2022 – the strongest ever half-year result since we started keeping records – this represents an unprecedented downturn in take-up of 97,200 m² or -63.5%.

No figure since H1 2019 was further removed from the 100,000 mark. Take-up also fell below the five-year average for the first half of the year of 102,360 m² by a substantial 45.5%.

As we already indicated in the full-year report for 2022, the reasons for the caution on the market include the recessionary sentiment among companies with respect to future-oriented strategic decisions and the prevailing shortage of space. We are still receiving serious requests for space and it would have been possible to conclude significantly more leases in the first half of the year if the corresponding properties and development projects had been available, although the figure would have been down on the previous year.

Facts

- Take-up for the first half of the year comes in at just above half the five-year average

- Market dominated by recessionary sentiment and shortage of space

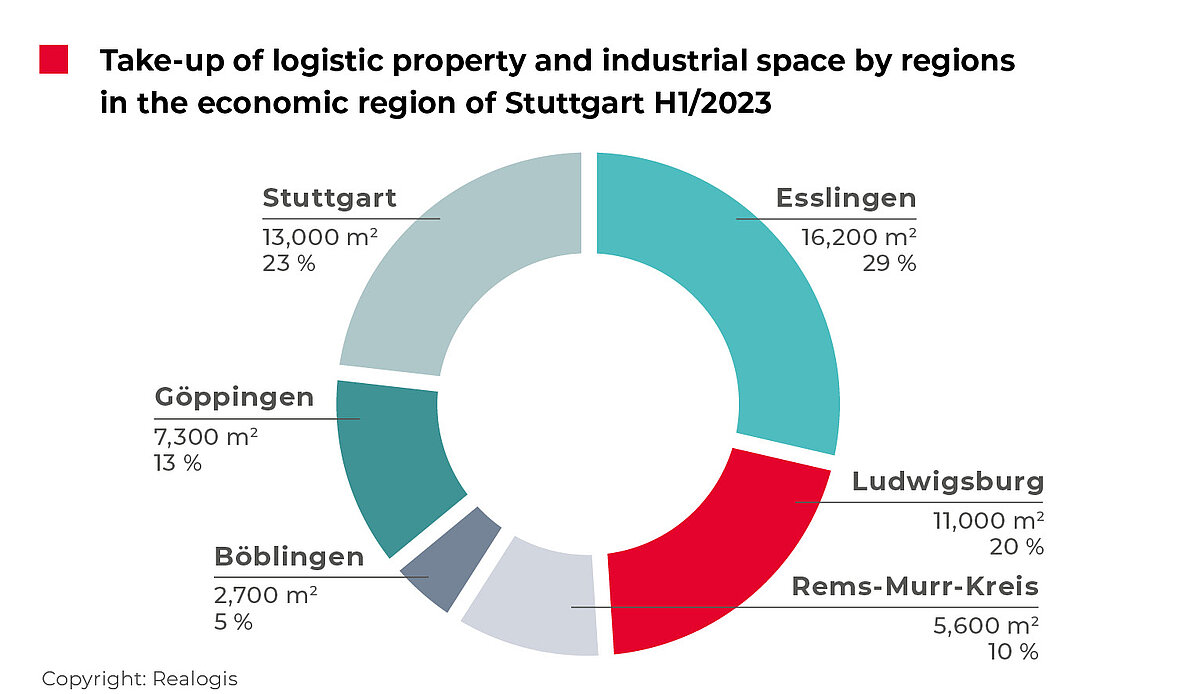

- Regional ranking: Esslingen and Böblingen districts largely responsible for the downturn in take-up

