HOCHWERTIG | 650 m² HALLE | 800 m² AUSSTELLUNG

ID: 998947DetailsGarching, repräsentatives Produktionsgebäude mit hochwertigen Büroflächen

ID: 93135Detailsca. 400 m² große, ebenerdige Lager-Produktionshalle mit Meisterbüro in Top Lage

ID: 1036679DetailsDirekt am Autobahnkreuz Ulm/Elchingen - Neubau multifunktionaler Logistik- und Produktionsflächen

ID: 994300DetailsLOGISTIK | RAMPEN | FREIFLÄCHE

ID: 1008605DetailsLager-/Logistik | Neubau | Rampen | teilbar | ebenerdig

ID: 1016255DetailsGEWERBEPARK | ERSTBEZUG | TOP-LAGE

ID: 996681DetailsBremen, ca. 1.300 m² Lager-/ Logistikfläche zu vermieten

ID: 1032273DetailsMünchen - Nord, Hallen- und Freiflächen in Bestlage zu vermieten

ID: 101077DetailsPROVISIONSFREI | GEWERBEPARK | FLEXIBEL

ID: 1000973DetailsArnsdorf | ca. 9.000 m² | Lager & Logistik | Betonrampe & ebenerdig | teilbar ab 2.000

ID: 1009874DetailsRepräsentativer Gewerbepark

ID: 1005086Detailsca. 1.350 m² große, ebenerdige Hallenfläche mit Büro

ID: 1035432DetailsPRODUKTION | LAGER | RAMPE

ID: 991522DetailsGarching, Neubau von ca. 8.000 m² Lager-,Forschungs- und Bürofläche

ID: 1030576DetailsMunich-North, warehouse and office spaces for rent

ID: 1033335DetailsMunich-North, warehouse and office spaces for rent

ID: 1024609DetailsMunich-North, warehouse and office spaces for rent

ID: 1034331DetailsMunich-North, warehouse and office spaces for rent

ID: 1002692DetailsMunich-North, warehouse and office spaces for rent

ID: 1034768DetailsMunich-North, warehouse and office spaces for rent

ID: 1034670DetailsMunich-North, warehouse and office spaces for rent

ID: 1034767DetailsMunich-North, warehouse and office spaces for rent

ID: 1025539DetailsMunich-North, warehouse and office spaces for rent

ID: 1010949DetailsMunich-North, warehouse and office spaces for rent

ID: 1032598DetailsAugsburg, site with about 2.500 sqm for rent

ID: 9040DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031912DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031769DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031836DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1028145DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030724DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030615DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1023871DetailsGladback, warehousing space for wholesale or retail for rent

ID: 95769DetailsGladback, warehousing space for wholesale or retail for rent

ID: 1013489DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1025426DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1026621DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1022435DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1023380DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1014315DetailsNeuss, approx. 1,295 sqm warehouse space in a business park for rent

ID: 997156DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1017665DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1019585Details

Do you have a question? Leave your contact details here and we will call you back!

