ca. 2.700 qm Lager- / Produktionsfläche zu vermieten!

ID: 1005104DetailsLogistikflächen im GVZ Altenwerder kurzfristig zu vermieten

ID: 98106DetailsHOCHWERTIG | 650 m² HALLE | 800 m² AUSSTELLUNG

ID: 998947DetailsGarching, repräsentatives Produktionsgebäude mit hochwertigen Büroflächen

ID: 93135Detailsca. 400 m² große, ebenerdige Lager-Produktionshalle mit Meisterbüro in Top Lage

ID: 1036679DetailsDirekt am Autobahnkreuz Ulm/Elchingen - Neubau multifunktionaler Logistik- und Produktionsflächen

ID: 994300DetailsLOGISTIK | RAMPEN | FREIFLÄCHE

ID: 1008605DetailsLager-/Logistik | Neubau | Rampen | teilbar | ebenerdig

ID: 1016255DetailsGEWERBEPARK | ERSTBEZUG | TOP-LAGE

ID: 996681DetailsBremen, ca. 1.300 m² Lager-/ Logistikfläche zu vermieten

ID: 1032273DetailsMünchen - Nord, Hallen- und Freiflächen in Bestlage zu vermieten

ID: 101077DetailsPROVISIONSFREI | GEWERBEPARK | FLEXIBEL

ID: 1000973DetailsArnsdorf | ca. 9.000 m² | Lager & Logistik | Betonrampe & ebenerdig | teilbar ab 2.000

ID: 1009874DetailsRepräsentativer Gewerbepark

ID: 1005086DetailsHH-Altona, ca. 1.500 m² große, ebenerdige Hallenfläche mit Büro

ID: 1035432DetailsPRODUKTION | LAGER | RAMPE

ID: 991522DetailsGarching, Neubau von ca. 8.000 m² Lager-,Forschungs- und Bürofläche

ID: 1030576DetailsMunich-North, warehouse and office spaces for rent

ID: 1033335DetailsMunich-North, warehouse and office spaces for rent

ID: 1024609DetailsMunich-North, warehouse and office spaces for rent

ID: 1034331DetailsMunich-North, warehouse and office spaces for rent

ID: 1002692DetailsMunich-North, warehouse and office spaces for rent

ID: 1034768DetailsMunich-North, warehouse and office spaces for rent

ID: 1034670DetailsMunich-North, warehouse and office spaces for rent

ID: 1034767DetailsMunich-North, warehouse and office spaces for rent

ID: 1025539DetailsMunich-North, warehouse and office spaces for rent

ID: 1010949DetailsMunich-North, warehouse and office spaces for rent

ID: 1032598DetailsAugsburg, site with about 2.500 sqm for rent

ID: 9040DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031912DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031769DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031836DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1028145DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030724DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030615DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1023871DetailsGladback, warehousing space for wholesale or retail for rent

ID: 95769DetailsGladback, warehousing space for wholesale or retail for rent

ID: 1013489DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1025426DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1026621DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1022435DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1023380DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1014315DetailsNeuss, approx. 1,295 sqm warehouse space in a business park for rent

ID: 997156DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1017665DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1019585Details

Do you have a question? Leave your contact details here and we will call you back!

