HOCHWERTIG | 650 m² HALLE | 800 m² AUSSTELLUNG

ID: 998947DetailsGarching, repräsentatives Produktionsgebäude mit hochwertigen Büroflächen

ID: 93135Detailsca. 400 m² große, ebenerdige Lager-Produktionshalle mit Meisterbüro in Top Lage

ID: 1036679DetailsDirekt am Autobahnkreuz Ulm/Elchingen - Neubau multifunktionaler Logistik- und Produktionsflächen

ID: 994300DetailsLOGISTIK | RAMPEN | FREIFLÄCHE

ID: 1008605DetailsLager-/Logistik | Neubau | Rampen | teilbar | ebenerdig

ID: 1016255DetailsGEWERBEPARK | ERSTBEZUG | TOP-LAGE

ID: 996681DetailsBremen, ca. 1.300 m² Lager-/ Logistikfläche zu vermieten

ID: 1032273DetailsMünchen - Nord, Hallen- und Freiflächen in Bestlage zu vermieten

ID: 101077DetailsPROVISIONSFREI | GEWERBEPARK | FLEXIBEL

ID: 1000973DetailsArnsdorf | ca. 9.000 m² | Lager & Logistik | Betonrampe & ebenerdig | teilbar ab 2.000

ID: 1009874DetailsRepräsentativer Gewerbepark

ID: 1005086Detailsca. 1.350 m² große, ebenerdige Hallenfläche mit Büro

ID: 1035432DetailsPRODUKTION | LAGER | RAMPE

ID: 991522DetailsGarching, Neubau von ca. 8.000 m² Lager-,Forschungs- und Bürofläche

ID: 1030576DetailsMunich-North, warehouse and office spaces for rent

ID: 1033335DetailsMunich-North, warehouse and office spaces for rent

ID: 1024609DetailsMunich-North, warehouse and office spaces for rent

ID: 1034331DetailsMunich-North, warehouse and office spaces for rent

ID: 1002692DetailsMunich-North, warehouse and office spaces for rent

ID: 1034768DetailsMunich-North, warehouse and office spaces for rent

ID: 1034670DetailsMunich-North, warehouse and office spaces for rent

ID: 1034767DetailsMunich-North, warehouse and office spaces for rent

ID: 1025539DetailsMunich-North, warehouse and office spaces for rent

ID: 1010949DetailsMunich-North, warehouse and office spaces for rent

ID: 1032598DetailsAugsburg, site with about 2.500 sqm for rent

ID: 9040DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031912DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031769DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031836DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1028145DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030724DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030615DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1023871DetailsGladback, warehousing space for wholesale or retail for rent

ID: 95769DetailsGladback, warehousing space for wholesale or retail for rent

ID: 1013489DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1025426DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1026621DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1022435DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1023380DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1014315DetailsNeuss, approx. 1,295 sqm warehouse space in a business park for rent

ID: 997156DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1017665DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1019585Details

Do you have a question? Leave your contact details here and we will call you back!

