HOCHWERTIG | 650 m² HALLE | 800 m² AUSSTELLUNG

ID: 998947DetailsGarching, repräsentatives Produktionsgebäude mit hochwertigen Büroflächen

ID: 93135Detailsca. 400 m² große, ebenerdige Lager-Produktionshalle mit Meisterbüro in Top Lage

ID: 1036679DetailsDirekt am Autobahnkreuz Ulm/Elchingen - Neubau multifunktionaler Logistik- und Produktionsflächen

ID: 994300DetailsLOGISTIK | RAMPEN | FREIFLÄCHE

ID: 1008605DetailsLager-/Logistik | Neubau | Rampen | teilbar | ebenerdig

ID: 1016255DetailsGEWERBEPARK | ERSTBEZUG | TOP-LAGE

ID: 996681DetailsBremen, ca. 1.300 m² Lager-/ Logistikfläche zu vermieten

ID: 1032273DetailsMünchen - Nord, Hallen- und Freiflächen in Bestlage zu vermieten

ID: 101077DetailsPROVISIONSFREI | GEWERBEPARK | FLEXIBEL

ID: 1000973DetailsArnsdorf | ca. 9.000 m² | Lager & Logistik | Betonrampe & ebenerdig | teilbar ab 2.000

ID: 1009874DetailsRepräsentativer Gewerbepark

ID: 1005086Detailsca. 1.350 m² große, ebenerdige Hallenfläche mit Büro

ID: 1035432DetailsPRODUKTION | LAGER | RAMPE

ID: 991522DetailsGarching, Neubau von ca. 8.000 m² Lager-,Forschungs- und Bürofläche

ID: 1030576DetailsMunich-North, warehouse and office spaces for rent

ID: 1033335DetailsMunich-North, warehouse and office spaces for rent

ID: 1024609DetailsMunich-North, warehouse and office spaces for rent

ID: 1034331DetailsMunich-North, warehouse and office spaces for rent

ID: 1002692DetailsMunich-North, warehouse and office spaces for rent

ID: 1034768DetailsMunich-North, warehouse and office spaces for rent

ID: 1034670DetailsMunich-North, warehouse and office spaces for rent

ID: 1034767DetailsMunich-North, warehouse and office spaces for rent

ID: 1025539DetailsMunich-North, warehouse and office spaces for rent

ID: 1010949DetailsMunich-North, warehouse and office spaces for rent

ID: 1032598DetailsAugsburg, site with about 2.500 sqm for rent

ID: 9040DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031912DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031769DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031836DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1028145DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030724DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030615DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1023871DetailsGladback, warehousing space for wholesale or retail for rent

ID: 95769DetailsGladback, warehousing space for wholesale or retail for rent

ID: 1013489DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1025426DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1026621DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1022435DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1023380DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1014315DetailsNeuss, approx. 1,295 sqm warehouse space in a business park for rent

ID: 997156DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1017665DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1019585Details

Do you have a question? Leave your contact details here and we will call you back!