Market report Stuttgart 1st half of year 2022

- About the logistics market in the economic region

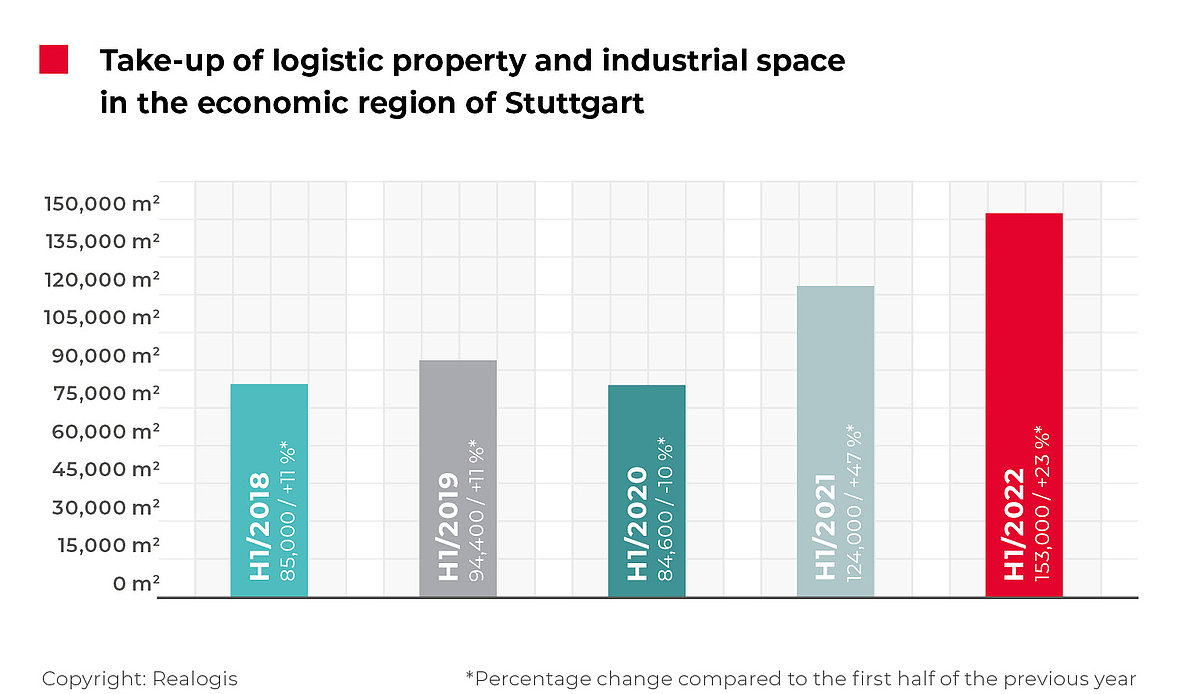

The market for industrial and logistics properties in the Stuttgart metropolitan region brought in a record result in the period from January to June 2022. According to our analysis 153,000 m² of space was newly let by all market participants combined in the first half of the year. The take-up in the first half of the previous year of 124,000 m² was topped by an impressive 23.4% and the current half-year result is the strongest since 2014. The five-year average of 108,200 m² was also exceeded by a significant 41.4%. Overall, we registered 29 deals by all market participants.

Der aktuelle Halbjahresabschluss ist beachtlich, da der Markt in den ersten Halbjahren 2017 bis 2020 eher an der 90.000er-Marke als an der 100.000er kratzte, ganz zu schweigen von dem Wert des vorläufigen Spitzenergebnisses von 150.000 m².

Die Verfügbarkeit von Großflächen und drei Top-Abschlüsse in dieser Kategorie sind unserer Einschätzung nach im ersten Halbjahr das Zünglein an der Waage gewesen. Ein Umstand, der für den Stuttgarter Markt durchaus etwas Besonderes ist. Zum Vergleich: Im Vorjahreszeitraum fand mit der Yahee GmbH über 20.800 m² lediglich ein Großabschluss statt.