Market report Munich 1st half of year 2022

- About the logistics market in the economic region

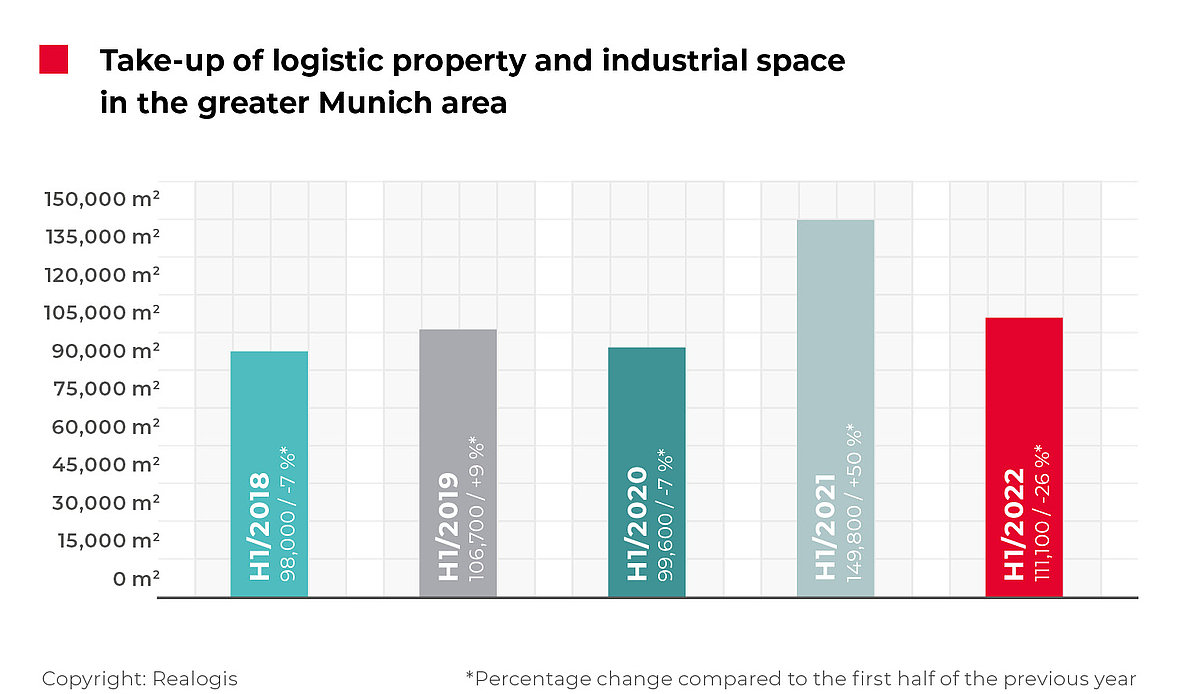

According to our observation, all market participants in the Munich metropolitan region generated take-up of industrial and logistics properties for rental of 111,000 m² in the first six months of 2022. Consequently, take-up in the first six months was down by 25.8% year-on-year, from 149,800 m² in H1 2021. It is now just under 1.7% below the five-year average of 113,040 m².

According to our evaluation, this result and the significant decrease illustrate the acute shortage of new space and available existing properties in the Greater Munich area. We are seeing extremely strong demand from all user groups. However, letting of large spaces has stagnated, and it is clear that not enough logistics space is currently being built in the Munich metropolitan region for retail, industry and their logistics service providers.

In addition we see that innovative service concepts such as online supermarkets are entering the market from the food and non-food sectors. They are becoming increasingly attractive to consumers – especially the older population. These concepts require more space. Therefore, more land has to be designated for e-food and non-e-food logistics within a 100 km radius of Munich.