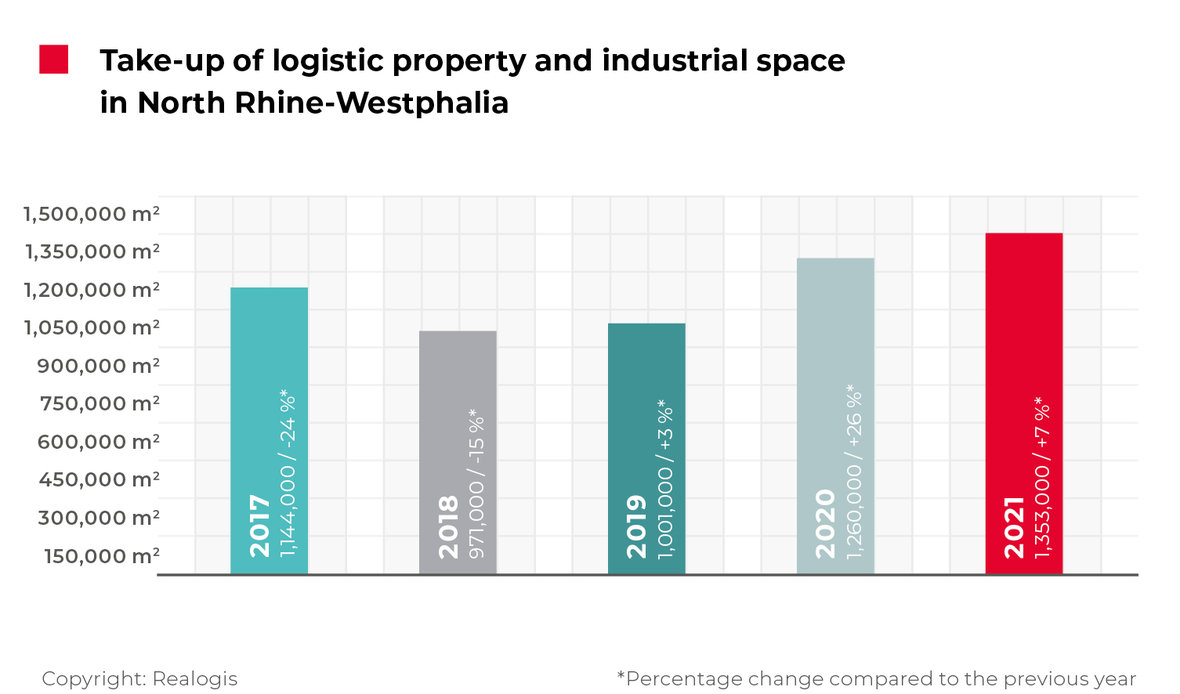

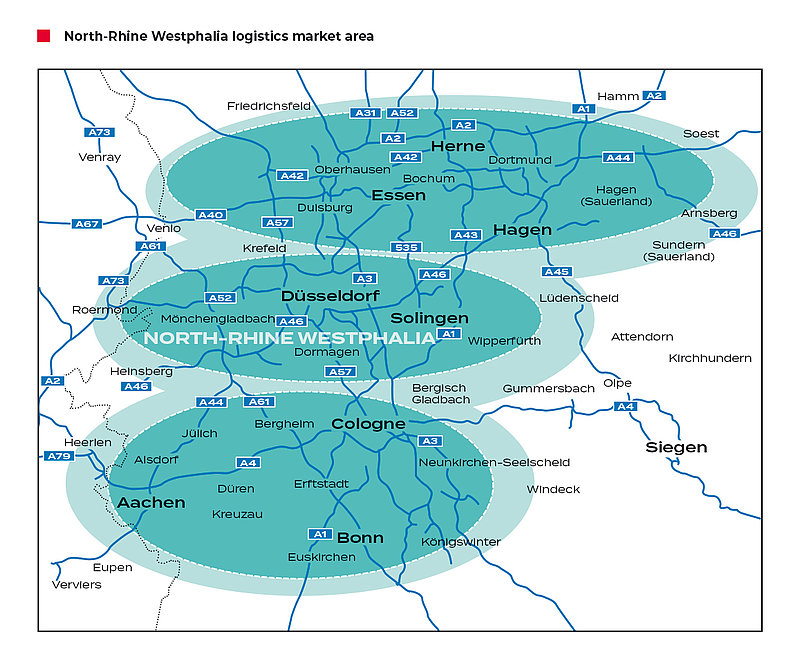

Market report North Rhine-Westphalia for the year 2021

- About the logistics market in the economic region

NRW logistics property market grows – albeit with the handbrake on

According to our analysis, the industrial and logistics property market in North Rhine-Westphalia (NRW) performed well in the past year. Logistics and industrial take-up across all market participants in the NRW market area amounted to 1.35 million m² in 2021. This corresponds to an increase of 7.4% (2020: 1.26 million m²). Underlining the positive trend in the last three years, the latest result is an impressive 18.1% above the five-year average of 1.15 million m².

Demand remains extremely stable and take-up is at a normal level. However, demand is outstripping supply – significantly more space could have been rented out and companies located if more space had been available.