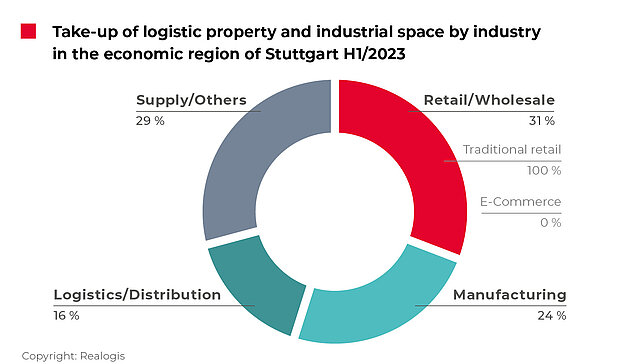

- Sector ranking: Retail continues to lead the way – no e-commerce deals

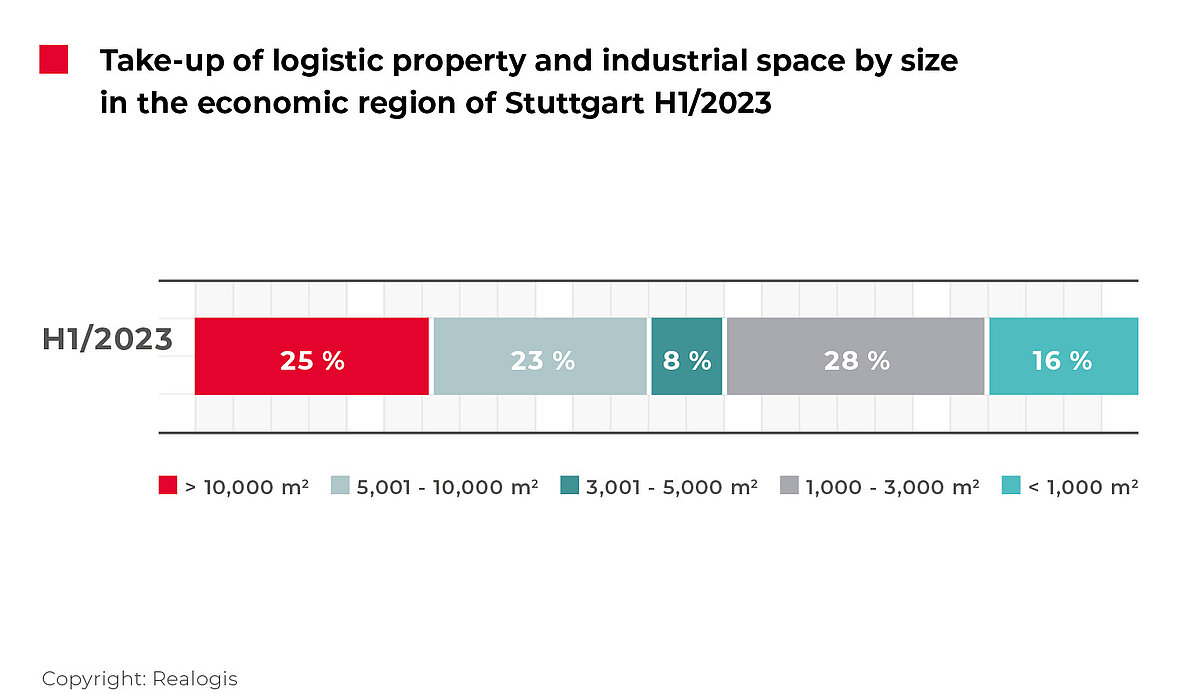

- Lack of lettings for large and medium-sized units

- Sharp rise in prime and average rents

As in the same period of the previous year, lettings in existing properties accounted for the majority of take-up at 48,800 m² or 87.5%. This means existing properties were responsible for almost nine in every ten square meters of take-up, with the trend in the relative share observed in the previous year continuing to intensify (H1 2022: 74.3% or 113,700 m²). In absolute terms, however, this represents a decline of 64,900 m² or -57.1%.

The share of new builds attributable to the deal concluded by a manufacturing company fell from an exceptional 39,300 m² or 25.7% in the same period of the previous year to 7,000 m² or 12.5% (-32,300 m² or -82.2%).

Stuttgart was exclusively a tenants’ market, with no owner-occupancy deals concluded in the first half of 2023.

