HOCHWERTIG | 650 m² HALLE | 800 m² AUSSTELLUNG

ID: 998947DetailsGarching, repräsentatives Produktionsgebäude mit hochwertigen Büroflächen

ID: 93135Detailsca. 400 m² große, ebenerdige Lager-Produktionshalle mit Meisterbüro in Top Lage

ID: 1036679DetailsDirekt am Autobahnkreuz Ulm/Elchingen - Neubau multifunktionaler Logistik- und Produktionsflächen

ID: 994300DetailsLOGISTIK | RAMPEN | FREIFLÄCHE

ID: 1008605DetailsLager-/Logistik | Neubau | Rampen | teilbar | ebenerdig

ID: 1016255DetailsGEWERBEPARK | ERSTBEZUG | TOP-LAGE

ID: 996681DetailsBremen, ca. 1.300 m² Lager-/ Logistikfläche zu vermieten

ID: 1032273DetailsMünchen - Nord, Hallen- und Freiflächen in Bestlage zu vermieten

ID: 101077DetailsPROVISIONSFREI | GEWERBEPARK | FLEXIBEL

ID: 1000973DetailsArnsdorf | ca. 9.000 m² | Lager & Logistik | Betonrampe & ebenerdig | teilbar ab 2.000

ID: 1009874DetailsRepräsentativer Gewerbepark

ID: 1005086Detailsca. 1.350 m² große, ebenerdige Hallenfläche mit Büro

ID: 1035432DetailsPRODUKTION | LAGER | RAMPE

ID: 991522DetailsGarching, Neubau von ca. 8.000 m² Lager-,Forschungs- und Bürofläche

ID: 1030576DetailsMunich-North, warehouse and office spaces for rent

ID: 1033335DetailsMunich-North, warehouse and office spaces for rent

ID: 1024609DetailsMunich-North, warehouse and office spaces for rent

ID: 1034331DetailsMunich-North, warehouse and office spaces for rent

ID: 1002692DetailsMunich-North, warehouse and office spaces for rent

ID: 1034768DetailsMunich-North, warehouse and office spaces for rent

ID: 1034670DetailsMunich-North, warehouse and office spaces for rent

ID: 1034767DetailsMunich-North, warehouse and office spaces for rent

ID: 1025539DetailsMunich-North, warehouse and office spaces for rent

ID: 1010949DetailsMunich-North, warehouse and office spaces for rent

ID: 1032598DetailsAugsburg, site with about 2.500 sqm for rent

ID: 9040DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031912DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031769DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031836DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1028145DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030724DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030615DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1023871DetailsGladback, warehousing space for wholesale or retail for rent

ID: 95769DetailsGladback, warehousing space for wholesale or retail for rent

ID: 1013489DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1025426DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1026621DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1022435DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1023380DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1014315DetailsNeuss, approx. 1,295 sqm warehouse space in a business park for rent

ID: 997156DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1017665DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1019585Details

Do you have a question? Leave your contact details here and we will call you back!