Market report Frankfurt 1st half of year 2022

- About the logistics market in the economic region

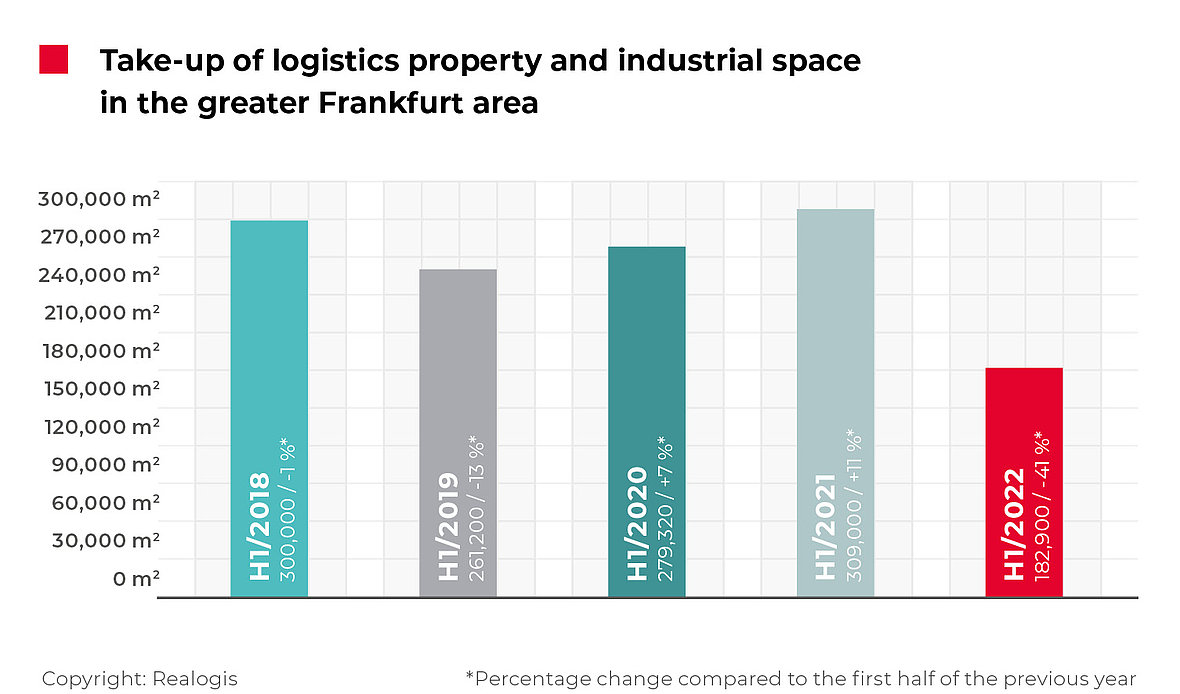

The letting market for industrial and logistics space in the Frankfurt metropolitan region has experienced a significant downturn. According to our analysis total take-up fell by a substantial 40.8% to 182,900 m² in the first six months. Compared to the 309,000 m² generated in the previous year, this represents the sharpest downturn compared to the first half of the year since our records began in 2015. In light of this, it is no surprise that take-up fell far short of the current five-year average for the first half of the year (266,484 m²), down 31.4%.

As well as the sharpest downturn, the market also recorded the lowest take-up for the first half of the year since 2014 and was 22.5% lower than the former weakest half year in H1 2014 at 236,000 m².