Biggest deals

Paul Lange & Co. OHG, Göppingen district, approx. 14,000 m² (Existing property), Retail

Manufacturing company, Ludwigsburg district, approx. 7,000 m² (New build), Manufacturing

Logistics company, Stuttgart, approx. 5,824 m² (Existing property), Logistics/ distribution

Regional ranking: Esslingen and Böblingen districts largely responsible for the downturn in take-up

The Esslingen district accounted for the highest share of take-up in the first half of the year at 16,200 m² or 29% (H1 2022: 45,200 m² or 29.5%, down 29,000 m² or 64.2% in absolute terms).

Second place was taken by the Stuttgart region at 13,000 m² or 23.3% compared with 5,000 m² and 3.3% in the previous year, making it the only region to see an increase in absolute terms (with take-up more than doubling by +8,000 m² or +160%). At +20 percentage points, it also saw the biggest increase in its relative share of total take-up. Unlike in the same period of the previous year, the city of Stuttgart saw one of the top take-ups thanks to the deal concluded by a logistics company for 5,824 m² (44.8%).

The Ludwigsburg region remains in third place at 11,000 m², corresponding to 19.7% of total take-up (H1 2022: 25,200 m² or 16.5%, down 14,200 m² or -56.3% in absolute terms). The next positions are occupied by Göppingen at 7,300 m² or 13.1% (H1 2022: 7,900 m² or 5.2%, down 600 m² or -7.6% in absolute terms), the Rems-Murr district at 5,600 m² or 10% (H1 2022: 12,800 m² or 8.4%) and the Böblingen district at 2,700 m² or 4.8% (H1 2022: 56,900 m² or 37.2%). The latter region saw two of the top deals in the region in the first half of the previous year, whereas no such deals were concluded in the first half of this year.

All in all, Esslingen and Böblingen districts accounted for 79.1% of the year-on-year change in take-up.

Sector ranking: Retail continues to lead the way – no e-commerce deal

In the sector analysis, retail has been responsible for the most take-up since H1 2021 and this remained the case in the first half of the current year. Although the sector retained its leading position with take-up of 17,000 m² or 30.5%, this represented a reduction of 49,100 m² or -74.3% to around one-quarter of the prior-year figure (H1 2022: 66,100 m² or 43.2%).

While traditional retail accounted for just over half of take-up in the retail sector in the previous year, no deals were concluded by e-commerce companies in the first half of this year (H1 2022: traditional retail 55.5% or 36,700 m², e-commerce 29,400 m² or 44.5%).

The majority of retail take-up was attributable to the major deal by the wholesaler Paul Lange & Co. OHG at 14,000 m² (corresponding to 82% of take-up in retail and traditional retail alike).

The “Other” category came in just behind retail with take-up of 16,600 m² or 29.7%, after 23,500 m² or 15.4% in the same period of the previous year. This year-on-year decrease of 6,900 m² or -29.4% was moderate compared with other sectors, while the relative share of take-up rose by a substantial 14.4 percentage points. Because all of the other sectors saw more pronounced downturns, in some cases significantly so, the “Other” category increased its relative share even as absolute take-up declined.

The remaining positions were taken by manufacturing at 13,200 m² or 23.7% (H1 2022: 27,300 m² or 17.8%) and logistics/ distribution at 9,000 m² or 16.1% (H1 2022: 36,100 m² or 23.6%).

Although take-up decreased across all sectors, this trend was particularly pronounced in the retail sector – especially e-commerce – and in logistics/ distribution.

This might also be interesting for you:

To the market report Germany

Lack of lettings for large and medium-sized units

Large spaces of 10,001 m² or more were the second-largest size category in H1 2023, accounting for 14,000 m² or 25.1% of total take-up. Compared with 71,200 m² or 46.5% in the same period of the previous year, this category saw the biggest downturn in absolute terms at -57,200 m² (-80.3%) and the most pronounced relative decrease of -21.4 percentage points. The deal concluded by Paul Lange & Co. OHG accounted for all of the take-up in this category.

Spaces of between 5,001 and 10,000 m² saw take-up of 12,824 m² or 23% (H1 2022: 26,400 m² or 17.3%, down -13,576 m² or -51.4% in absolute terms), which included the two top deals concluded by a manufacturing company and a logistics company.