Market report Munich half year 2023

- About the logistics market in the economic region

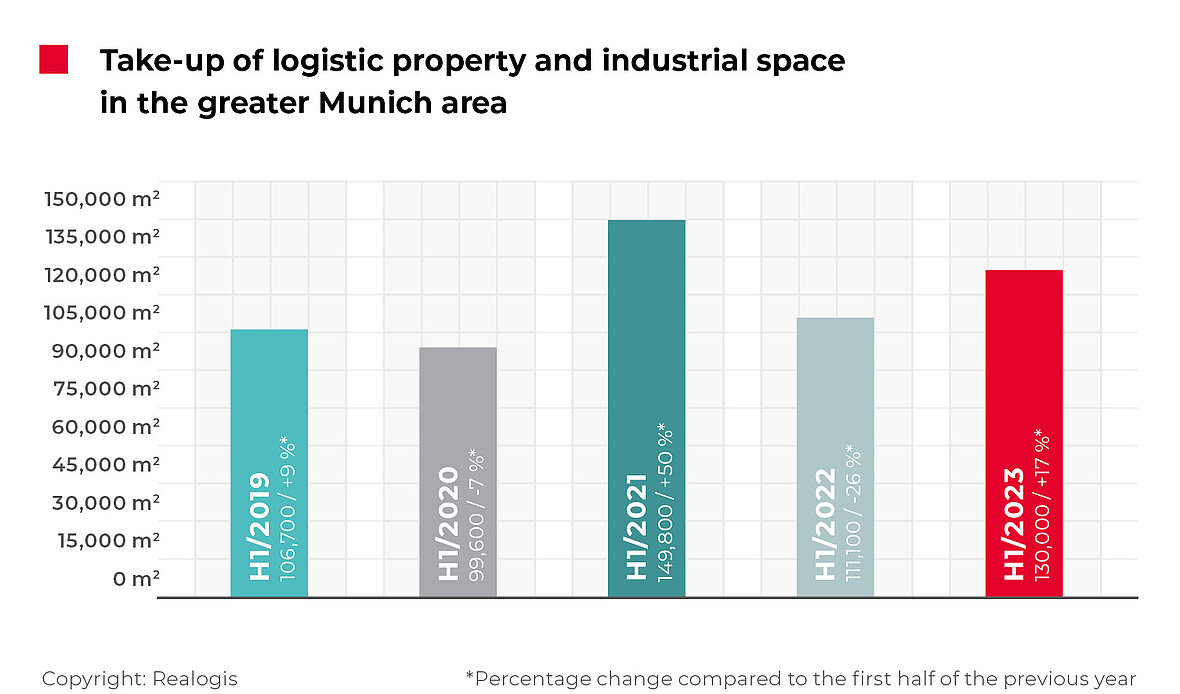

Munich’s industrial and logistics property market resistant to crisis

While many commercial property markets faltered or collapsed in the first half of 2023, Munich’s market for rental and owner-occupied industrial and logistics properties proved resistant to the crisis. In the first six months of 2023, the take-up achieved by all participants in Munich’s industrial and logistics property market for renters and owner-occupiers amounted to 130,000 m². This equates to growth of 17% on the first half of the previous year.

In terms of the take-up of all market participants, the first half of 2023 was above average. The five-year average for the first half of a year, which is currently 119,400 m², was exceeded by 8.8%.

The half-year result was significantly influenced by the major deal for 30,000 m² of usable space at the former KraussMaffei site in Allach in the northwest of the city, which was secured by Siemens Mobility GmbH.

Facts

- + 17% with take-up of 130,000 m²

- Negative trend of the previous year overcome

- Existing properties provide nearly 77% of take-up

- Region ranking: Munich North in first place

- Sector ranking once again led by manufacturing

- Smaller spaces between 1,000 and 3,000 m² remain number one

- Prime rent set to rise again

We expect the Munich market for rental and owner-occupied industrial and logistics properties to reach the 200,000 m² mark again by the end of the year.

Like in the first halves of previous years, the market was dominated by deals in existing properties. With three out of every four square metres (76.5% or 99,400 m²), the overwhelming majority of take-up was attributable to existing space. The remaining 30,600 m² or 23.5% took place in new properties, which is line with the average for the first halves of the last five years of 24.5% or 28,663 m².

Biggest deals

Siemens Mobility GmbH, Munich north (city), approx. 30,000 m² (Exisiting property), Manufacturing

Yaskawa Europe GmbH, Munich north, approx. 10,000 m² (New building), Manufacturing

Drinks supplier, Munich south (city), approx. 6,200 m² (Exisiting property), Retail (E-commerce)

BRUNS Messe- und Ausstellungsgestaltung GmbH, Munich north, approx. 5,500 m² (Exisiting property), Other

Voltstorage GmbH, Munich north, approx. 5,200 m² (New building), Other

In-Tech GmbH, Munich north, approx. 5,029 m² (New building), Manufacturing

In the first half of 2023, as so often in recent years, there was a lack of newly built space on the Munich market. We assume that rents will remain stable for potential new construction projects that will be realised or at least initiated before the end of the year. Because of the strong demand, they could even continue to increase. ESG issues are becoming increasingly important for new builds, including with regard to the exit for investors.