Facts

NRW logistics property market grows by 7.4% year-on-year in 2021

Retail leads the way – e-commerce yet to reach its full potential

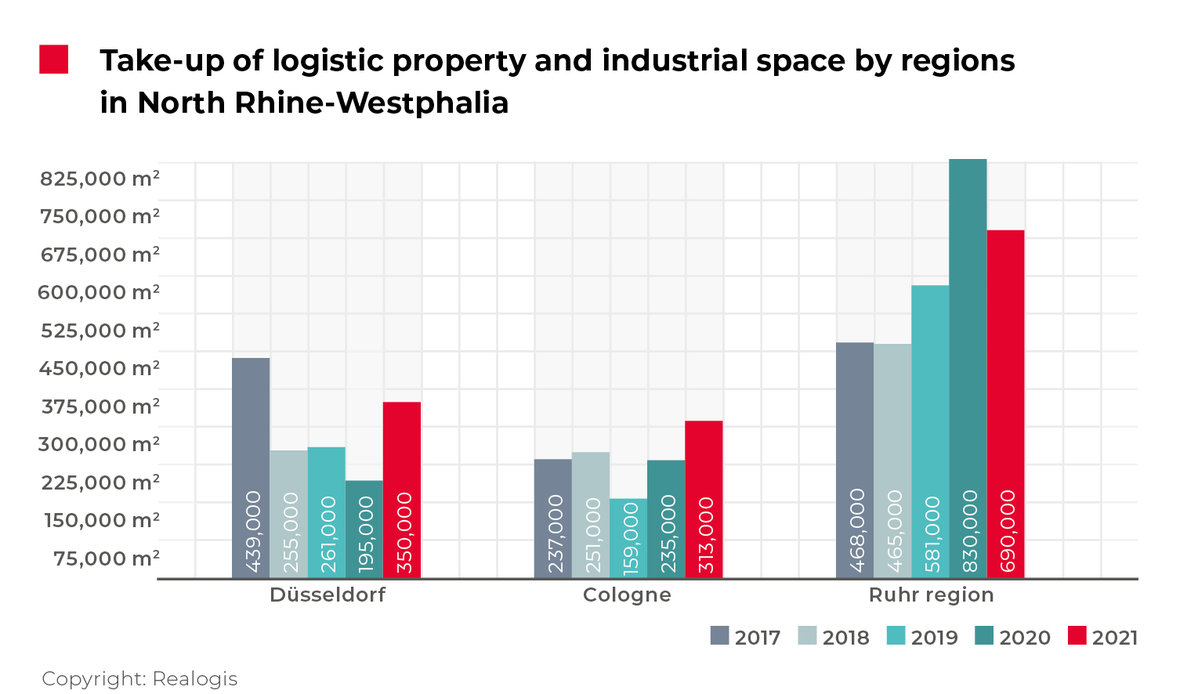

Ruhr region sub-market reinforces leading position and accounts for every second square metre let

Düsseldorf and Cologne increase their market share

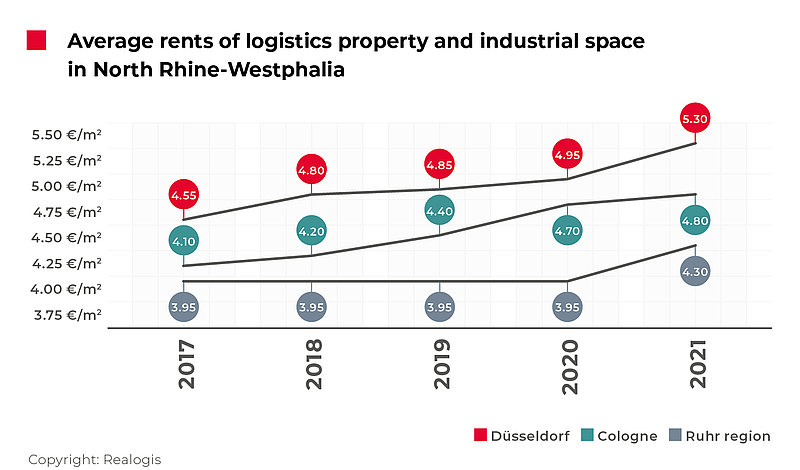

Prime rents up across all three sub-markets

Forecast for 2022: Huge run on existing properties

Ruhr region again contributes half of total take-up

As in the previous year, the Ruhr region made the biggest contribution to the result for the year with a share of 51%. This means the Ruhr region accounted for more than every second square metre let in the NRW core markets in 2021, thus maintaining its leading position. At 690,000 m², however, the strongest sub-market in NRW saw a proportionate reduction in take-up compared with the previous year.