Fakten

- Existing space dominates at over 70%

No big-box deals, just under 30% of space in traditional business parks

Third-party users to the fore, way ahead of owner-occupiers

Just under half of take-up and three of the top 5 deals concluded in Munich West

Manufacturing category tops the sector ranking

Decrease in take-up by e-commerce

Smaller spaces between 1,000 and 3,000 m² account for almost half of take-up

82,000 m² of new space under development

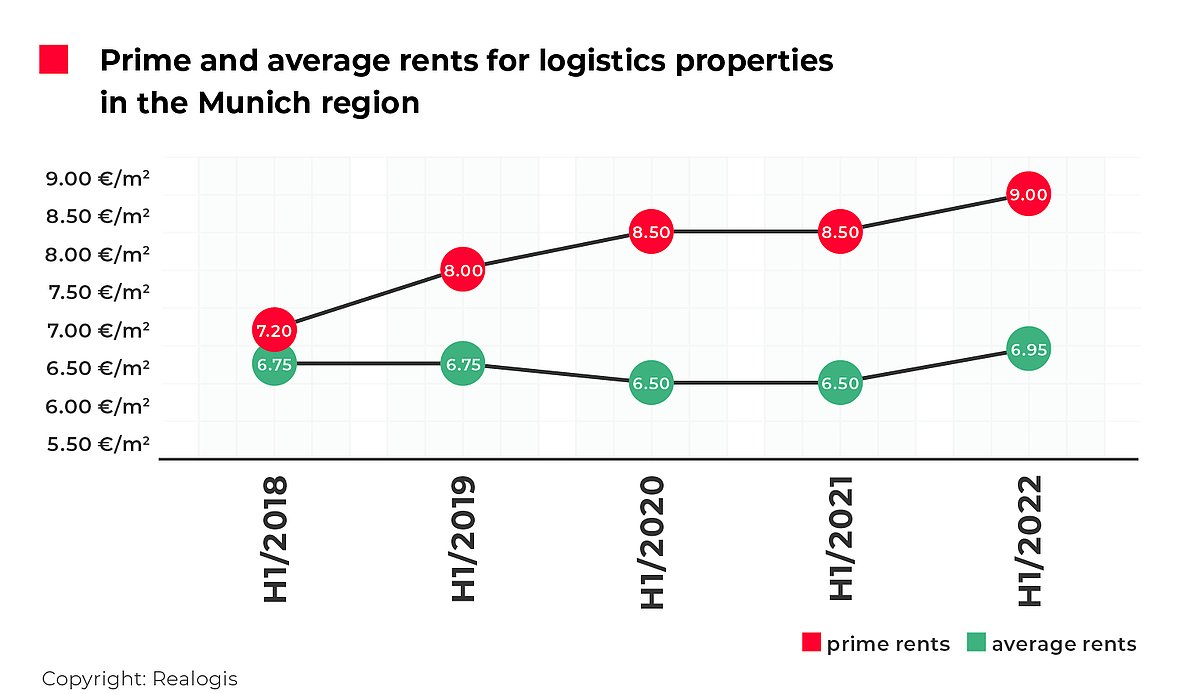

Highest level to date for prime rent at EUR 9.00/m² and average rent at EUR 6.95/m²

Existing space dominates at over 70%

The percentage of new-build and existing properties was similar to the same period of the previous year. New builds accounted for less than a third of space (H1 2022: 32,600 m² or 29.3%; H1 2021: 33,700 m² or 22.5%). The biggest deal was concluded by the logistics service provider DHL, which is constructing a stand-alone property in Germering for its own use.

Lessors with highest take-up

DHL, Munich West, approx. 14.000 m² (New build, owner-occupied), Logistics

k.A., Munich West, approx. 12.500 m² (Development of existing property), Industry (pharmaceuticals)

TopTica Photonics AG, Munich West, approx. 5.800 m² (Existing property), Industry

seHuber GmbH & Co KG, Munich East, approx. 4.600 m² (Existing property), Retail

Bravobike GmbH, Munich North, approx. 3.520 m² (Existing property), Retail

At over 70%, existing properties dominated (H1 2022: 78,500 m² or 70.7%; H1 2021: 101,600 m² or 67.8%). By contrast, there was no take-up for brownfield sites between January and June 2022. In the first half of 2021, their share was 9.7% or 14,500 m².

Overall, we registered 44 deals on the Munich market, compared with 69 in the same period of the previous year. 12 of the new contracts have a short to medium term of 1–4 years, 18 have a longer term of 5–9 years, and 14 have a long term of 10 years or more.

The vast majority of space was rented in properties that did not belong to the users (95,700 m² or 86.1%). Owner-occupiers were responsible for only 13.9% of take-up, or 15,400 m².

New categorisation: No big-box deals, just under 30% of space in traditional business parks

No big-box logistics lettings – i.e. the category of large spaces of 10,000 m² or more, with logistics as the main type of use and an office share of no more than 20% – were in evidence on the Munich market in the first half of 2022. At 33,100 m², traditional business parks accounted for 29.8% of deals. The majority of leases – 67.8%, covering 75,300 m² – were concluded for individual properties rather than business parks or the big-box category.