Facts

40.8% decrease in take-up compared to 182,900 m²

Hesse business moves to Rhineland-Palatinate and NRW

Letting dominated by big-box category and business parks

Rhine-Main South tops regional ranking

Sector ranking: Logistics/distribution again outperforms retail

Shortage of units upwards of 5,000 m² on Frankfurt market

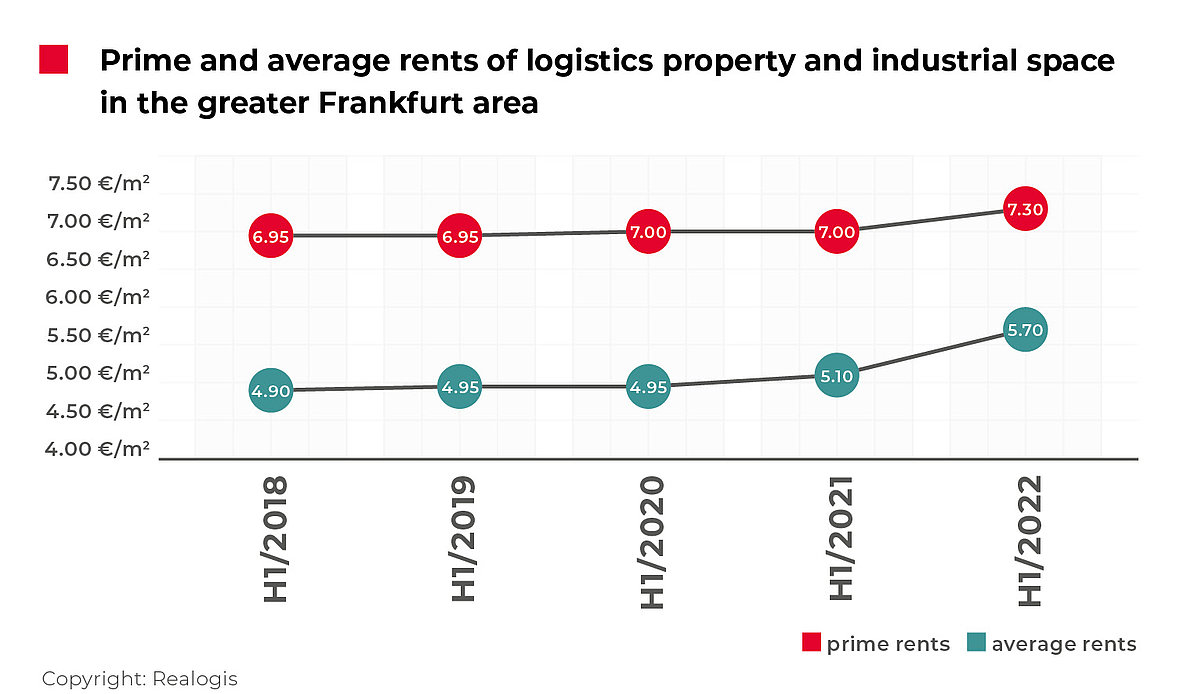

Prime and average rent reach highest levels to date

Current developments are also clearly reflected in the number of new leases signed: Between January and June 2022, all market participants combined signed a total of 50 leases for industrial and logistics space, compared to 62 in the first half of the previous year.

The main factor behind this weak result is the lack of new construction development: Just 43,900 m² of new-build properties was let in the last six months. By way of comparison, leases for new buildings accounted for more than two thirds of take-up in the first half of 2021 (65%) with take-up of 200,000 m². Now, they make up just 24% or one in every four-square metres let.

The development, which we had been warning about for years, is attributable to the fact that no new construction areas can be realized in the Frankfurt metropolitan region due to a lack of land designation. This trend is now taking full effect.

Demand in the retail and logistics sectors in the Rhine-Main region remains consistently high. The lack of new space is resulting in a run on existing properties among users and pushing up prices. These had been relatively stable for the last eight years but now they are rising noticeably. While rents for new big boxes, when they are available, are about EUR 7.30 per square metre, users of units in modern business parks can expect to pay as much as EUR 7.90 per square metre.

Considering the shortage of land, higher construction costs, the shortage of raw materials and increased financing costs, as things stand at present, we expect rents for users to continue rising in the future.

Looking to the future and in view of limited availability, especially in new construction, we expect total take-up by all market participants to come close to the 400,000 mark.

Lessors with highest take-up

B+S, Rhine-Main East, approx. 39,500 m² (Existing property), Logistics

Rexel, Rhine-Main South, approx. 26,000 m² (New build), Retail

Atrikom, Mainz/Wiesbaden, approx. 12,532 m² (New build), Logistics

P&A Managment GmbH, Frankfurt, approx. 5,600 m² (Existing property), Logistics

LSC Logistic Service Centre GmbH, Rhine-Main South, approx. 4,240 m² (Existing property), Logistics

Hesse business moves to Rhineland-Palatinate and NRW

Due to the shortage of development sites for industry and logistics in the Frankfurt metropolitan region, locations are being moved further and further out. This is clearly shown by current developments in Wiesloch, Philippsburg and Bad Hersfeld, as well as locations along the A3 motorway in the direction of Cologne. We also think there is still large potential for project developments, for example in the well-connected Koblenz region, which has seen some major deals signed in the last year.

The phenomenon of having to move out to the periphery or even to neighbouring states because of the lack of space has now clearly reached the Rhine-Main region too. Although users are looking for locations in the greater Frankfurt area, they have to compromise when choosing a location. In exchange, structurally weak regions are benefiting.

By contrast, the share and take-up of existing lets have increased. Compared to 109,000 m² and a share of 35% previously, they accounted for the majority in H1 2022 at about 135,500 m² or three quarters of space.

Brownfield letting accounted for take-up of 3,500 m² and a share of 1.9% in the first half of 2022. This was not represented in the previous year.

There were no contracts signed with owner-occupiers in the last half year, i.e., all new contracts were for properties that do not belong to the tenants.

Share of leases in big-box category and business parks almost on a par

The big-box category – i.e. large spaces of 10,000 m² or more, with logistics as the main type of use and an office share of no more than 20% – leads the pack at 85,800 m² and 46.9%, ahead of business parks at 79,700 m² and 43.6%. Space not covered by either of these two categories, such as individual properties, accounts for 9.5% at 17,400 m².