The relative importance of the Ruhr region within NRW had been rising since 2017, peaking at 65.9% or 830,000 m² in 2020, whereas the latest figure represents a decline of 14.9 percentage points. Total take-up in the Ruhr region has also fallen by 16.9% in the past year.

Düsseldorf and Cologne both increased their market share. In the period from January to December, Düsseldorf accounted for 25.9% or 350,000 m² in take-up (2020: 15.5%, 195,000 m²), whereas the corresponding figures for Cologne were 23.1% and 313,000 m² (2020: 18.7%, 235,000 m²).

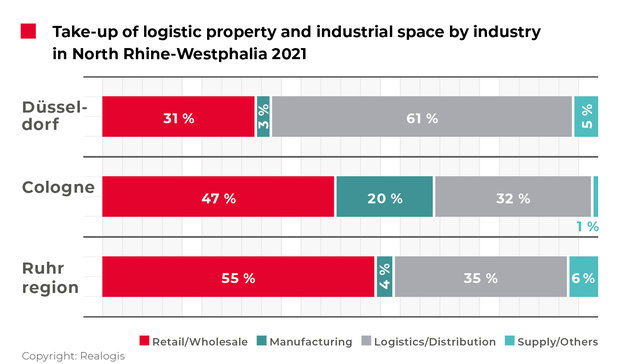

Sector comparison: Retail leads the way – buffer stocks on the rise

At 47% or 634,450 m², retail accounted for almost every second square metre let in 2021. Having placed second in the previous year, this makes retail the leading sector in 2021 (2020: 553,850 m² or 44%).

Germany is still some way from reaching its full potential when it comes to take-up by online retailers. Retail companies have been ordering more goods since the onset of the supply difficulties in Asia. Because consumers quickly turn their back on online stores that are unable to fulfil orders, the result is that warehouses are filling up. As such, retail companies and their logistics specialists are acting cautiously, building up buffers and calling up even more goods that need to be stored in the meantime.

Four of the nine lessors with the highest take-up in 2021 belong to this category, which collectively accounted for a total of 204,000 m² or 32% of retail take-up in NRW. This includes the biggest deal, which involved the e-commerce company BBG (Chal-Tec) letting 105,000 m² of space at a new build in Werne in the Ruhr region. Other major deals included the retail companies Lekkerland (28,000 m²) in Kerpen, P&C (45,000 m²) in Cologne, and Dokas (26,000 m²) in the Ruhr region.

Logistics/ distribution took second place with total take-up of 555,800 m² (41%). Having ranked first in the previous year (2020: 598,050 m² or 47%), this meant the segment’s market share fell by 6 percentage points. The positive result was thanks in particular to major deals in the Düsseldorf metropolitan region: Rhenus (85,000 m²), Ontaro (22,000 m²) and Yusen (20,000 m²) collectively accounted for space of 127,000 m² (or 22.8% of the logistics/ distribution take-up in NRW).

This might also be interesting for you:

To the market report Germany

After taking last place in the previous year, manufacturing was ranked third with take-up of 100,700 m² or 7% (2020: 47,450 m² or 4%). The market was dominated by the major deal concluded by WEG in the Cologne market (Kerpen), which accounted for around half of the sector’s take-up at 50,000 m². Thanks to this deal, manufacturing saw the strongest growth in market share among all the sectors at 3.7 percentage points.

The miscellaneous category “Other” slipped from third place in the previous year (2020: 60,650 m², 5%) to last place with take-up of 62,050 m² and a market share of 5%. One of the top deals, MT Deutschland with 22,000 m² in Voerde (Ruhr region), was allocated to this category.