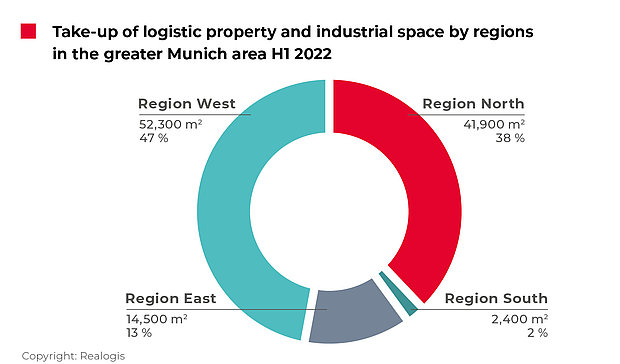

High take-up in Munich West

The region with the highest take-up in the first half of 2022 was the West region with 52,300 m², a share of 47.1%. Having come second in the previous year with 32,200 m² or 21.5%, this was the region with the sharpest rise in relative importance (25.6 percentage points). It is also the only region that saw an overall upturn in take-up compared with the strong first half of the previous year (up by 62.4% from 32,200 m² to 52,300 m²).

The biggest three of the top five deals were made in the West region. These deals amounted to approx. 30,800 m², or 58.9% of take-up in the West region:

DHL for approx. 14,000 m² in new space

A pharmaceutical company for approx. 11,000 m² in an existing property

- TopTica Photonics AG for approx. 5,800 m² in an existing property

The North region, the leader a year ago with 65,900 m² or 44%, came second with 41,900 m² or 37.7% (a decrease of 6.3 percentage points in terms of relative importance). The smallest top deal, by Bravobike GmbH in an existing property covering approx. 3,520 m², was concluded in this region.

As last year, the East region came third, with 14,500 m² or 13%. The only one of the top deals here was for an existing property, with approx. 4,600 m², concluded by seHuber GmbH & Co KG. The South region brought up the rear with 2,400 m² or 2.2%.