Fakten

Stuttgart exceeds 150,000 m² mark

23.4% increase in take-up as against previous year

Strong result attributable to unusually large number of major deals

More than two-thirds of newly let space in existing properties

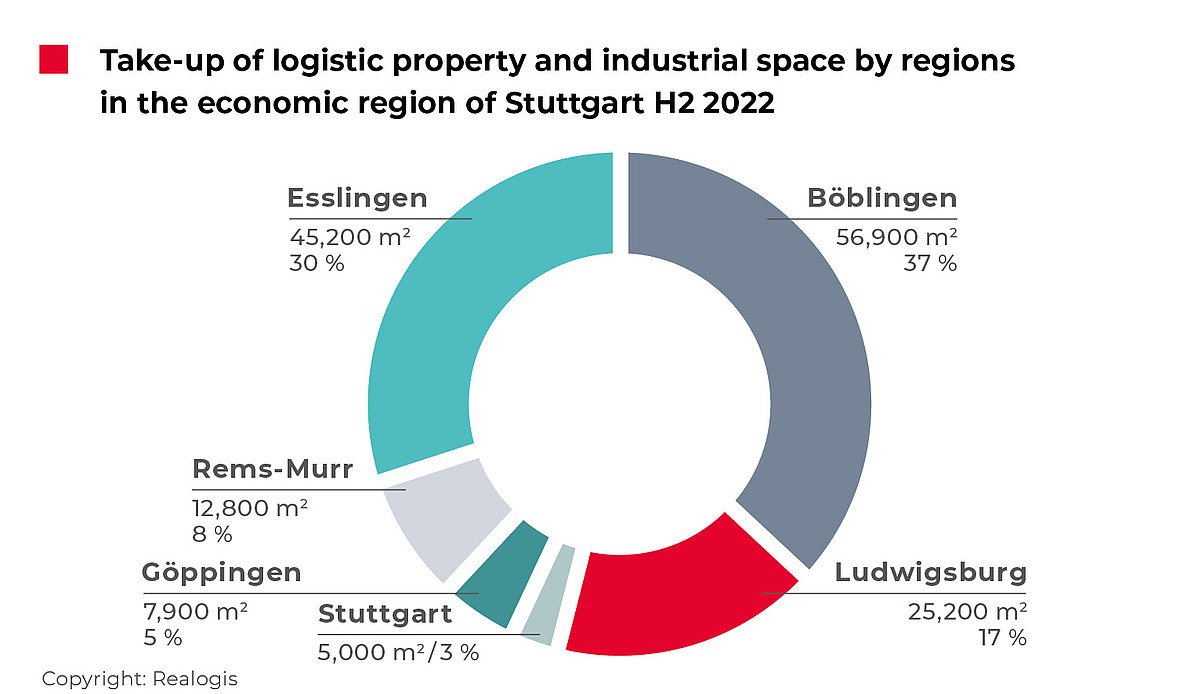

Böblingen takes top spot from Ludwigsburg

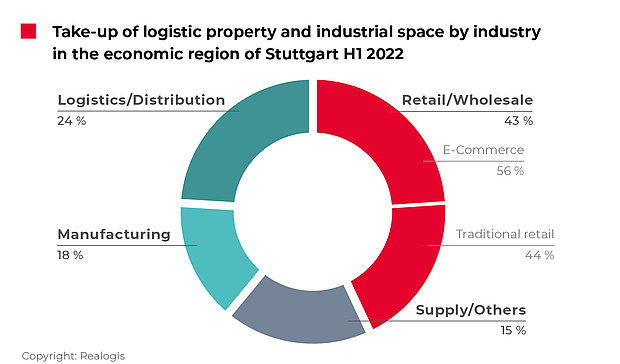

Retail/e-commerce leads sector ranking again

Average rent rises in contrast to previous year

More than 70% of newly let space was in existing properties

The strong take-up was mainly due to lettings in existing properties, which accounted for a share of 74.3% or 113,700 m². Roughly, a quarter of take-up was in new builds at 39,300 m².

Lessors with highest take-up

REWE, Böblingen district, ca. 35,000 m² (Existing property), Retail

E. Breuninger GmbH & Co. KG, Ludwigsburg district, ca. 22,282 m² (Existing property), E-commerce

Robert Bosch GmbH, Esslingen district, ca. 10,525 m² (New build), Manufacturing

Yusen Logistics, Esslingen district, ca. 9,087 m² (New build), Logistics/

distribution

Trumpf GmbH, Böblingen district, ca. 8,768 m² (New build), Manufacturing

In the first six months, Stuttgart was a clear tenant market. All lettings without exception were in properties owned by third parties.

Böblingen takes top spot from Ludwigsburg

The Böblingen district accounted for the highest take-up in the first half of the year at 56,900 m² or 37.2% (H1 2021: 27,000 m² or 21.8%) and is currently the region with the sharpest rise in relative importance at 15.4 percentage points.

Two of the top five deals in the reporting period are attributable to Böblingen. The biggest deal was signed by Rewe for over 35,000 m² in an existing property.

In addition, Trumpf GmbH rented around 8,768 m² in a new build. These two deals totalled approximately 43,768 m², representing three-quarters of take-up in the Böblingen district.

In second place is the Esslingen district with 45,200 m² or 29.5% (H1 2021: 30,300 m² or 24.4%, +5.1 percentage points). Two more of the top deals were located in this region, both in new builds: Robert Bosch GmbH leased around 10,525 m² and Yusen Logistics around 9,087 m². Together, they accounted for 19,612 m² or 43.4% of take-up there.

In third place is the Ludwigsburg district with 25,200 m² or 16.5%, which had taken first place in H1 2021 with 57,000 m² or 46%. It thus saw the biggest relative decline out of all regions, with pro-rata take-up decreasing by 29.5 percentage points year-on-year. However, the Ludwigsburg district managed to gain a top e-commerce company in E. Breuninger GmbH & Co. KG, which leased around 22,282 m² in an existing property.

In fourth place is the Rems-Murr district, which totalled 12,800 m² or 8.4% after coming last in the same period of the previous year, when there were no lettings. Last but one is Göppingen with 7,900 m² or 5.2% (H1 2021: 400 m² or 0.3%). In last place is the Stuttgart urban region with 5,000 m² or 3.3% (H1 2021: 9,300 m² or 7.5%).