Overall, we registered 42 deals in the reporting period, two fewer than in the first half of 2022.

As in the same period of the previous year, the breakdown by type of building leased is dominated by “other properties”, which cannot be assigned either to big boxes or business parks, at 85,300 m² or 65.6% (H1 2022: 78,000 m² or 70.2%). Deals in business parks came to 44,700 m² or 34.4% (H1 2022: 33,100 m² or 29.8%). As in the same period of the previous year, no big box leases were registered. The breakdown of take-up by building type largely matches the same period of the previous year.

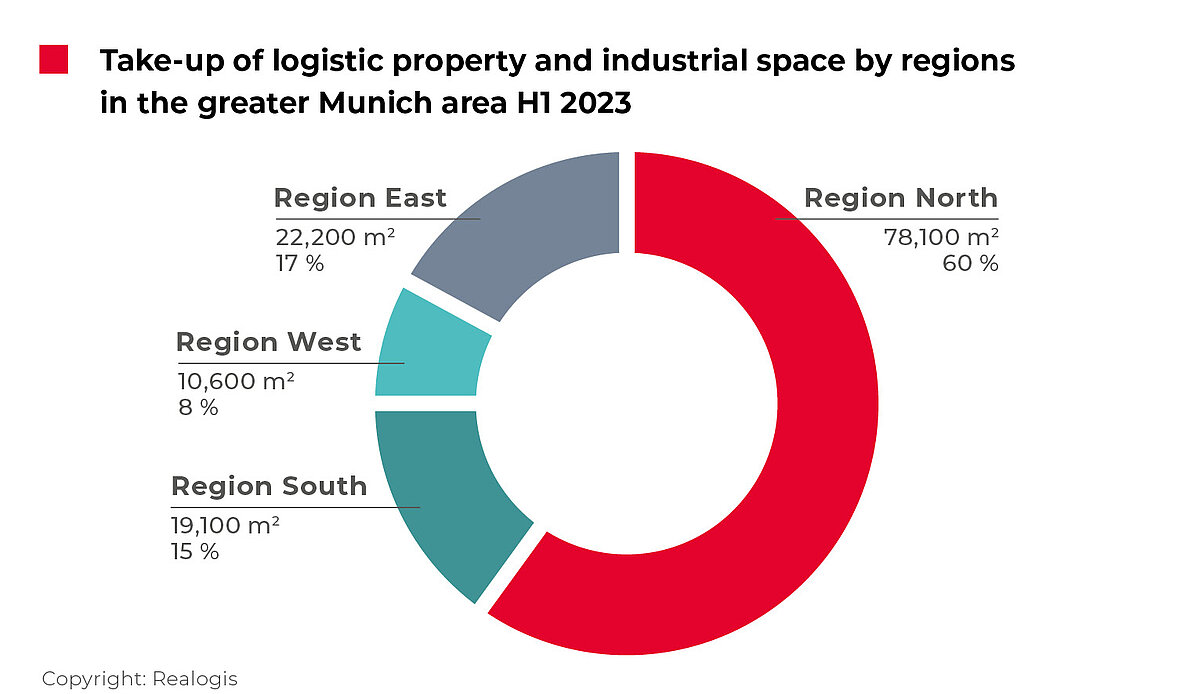

Region ranking: Munich North remains in first place

The region with the highest take-up in the first half of 2023 was Munich North with 78,100 m² or 60.1% (+87% on H1 2022). With the exception of the first half of 2022, Munich North was always the region with the highest take-up in the first halves of the last five years. Five of the six biggest deals are currently attributable to this region and cumulatively amount to 55,729 m². In addition to the largest deal by Siemens Mobility GmbH, Yaskawa Europe GmbH’s lease for 10,000 m² is also located in the North.