Units between 3,001 and 5,000 m² contributed take-up of 4,300 m² or 7.7% (H1 2022: 33,500 m² or 21.9%, down -29,200 m² or -87.2% in absolute terms). Small to medium-sized spaces of between 1,000 and 3,000 m² came in at 15,576 m² or 27.9%, thereby accounting for the biggest share of take-up in the first half of 2023 (H1 2022: 19,800 m² or 12.9%, down -4,224 m² or -21.3% in absolute terms). The smallest spaces of less than 1,000 m² contributed 9,100 m² or 16.3% of total take-up (H1 2022: 2,100 m² or 1.4%). The smallest spaces of less than 1,000 m² were the only size category to see an increase in take-up.

The lack of lettings in two categories – large spaces of 10,001 m² or more and medium-sized units of between 3,001 and 5,000 m² – accounted for most of the change in the weak half-year result.

Large spaces were responsible for 55% or -57,200 m² of the decrease in total take-up, while medium-sized to large spaces accounted for a further 28% or -29,200 m². Taken together, they make up 83% or 86,400 m² of the 97,200 m² reduction in the half-year result.

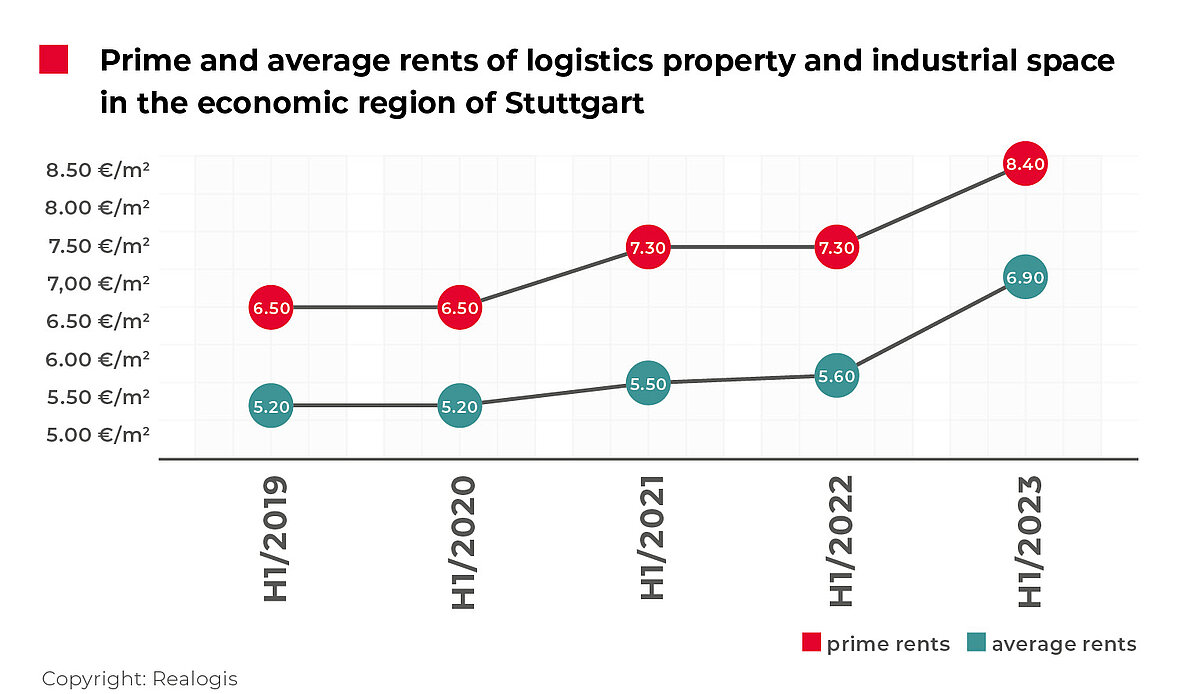

Sharp rise in prime and average rents

After stagnating at EUR 7.30/m² in the first half of the previous year, prime rent saw strong growth of 15.1% over the past twelve months to a new high of EUR 8.40/m². This represents the biggest increase since our records began. The current prime rent is a substantial 16.7% higher than the five-year average of EUR 7.20/m².