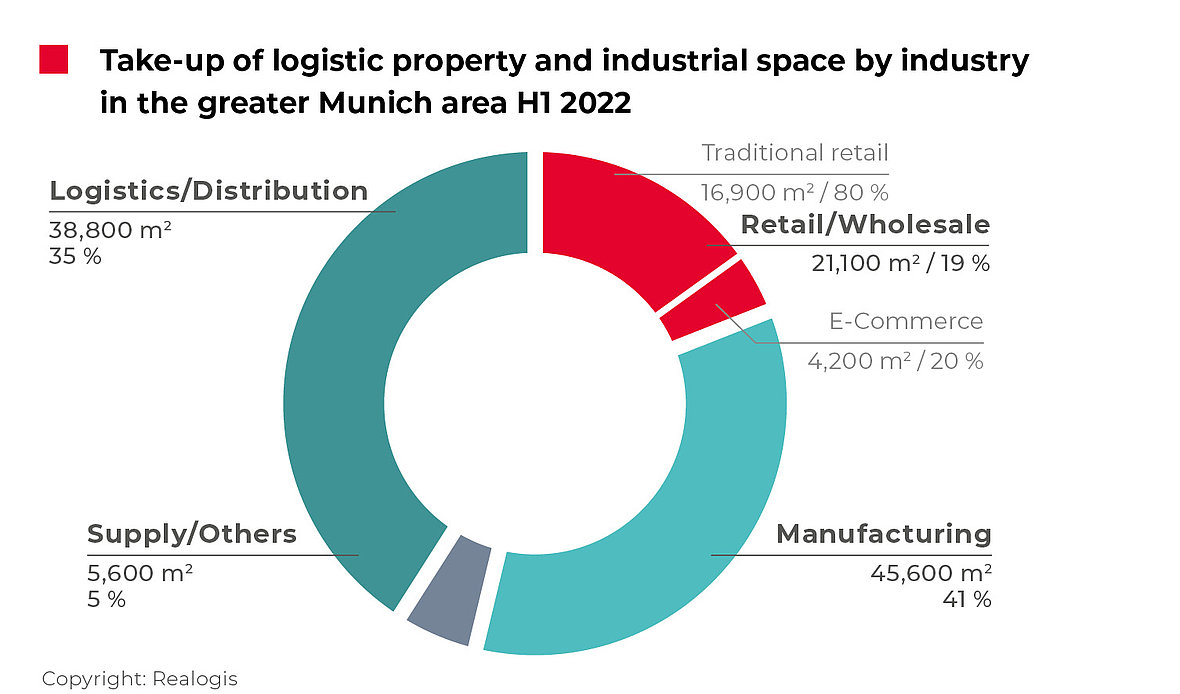

Manufacturing category tops the sector ranking

The sector with the highest take-up was manufacturing, which was responsible for 45,600 m² or a share of 41% in H1 2022. It posted the highest gain of all sectors in terms of relative importance (+14 percentage points), up from a share of 27% or 40,500 m² in H1 2021. In addition, it achieved the only absolute increase, at +12.6% (rising from 40,500 m² to 45,600 m²).

This might also be interesting for you:

To the market report Germany

Overall, the manufacturing sector accounted for 14 deals, almost one in three. These also include the second- and third-largest top deals: a company in the pharmaceutical sector with approx. 11,000 m² and TopTica Photonics AG with 5,800 m². Their combined share of the sector’s take-up in H1 2022 was around 37%.

The second-strongest sector was logistics/distribution at 38,800 m² or 34.9%. It came first last year with 49,900 m² or 33.3%. This category posted the highest number of deals in H1 2022 at 16, equating to around 36% of all deals in the first six months. The biggest of the top five deals, DHL with 14,000 m², contributed around 36%.

Decrease in take-up by e-commerce

Next came retail with 21,100 m², a share of 19%, down from 46,800 m² or 31.2% in the same period of the previous year. This was the sharpest decrease in relative importance of all sectors in H1 2022 (-12.2 percentage points). Retail accounted for a total of 10 deals (more than one in five at 22%), including just three deals in e-commerce totalling a mere 4,200 m². By way of comparison, e-commerce was responsible for two thirds of all retail space or 31,000 m² in the same period of the previous year. At present, e-commerce has a share of 19.9%, down 46.3 percentage points.

Traditional retail currently makes up 80.1% or 16,900 m², which is close to the previous year's figure (15,800 m²) in absolute terms. However, traditional retail saw its relative importance rise significantly by 46.3 percentage points to a share of 80.1% due to the poor performance of e-commerce.

With 7 deals, traditional retail accounted for the majority of transactions in the two sub-categories. Furthermore, two of the top deals were attributable to traditional retail: seHuber GmbH & Co KG for approx. 4,600 m², and Bravobike GmbH for approx. 3,520 m² (a combined contribution of 8,120 m² or 38.5%).

As in the same period of the previous year, the miscellaneous category “Others” ranked last with take-up of 5,600 m² or 5%, compared with 12,600 m² or 9% (4 deals).