In second place was the East region with 22,200 m² or 17.1% (+53% or +4 percentage points on H1 2022) – it achieved this result without even contributing a top deal. Munich South was in third place with 19,100 m² or 14.7% (+12.5 percentage points on H1 2022), a third of which was due to a 6,200 m² lease taken up by a well-known drinks supplier. Last place went to Munich West with 10,600 m² or 8.2%, coming from first place with 52,300 m² or 47.1% in the first half of 2022 (significant drop of -80% or -38.9 percentage points on H1 2022).

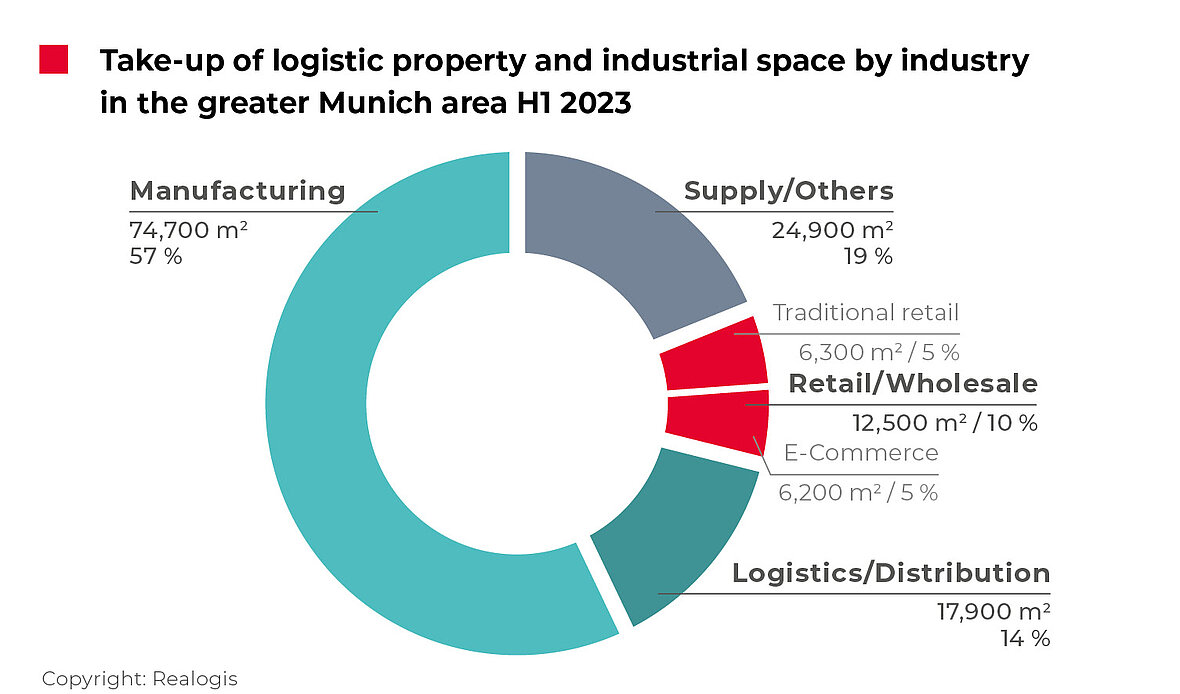

Sector ranking once again led by manufacturing

Once again, the leading sector in the first half of 2023 was manufacturing with 74,700 m² or 57.5%, compared with 45,600 m² or 41% in H1 2022. In absolute terms, it therefore achieved the second-highest growth of 64%. At 16.4 percentage points, it was also the sector with the greatest increase in its relative share. Together, Siemens Mobility GmbH, Yaskawa Europe GmbH and In-Tech GmbH contributed 45,029 m² or 60.3%.

Second place was taken by the “Other” category with 24,900 m² or 19.2%, which is unusual for the Munich market (in the first halves of the last five years, this category’s average share in total take-up amounts to 9%). This was due in particular to the two top deals by BRUNS Messe- und Ausstellungsgestaltung GmbH and Voltstorage GmbH.