Retail leads sector ranking again

As in the same period of the previous year, retail (including e-commerce) took the lead again out of all sectors. With take-up of 66,100 m², retail is responsible for 43.2% of total take-up (H1 2021: 49,400 m² or 39.8%; +3.4 percentage points).

The breakdown between retail and e-commerce was more even in the past half-year period than in the same period of the previous year. Currently, 55.5% (or 36,700 m²) is attributable to traditional retail and 44.5% (or 29,400 m²) to e-commerce. In the same period of the previous year, e-commerce had been well ahead with 71.9% or 35,500 m² as compared to traditional retail with 28.1% or 13,900 m².

The majority of take-up in the retail/e-commerce sector came from the two top deals with Rewe and Breuninger (together amounting to approximately 57,282 m² or 86.7%).

Next in the sector ranking comes logistics/distribution with a share of 23.6% or 36,100 m² (H1 2021: 28.4% or 35,200 m²). One of the top deals, Yusen Logistics, was attributable to this sector and contributed around a quarter of its take-up (25.2%).

In third place is manufacturing with 27,300 m² or 17.8% (H1 2021: 18,400 m² or 14.8%). This sector recorded two top deals with Robert Bosch GmbH and Trumpf GmbH. The miscellaneous category “Other” amounted to 23,500 m² or 15.4% (H1 2021: 21,000 m² or 16.9%).

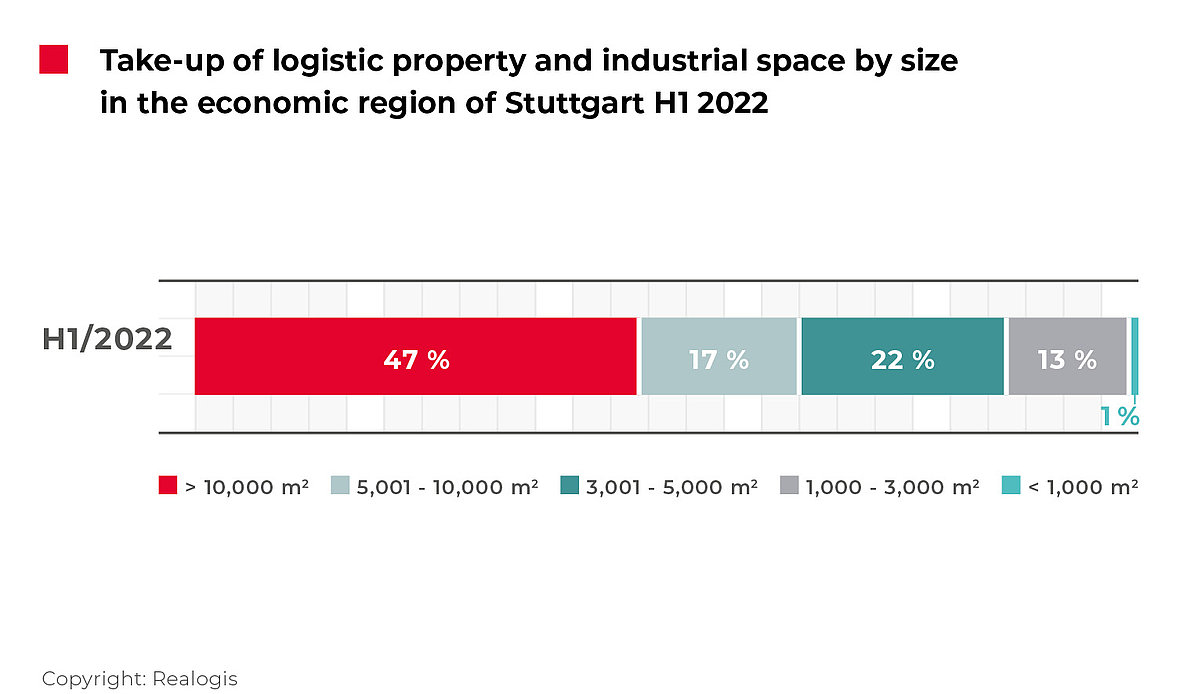

Size category: large spaces stand out in reporting period

In the first half of the year, the size category of 10,001 m² and up accounted for 71,200 m² or 46.5% of the total take-up generated by all market participants in the Stuttgart metropolitan region. In the previous year, this category of large spaces had been in third place with 21,900 m² or 17.7%. It thus increased by a substantial 28.9 percentage points in terms of relative importance, while its take-up more than quadrupled in absolute terms.