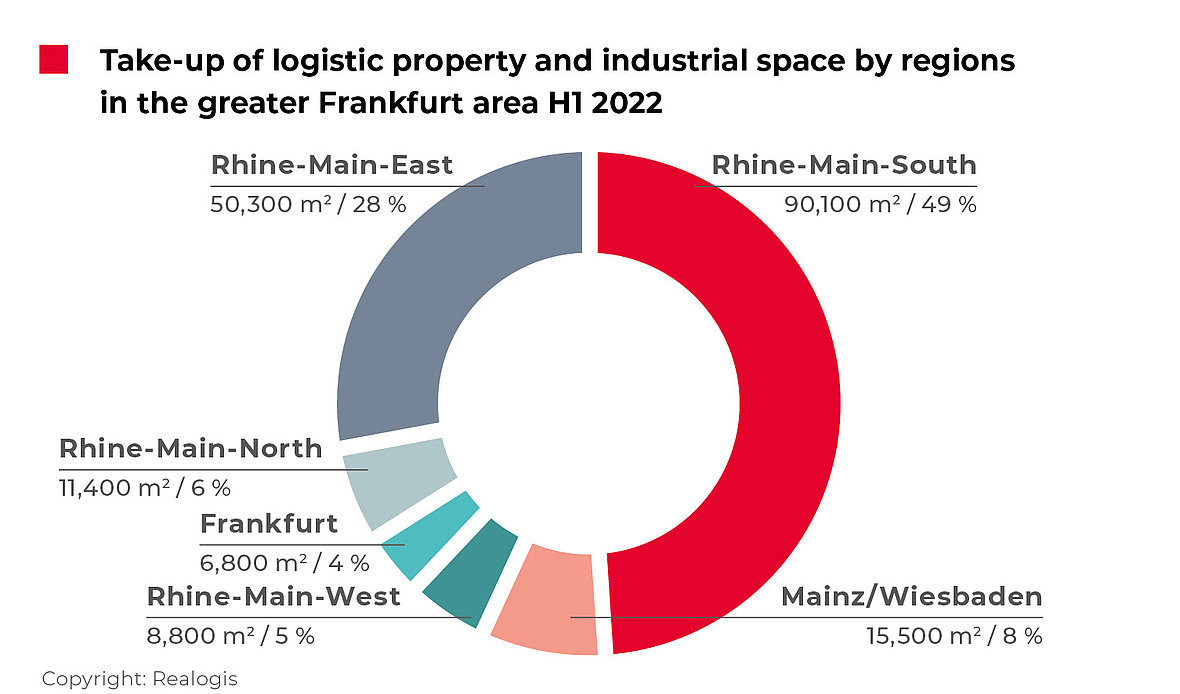

Rhine-Main South tops regional ranking

Rhine-Main South again came in first place with take-up of 90,100 m² or 49.3% (H1 2021: 153,300 m² or 49.6%). Two of the top five deals were again conducted in this region: Rexel (26,000 m²) and LSC Logistic Service Centre GmbH (4,240 m²). Overall, the region has over 60,000 m² less than in the previous year.

Rhein-Main East again comes in second with 50,300 m² or 27.5% (H1 2021: 105,600 m² or 34.2%), with take-up more than halving in absolute terms. The logistics service provider B+S was the greatest driver of take-up in this sub-market (79%) and also accounted for the largest deal (39,500 m²).

In third place comes the Mainz/Wiesbaden sub-market at 15,500 m² or 8.5% (H1 2021: 900 or 0.3% m²), the most significant relative increase of all regions compared with the previous year (up 8.2 percentage points). The Atrikom deal accounted for the majority of this at about 12,532 m².

These are followed by Rhein-Main North at 11,400 m² or 6.2% (H1 2021: 9,600 m² or 3.1%) and Rhein-Main West at 8,800 m² or 4.8% (H1 2021: 10,000 m² or 3.2%). The city of Frankfurt brings up the rear, sliding considerably to 6,800 m² or 3.7% (H1 2021: 29,600 m² or 9.6%), although a top deal was signed here with P&A Management GmbH for 5,600 m².

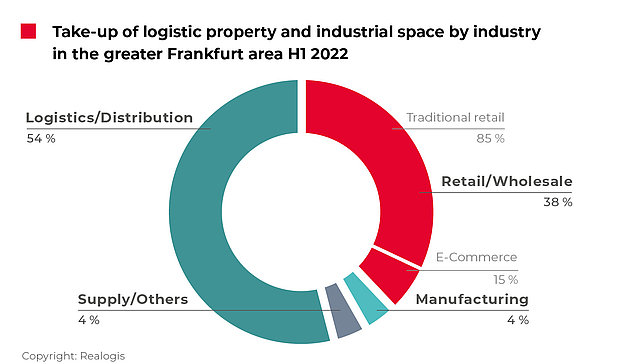

Sector ranking: Logistics/distribution again outperforms retail

Once again, the logistics/distribution had the highest take-up on the Frankfurt industry and logistics property market in the first half of 2022, accounting for more than half of all square metres at 98,700 m² or 54% (H1 2021: 136,800 m² or 44.3%).