Average rent picked up even more strongly than prime rent, rising by 23.2% to EUR 6.90/m² compared with EUR 5,60/m² previously. This is 21.5% higher than the five-year average of EUR 5.68/m².

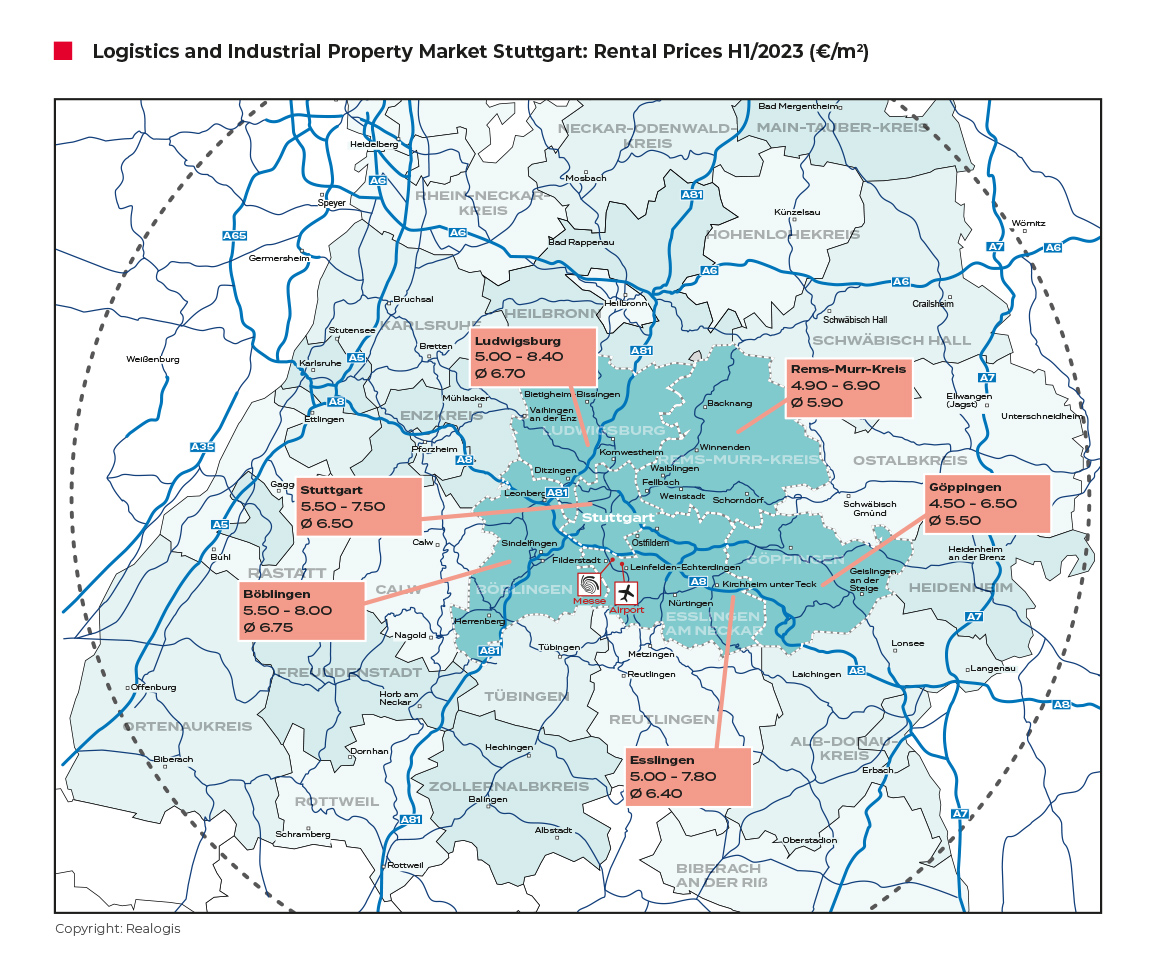

To the rent price maps:

Request the complete market report as PDF