The logistics/ distribution sector moved from second to third place with 17,900 m² or 13.8% (H1 2022: 38,800 m² or 34.9%). At 21.2 percentage points, it saw the biggest downturn in relative share across all sectors.

Retail was in last place with 12,500 m² or 9.6%, compared with 21,100 m² or 19% (-9.4 percentage points). Traditional retail and e-commerce each contributed half of the take-up in the retail category.

This might also be interesting for you:

To the market report Germany

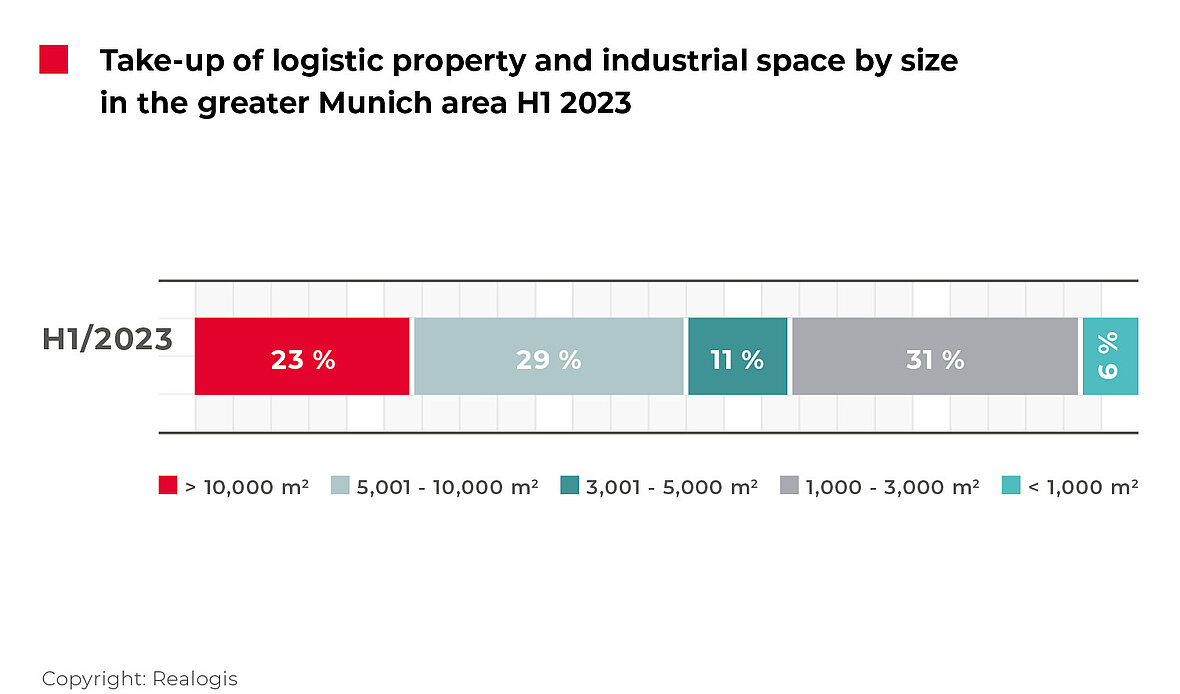

Smaller spaces between 1,000 and 3,000 m² remain number one

Spaces in the largest category of 10,001 m² and above maintained the previous year’s level and accounted for the third-most space in the first half of the year at 30,000 m² or a share of 23.1% (H1 2022: 27,500 m² or 24.8%). The single deal in this segment (Siemens Mobility GmbH) shows that this large size category comes into play less often in Munich – only two deals were seen in the same period of the previous year.

Larger to large spaces between 5,001 and 10,000 m² saw high market activity with take-up of 37,300 m² and a share of 28.7%, coming from 6,400 m² or 5.8% which led to the second place compared to the other categories in terms of take-up. The absolute growth is nearly sixfold. In relative terms, this size category grew the most with a rise of 22.9 percentage points. Currently, five of the six largest deals combined contribute significantly to the size category’s take-up (31,929 m² or 86%).