This might also be interesting for you:

To the market report Germany

However, all other size categories recorded year-on-year decreases in terms of their relative importance. Larger spaces between 5,001 and 10,000 m² accounted for 26,400 m² or 17.3% (third place). In the previous year, they had been in first place with 46,600 m² or 37.6%, meaning that they lost the most relative importance out of all size categories at 20.3 percentage points.

Medium-sized spaces between 3,001 and 5,000 m² took second place with 33,500 m² or 21.9% (H1 2021: 30,900 m² or 24.9%). Small to medium-sized spaces of between 1,000 and 3,000 m² ended up second-to-last with 19,800 m² or 12.9% (H1 2021: 20,300 m² or 16.4%), while the smallest spaces of less than 1,000 m² brought up the rear, as in the same period of the previous year, with 2,100 m² or 1.4% (H1 2021: 4,300 m² or 3.5%).

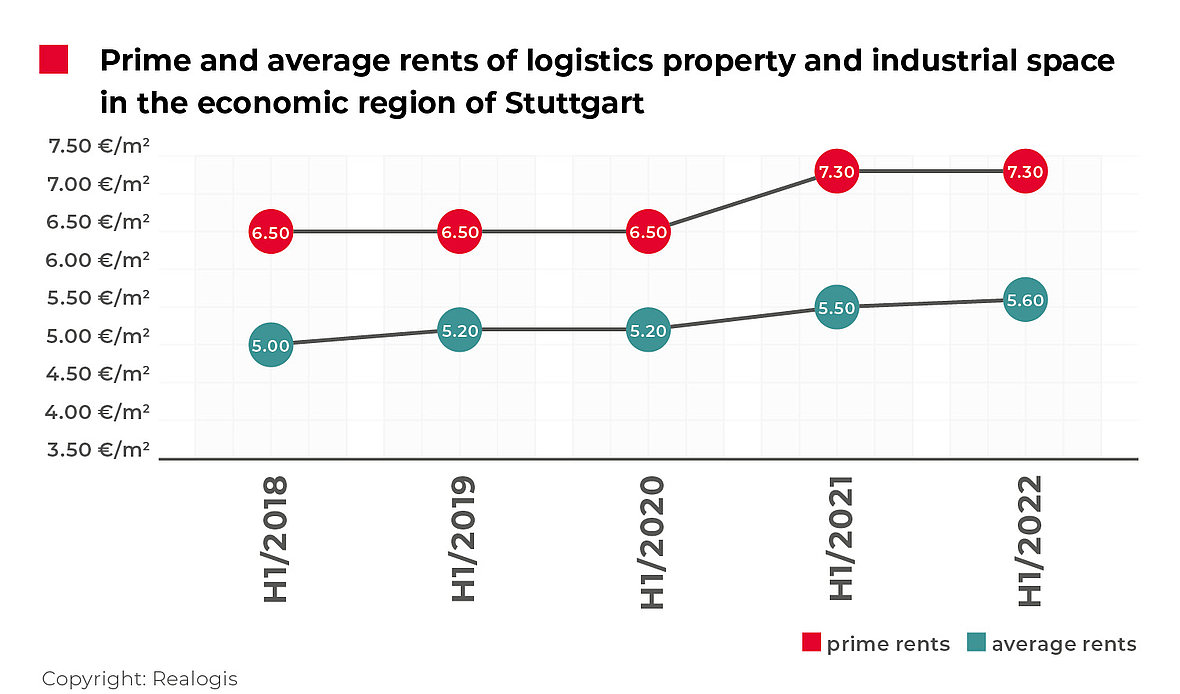

Average rent rises

The prime rent for modern industrial and logistics properties remained at the previous year’s level of €7.30/m², which represents the highest level to date for the first half of a year and resulted from an increase of 12.3% to €7.30/m² in the first half of 2021 (coming from €6.50/m² in H1 2020). The five-year average of €6.82/m² was exceeded by 7%.

The average rent on the Stuttgart market was much more dynamic, rising for the fourth time in the first halves of the past five years. It is currently at €5.60/m², representing an increase of 1.8% (H1 2021: €5.50/m², +5.8%). Average rents are 5.7% higher than the five-year average of €5.30/m².

To the rent price maps:

Order the complete market report as PDF