Four of the top five deals were made in this sector, representing cumulative total take-up of about 61,872 m² or around 63% of the sector take-up:

B+S (39,500 m²)

Atrikom (12,532 m²)

P&A Management GmbH (5,600 m²)

LSC Logistic Service Centre GmbH (4,240 m²)

Retail again came in second place at 69,200 m² or 37.8% (H1 2021: 135,800 m² or 43.9%). Traditional retail currently accounts for more than four-fifths of the square metres taken up (H1 2022: 58,600 m² or 84.7%). The contract with Rexel, a company that specialises in the sale of electrical installation material and electrical components, made the greatest contribution to take-up (26,000 m²). Just 10,500 m² or 15.2% was rented by e-commerce companies.

The miscellaneous category “Other” came to 7,800 m² or 4.3% (H1 2021: 21,400 m² or 6.9%), and the manufacturing sector came to 7,200 m² or 3.9% (H1 2021: 15,000 m² or 4.9%).

This might also be interesting for you:

To the market report Germany

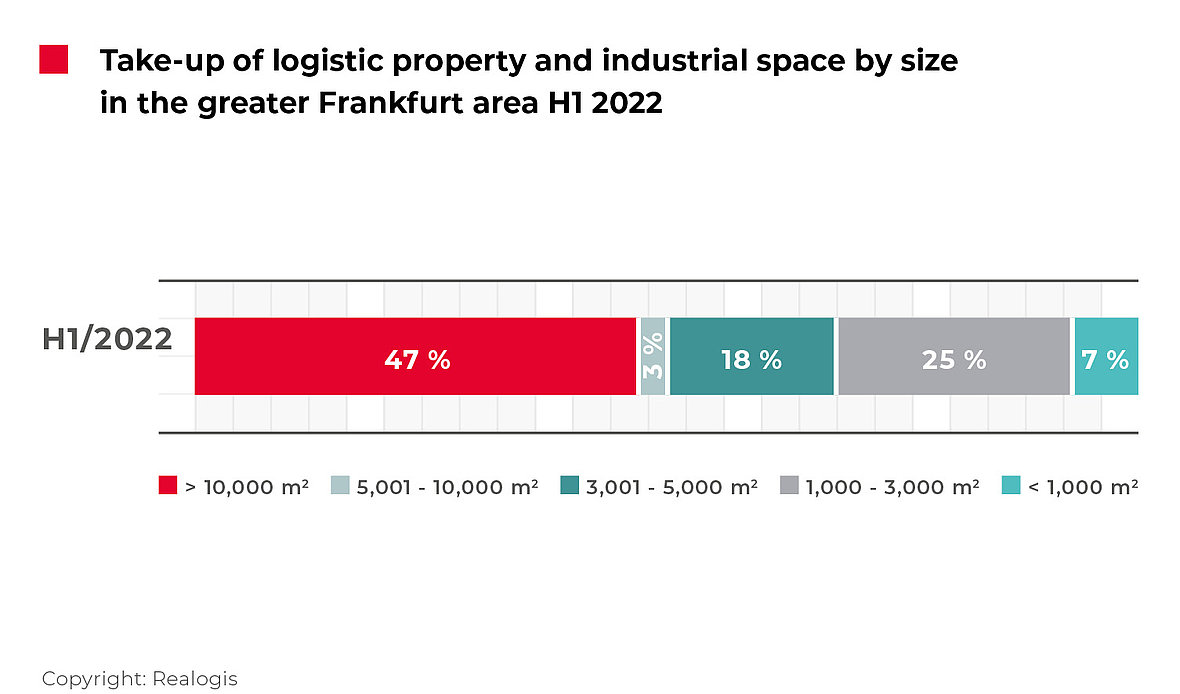

Shortage of units upwards of 5,000 m² on Frankfurt market

Almost half of all square metres in industrial and logistics space were in large-scale space between January and June 2022. The 10,001 m² and above size category claimed the most space at 85,800 m² or 46.9% (H1 2021: 125,900 m² or 40.7%).

Spaces between 5,001 and 10,000 m² lost out the most, falling by 94% in absolute terms and currently featuring total take-up of only 6,200 m² or 3.4% (H1 2021: 98,100 m² or 31.7%). Overall, 32,000 m² was newly let in the 3,001 to 5,000 m² segment (H1 2021: 20,800 m²), accounting for 17.5% of total take-up. Climbing by 8.2 percentage points, this size class saw the greatest upturn.