Typically, the 5,001 to 10,000 m² size category has been and still is very significant for the Munich market. However, its share continues to decline. From 2019 to 2022, this category was always in first place with almost half of the take-up, whereas it now provides just under a third of the take-up.

The stable 3,001 to 5,000 m² size category follows in fourth place with 14,600 m² or 11.2% (H1 2022: 16,200 m² or 14.6%).

Smaller spaces between 1,000 and 3,000 m² are still in first place with 40,300 m² or 31%, compared with 52,400 m² or 47.2% in H1 2022. However, they became less significant in both absolute (-23%) and relative terms (-16.2 percentage points).

The smallest spaces of less than 1,000 m² remain in fourth place with 7,800 m² or 6% (H1 2022: 8,600 m² or 7.7%).

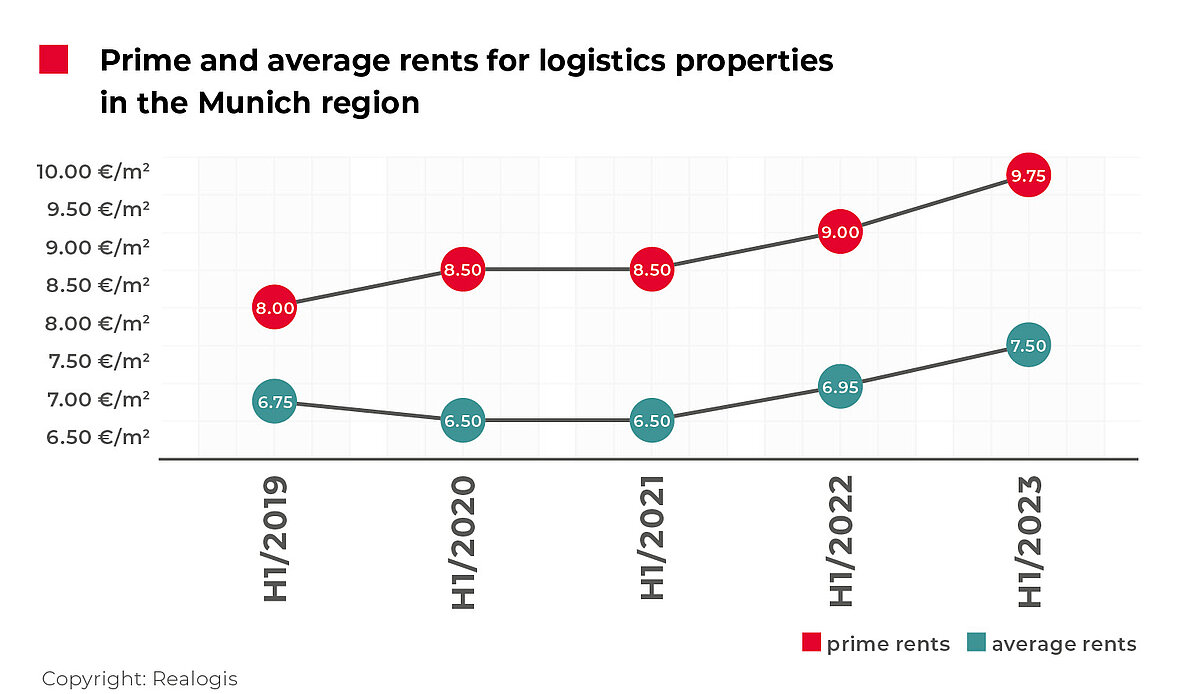

Prime rent set to rise again

According to our analysis, which is based exclusively on new contracts and thus does not account for extensions of existing leases, the prime rent for industrial and logistics properties and business parks in the Munich metropolitan region has risen compared with the first half of 2022 to EUR 9.75/m², its highest level to date. Prime rent was 11.4% higher than the five-year average of EUR 8.75/m². Because of the deals in new properties in the coming months, which were not yet on hand in the first half of the year, we assume that the prime rent will increase even further.