Forecast for 2022

We will see continued high demand at a healthy level in 2022. However, the shortage of supply in particular means that the NRW industrial and logistics property market will be unable to repeat the same letting performance as in past years. We expect this year to see another massive run on existing properties and properties under construction. In turn, this will have a big impact on rent increases. All of the markets will be affected – even the Ruhr region, which had previously been the exception to the rule. This development has now become a common thread throughout all of the core markets in North Rhine-Westphalia.

Take-up in the Düsseldorf sub-market grows by +79.5%

Following the slump in the previous year, 2021 saw the best full-year result for the Düsseldorf industrial and logistics property market since 2017. Take-up grew by an impressive 79.5% to 350,000 m², meaning that 155,000 m² more space was let than in the previous year across all market participants. This figure was also 16.7% higher than the five-year average of 300,000 m².

In normal years, the Düsseldorf market sees take-up of up to 260,000 m². However, recent years have seen a downturn on the Düsseldorf market due to a shortage of large spaces and corresponding deals. Some existing properties came onto the market after reaching the end of their letting cycle in 2021 in addition to new builds. All of them were quickly and efficiently taken up by the various user groups. If the market had had 400,000 m² in available space in 2021, this would have been fully let – there is significant excess demand.

Lessors with the highest take-up in the Düsseldorf market area:

Rhenus, Wesel, approx. 85,000 m² (New build BTS), Logistics

Ontaro, Krefeld, approx. 22,000 m² (New build), Logistics

Yusen, Düsseldorf, approx. 20,000 m² (New build BTS), Logistics

The leading sector in the Düsseldorf logistics and industrial property market is logistics/ distribution, with a market share of 61% or 213,500 m². The logistics/ distribution sector recorded significant growth in absolute terms, more than doubling its result from 2020 (93,600 m² or +128%), as well as in terms of its relative market share (+13 percentage points).

At 127,000 m², the top deals made a particularly strong contribution to the logistics/ distribution result. With all three of the top deals falling within this category, they collectively accounted for 60% of take-up in the sector: Rhenus with 85,000 m² in a new build BTS in Wesel, Ontaro with 22,000 m² in a new build in Krefeld, and Yusen with 20,000 m² in a new build BTS in Düsseldorf.

As in the previous year, retail was the second-largest sector at 31% or 108,500 m². However, its relative market share declined by a substantial 14 percentage points (2020: 45% of total take-up) despite the fact that take-up increased by around 24% in absolute terms from the prior-year figure of 87,750 m². Retail was followed by the miscellaneous category “Other” (17,500 m² or 5%) and manufacturing (10,500 m² or 3%).

The prime rent in the Düsseldorf market increased by 5.9%, the highest percentage rise since 2014. This took it to a new provisional high of EUR 6.30/m² (after EUR 5.95/m² at the end of 2020), meaning that the upward trend recorded in previous years intensified. The five-year average of EUR 5.84/m² was exceeded by 7.9%.

The average rent followed the same pattern as the prime rent but with even stronger growth, climbing 7.1% to a new provisional high of EUR 5.30/m² (after EUR 4.95/m² in the previous year). This was 8.4% higher than the five-year average of EUR 4.89/m².

Cologne sub-market benefits from existing space becoming vacant

Take-up on the Cologne industrial and logistics property market increased by 33.2%, from 235,000 m² at the end of 2020 to 313,000 m² in 2021. This strong result also exceeded the five-year average of 239,000 m² by an impressive 31%.

Among other things, the growth in take-up was due to space with expiring leases being re-let without substantial vacancies. Additionally, several new builds were added to the market in the past year. Demand is also outstripping supply in the Cologne metropolitan region.

As in the previous year, the strongest sector was retail at 47% or 146,450 m². Although retail saw absolute growth of 25% compared with the figure of 117,500 m² in 2020, its relative market share slipped by three percentage points compared with the other sectors.

The top deals made a substantial contribution of 73,000 m² (49.8% of total take-up in the retail sector). This included P&C with 45,000 m² in Bedburg and Lekkerland with 28,000 m² as both companies moved into built-to-suit new builds.