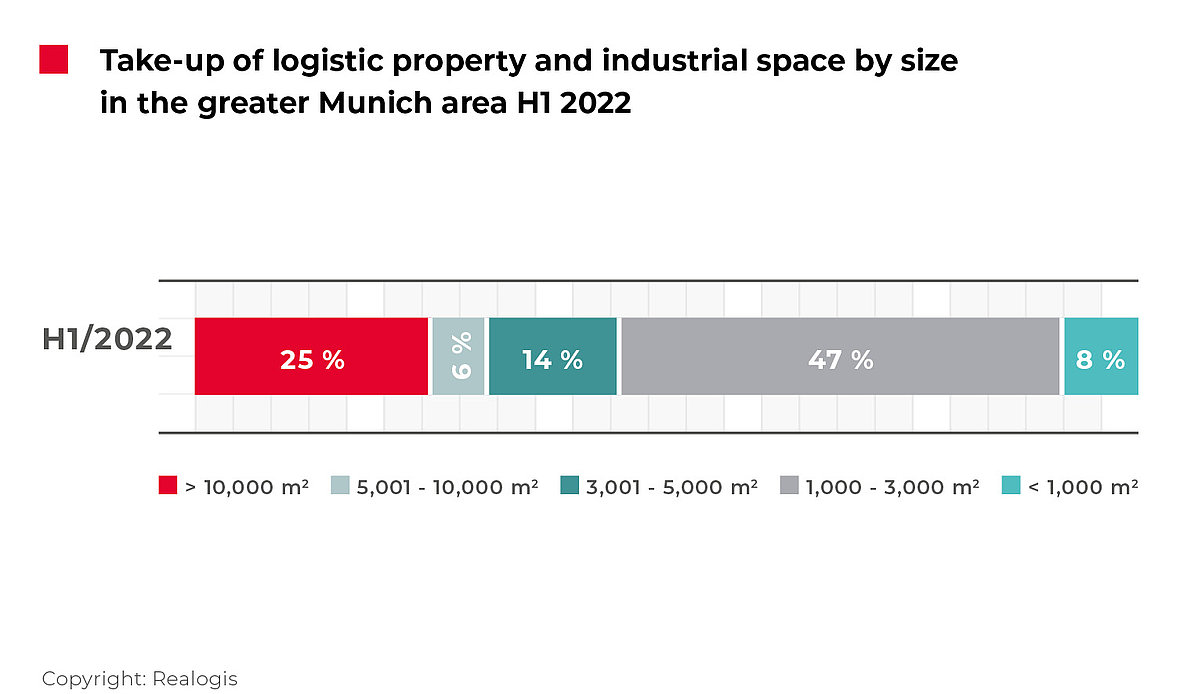

Small spaces account for almost half of take-up

Large spaces of 10,000 m² or more amounted to 27,500 m² or 24.7% of total take-up in the first half of the year, taking second place (H1 2021: 25,700 m² or 17.2%; +7.5 percentage points).

The size segment between 5,001 and 10,000 m² saw unusually little market activity, totalling just 6,400 m² or 5.8%, and consequently fell to the bottom of the size-category table in terms of take-up (H1 2021: 51,700 m² or 34%; -28.2 percentage points). Spaces between 3,001 and 5,000 m² came to 16,200 m² or 14.6% in the first half-year, taking third place (H1 2021: 29,400 m² or 19.6%).

Smaller spaces between 1,000 and 3,000 m² accounted for the lion’s share of the half-year result at 52,400 m² or 47.2%, claiming first place (H1 2021: 49,100 m² or 32.8%). The smallest spaces of less than 1,000 m² amounted to 8,600 m² or 7.7% (H1 2021: 19,600 m² or 13.1%).

82,000 m² of space under development

At present, just under 82,000 m² of new space is under development. Munich West is the region with the highest share, at more than 30,000 m². However, no properties will be completed this year. Approx. 50,000 m² will gradually enter the market in 2023.

Current project developments

Unternehmer Park by Aurelis, approx. 31,400 m² (Speculative), Around Q2 2024

Giesserei by Beos, approx. 22,000 m² (Speculative), Around Q2 2023

City Dock Kirchheim by Panattoni, approx. 14,800 m² (Speculative), Around Q4 2023

Am Lenzenfleck by Am Lenzenfleck GmbH, approx. 10,300 m² (Speculative), Around Q1 2023

multimini Kirchheimby MB Park Deutschland GmbH, approx. 3,500 m² (Speculative), Around Q4 2023

Highest level to date for prime rent at EUR 9.00/m² and average rent at EUR 6.95/m²

Businesses must now expect a prime rent of EUR 9.00/m² for industry and logistics properties in the Munich metropolitan region. This represents a 5.9% increase, taking it to its highest level to date. Moreover, the current prime rent exceeds the average prime rent of the last 5 half-years of EUR 8.24/m² by 9.2%.

Average rents have actually risen by 6.9% year-on-year from EUR 6.50/m² to the new record level of EUR 6.95/m². The current level is around 4% above the five-year average of EUR 6.69/m².

To the rent price maps:

Order the complete market report as PDF