The average rent has also risen to an all-time high of EUR 7.50/m², which equates to growth of 7.9% on the previous year’s figure. The current level is around 9.6% above the five-year average of EUR 6.84/m².

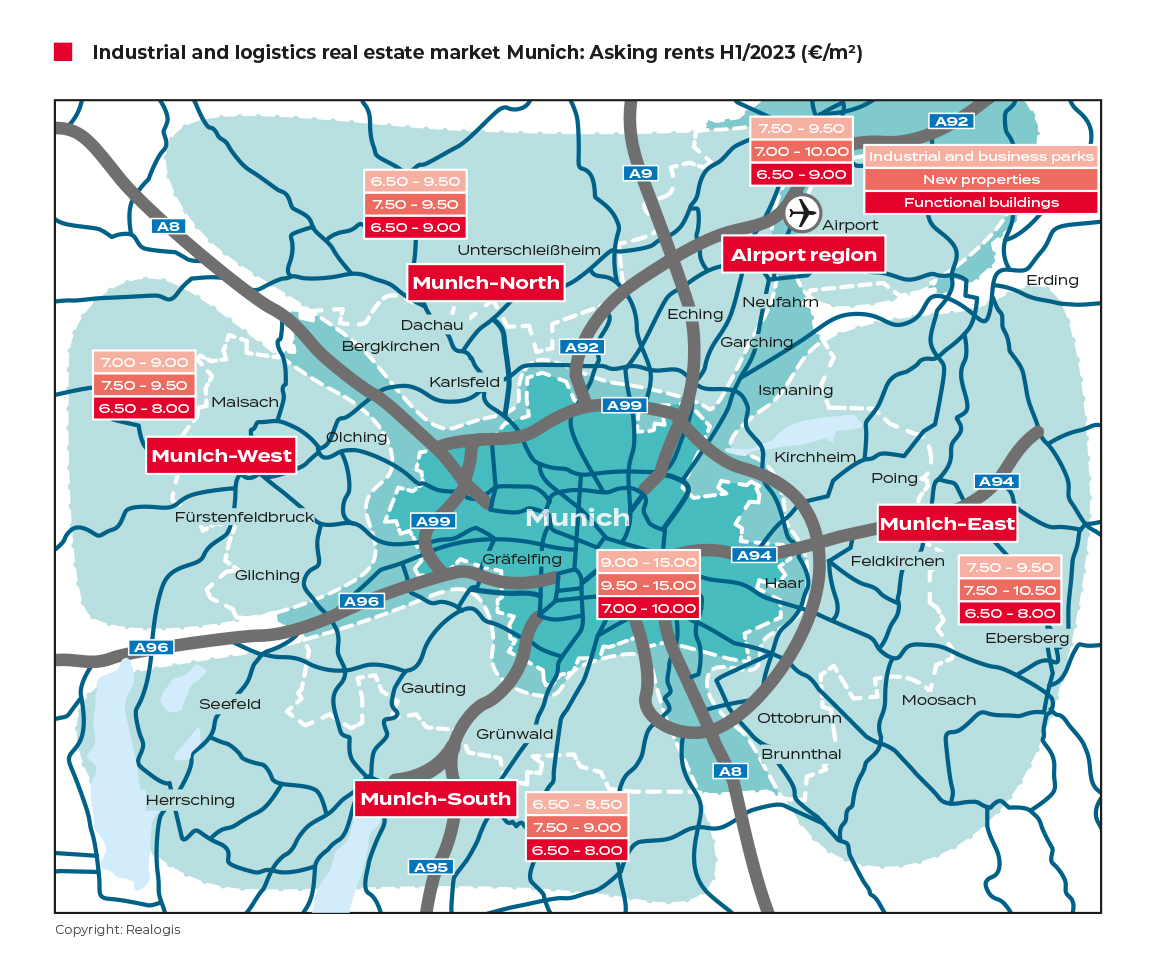

To the rent price maps:

Request the complete market report as PDF