Smaller spaces of between 1,001 and 3,000 m² account for take-up of 45,400 m² or 24.8% (H1 2021: 51,300 m² or 16.6%), while the smallest spaces of less than 1,000 m² make up 13,500 m² or 7.4% (H1 2021: 12,900 m² or 4.2%).

Prime and average rent reach highest levels to date

Prime rent reached its highest level to date at EUR 7.30/m². Compared to EUR 7.00/m² in the previous year, this represents a 4.3% price increase, the biggest rise since the first half of 2018. This is 3.7% higher than the five-year average of EUR 7.04/m².

Average rent is also dynamic and is up by a substantial 11.8% on the previous year’s EUR 5.10/m² at EUR 5.70/m², marking the highest percentage increase since 2016. This is 11.3% above the five-year average of EUR 5.12/m².

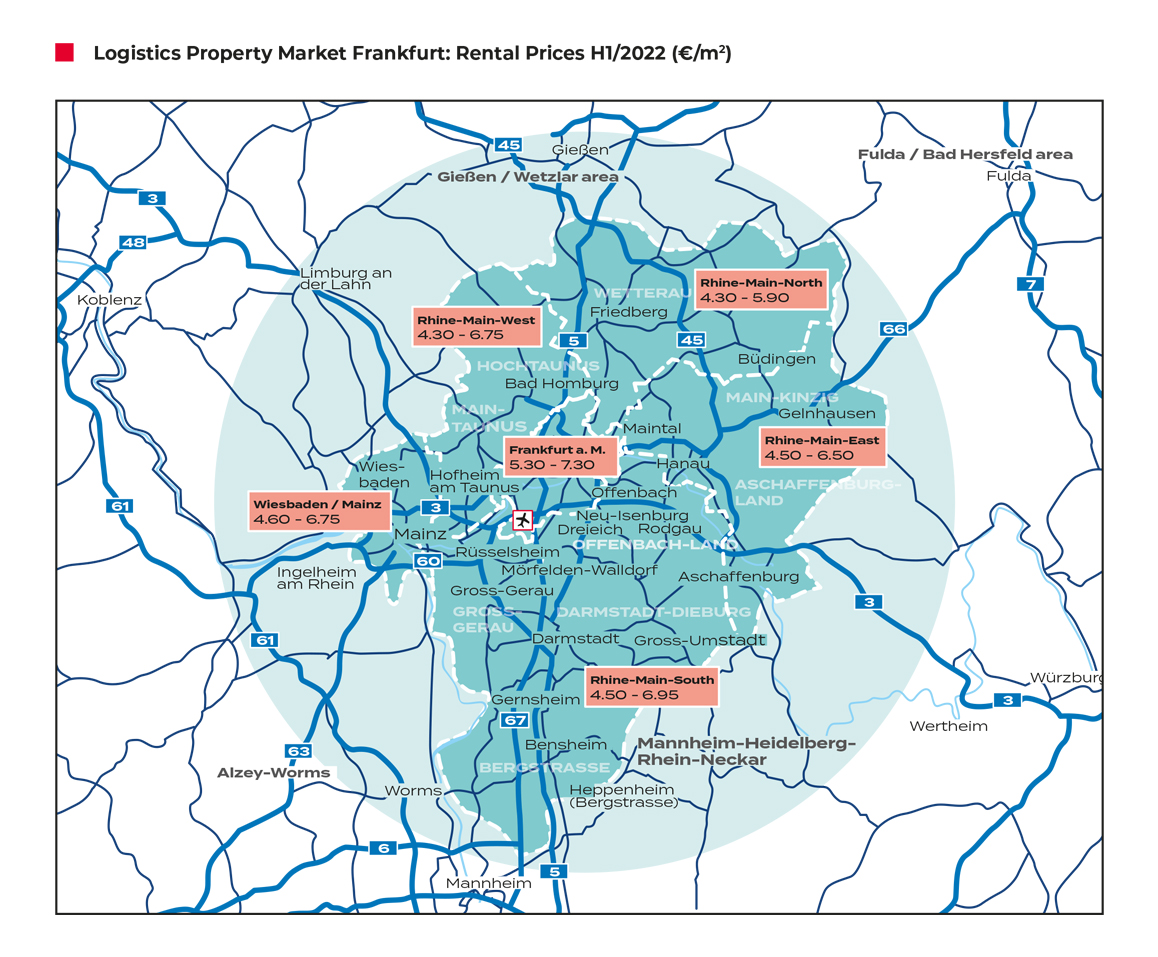

To the rent price maps:

Order the complete market report as PDF