Lessors with the highest take-up in the Cologne market area:

WEG, Kerpen, approx. 50,000 m² (New build BTS), Manufacturing

P&C, Bedburg , approx. 45,000 m² (New build BTS), Retail

Lekkerland, Kerpen, approx. 28,000 m² (New build BTS), Retail

As in the previous year, second place was taken by logistics/ distribution at 100,800 m² or 32%, compared with 72,850 m² or 31% in 2020. The sector recorded absolute growth of 38%, while its market share remained essentially unchanged (+1 percentage point). Manufacturing ranked third with take-up of 62,600 m² or 20% compared with 35,250 m² or 15% in the previous year, making it the industry with the biggest increase in market share (in percentage points). The miscellaneous category “Other” ranked last with take-up of 3,150 m² and a market share of 1% (2020: 9,400 m², 4%).

The prime rent in the Cologne market area increased only slightly by 1.7% to reach a new provisional high of EUR 5.95/m². The prime rent had previously seen stronger growth since 2019, but while the positive trend is continuing, it appears to be slowing at present. The five-year average increased by 3.2% to EUR 5.50/m² and was exceeded by 8%.

The average rent also reached a new provisional high of EUR 4.80/m², an increase of 2.1%. With the average rent having increased by 6.8% in 2020 (from EUR 4.40/m² in 2019 to EUR 4.70/m²), this means the upturn seen in recent years is also slowing. The five-year average of EUR 4.44/m² was exceeded by 8%.

Ruhr region loses momentum due to shortage of space

The industrial and logistics property market in the Ruhr region failed to maintain the positive momentum recorded in previous years with take-up declining substantially by -16.9% to 690,000 m², although this still represents the third-best figure since our records started. The five-year average of 606,800 m² was exceeded by 13.7% in the past year. This was down slightly on the previous year, when the take-up of 830,000 m² exceeded the average of 672,800 m² by 23.4%.

The strongest sector in 2021 was retail with take-up of 379,500 m² and a market share of 55%, having placed second in 2020 with 348,600 m² and 42%. With growth of 13 percentage points, retail saw the biggest upturn in market share across all sectors as well as increasing slightly in absolute terms (by 9%, from 348,600 m² to 379,500 m²).

The good performance of the sector was thanks in particular to the biggest deal of the year in NRW – the 105,000 m² new build let by the e-commerce company BBG (Chal-Tec) in Werne – as well as Dokas letting 26,000 m² in a new property in Gelsenkirchen. Taken together, these deals accounted for 131,000 m² or 35% of total take-up in the retail category.

Lessors with the highest take-up in the Ruhr region market area

BBG (Chal-Tec), Werne, approx. 105,000 m² (New build), Retail

Rhenus, Bönen, approx. 60,000 m² (New build), Logistics/distribution

Dokas, Gelsenkirchen, approx. 26,000 m² (New build), Retail

Second place was taken by logistics/ distribution at 241,500 m² or 35%, compared with first place in 2020 with 431,600 m² and 52%. At -17 percentage points, logistics/ distribution saw the biggest downturn in market share across all sectors as well as falling sharply in absolute terms (-44% or -190,100 m²). The main deal was concluded between Rhenus Logistik and Dietz AG for over 60,000 m² of newly built space at the former Woolworth site in Bönen.

Third place again belonged to the “Other” category with 41,400 m² and 6%, after 41,500 m² and 5% in the previous year. Just over half of this figure (53%) was attributable to the deal by MT Deutschland for 22,000 m² of space in a new build BTS in Voerde, without which “Other” would have been ranked last. Instead, manufacturing took last place with 27,600 m² and 4%.

The growth in prime rents in recent years continued and accelerated slightly. The prime rent increased by 4.8% to a new provisional high of EUR 5.50/m². The only time we previously recorded a larger rise was in 2015 (when the prime rent climbed by 9.3%, from EUR 4.30/m² to EUR 4.70/m²). The five-year average of EUR 5.13/m² was exceeded by 7.2%.

Having remained constant at EUR 3.95/m² since 2018, the average rent increased substantially by 8.9% to EUR 4.30/m². This is the highest figure recorded since 2014. The five-year average amounted to EUR 4.02/m² and was exceeded by 7%.

To the rent price maps:

Order the complete market report as PDF

NRW - 2021