HOCHWERTIG | 650 m² HALLE | 800 m² AUSSTELLUNG

ID: 998947DetailsGarching, repräsentatives Produktionsgebäude mit hochwertigen Büroflächen

ID: 93135Detailsca. 400 m² große, ebenerdige Lager-Produktionshalle mit Meisterbüro in Top Lage

ID: 1036679DetailsDirekt am Autobahnkreuz Ulm/Elchingen - Neubau multifunktionaler Logistik- und Produktionsflächen

ID: 994300DetailsLOGISTIK | RAMPEN | FREIFLÄCHE

ID: 1008605DetailsLager-/Logistik | Neubau | Rampen | teilbar | ebenerdig

ID: 1016255DetailsGEWERBEPARK | ERSTBEZUG | TOP-LAGE

ID: 996681DetailsBremen, ca. 1.300 m² Lager-/ Logistikfläche zu vermieten

ID: 1032273DetailsMünchen - Nord, Hallen- und Freiflächen in Bestlage zu vermieten

ID: 101077DetailsPROVISIONSFREI | GEWERBEPARK | FLEXIBEL

ID: 1000973DetailsArnsdorf | ca. 9.000 m² | Lager & Logistik | Betonrampe & ebenerdig | teilbar ab 2.000

ID: 1009874DetailsRepräsentativer Gewerbepark

ID: 1005086Detailsca. 1.350 m² große, ebenerdige Hallenfläche mit Büro

ID: 1035432DetailsPRODUKTION | LAGER | RAMPE

ID: 991522DetailsGarching, Neubau von ca. 8.000 m² Lager-,Forschungs- und Bürofläche

ID: 1030576DetailsMunich-North, warehouse and office spaces for rent

ID: 1033335DetailsMunich-North, warehouse and office spaces for rent

ID: 1024609DetailsMunich-North, warehouse and office spaces for rent

ID: 1034331DetailsMunich-North, warehouse and office spaces for rent

ID: 1002692DetailsMunich-North, warehouse and office spaces for rent

ID: 1034768DetailsMunich-North, warehouse and office spaces for rent

ID: 1034670DetailsMunich-North, warehouse and office spaces for rent

ID: 1034767DetailsMunich-North, warehouse and office spaces for rent

ID: 1025539DetailsMunich-North, warehouse and office spaces for rent

ID: 1010949DetailsMunich-North, warehouse and office spaces for rent

ID: 1032598DetailsAugsburg, site with about 2.500 sqm for rent

ID: 9040DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031912DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031769DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031836DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1028145DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030724DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030615DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1023871DetailsGladback, warehousing space for wholesale or retail for rent

ID: 95769DetailsGladback, warehousing space for wholesale or retail for rent

ID: 1013489DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1025426DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1026621DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1022435DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1023380DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1014315DetailsNeuss, approx. 1,295 sqm warehouse space in a business park for rent

ID: 997156DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1017665DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1019585Details

Do you have a question? Leave your contact details here and we will call you back!

Market report Hamburg half year 2023

- About the logistics market in the economic region

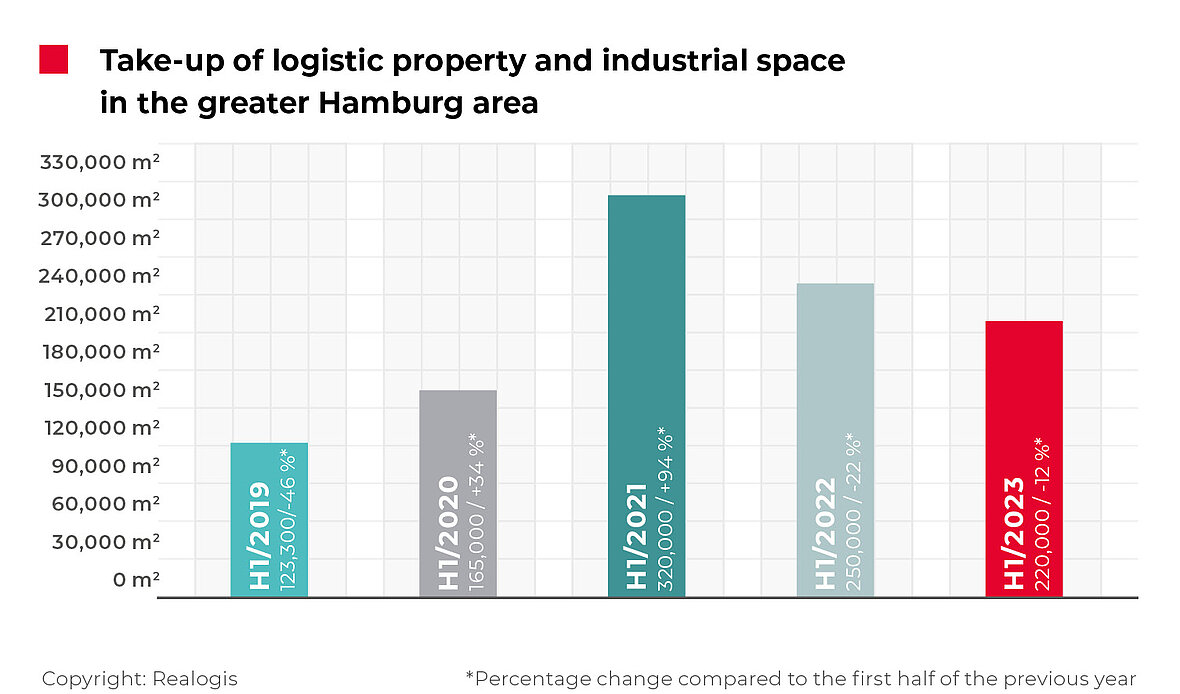

Hamburg industrial and logistics property market stands its ground despite second successive contraction

The Hamburg market for rental and owner-occupied logistics and industrial properties has contracted for the second year in succession. Take-up in the Hamburg metropolitan region declined by 12% to 220,000 m² in the first half of 2023 after 250,000 m² in the same period of the previous year. The figure for H1 2022 already represented a downturn of 21.9% compared with the record level of 320,000 m² recorded in H1 2021.

However, the negative trend has slowed, and the current take-up still exceeds the two weakest half-years recorded by us in the last five years by 55,000 m² and 126,700 m² respectively. It is also 2% higher than the five-year average for the first half of the year, which is 215,660 m². In other words, the result for the last six months is slightly above average. Looking back over the past decade, the Hamburg logistics and industrial property market came in above the 200,000 mark every year with the exception of the first half of 2019 and 2020.

Facts

- Take-up exceeds five-year average at 220,000 m²

- Rental market dominates

- Business parks account for two-thirds of take-up

- Hardly any big-box logistics properties available

- Outlook for the rest of the year: No new builds ready to go

- Regional ranking: Hamburg South region only narrowly ahead

- Sector ranking: Strong growth in manufacturing

- Size classes: Units between 5,000 and 10,000 m² up 15 percentage points

- Prime rents reach new peak

In the same way as for most of the other top markets for logistics and industrial properties, existing properties were the dominant category in Hamburg in the first six months of the year, accounting for 69.1% or 150,200 m² of total take-up. Lettings of new builds amounted to 68,000 m² or 30.9%. No brownfield developments were taken up in the period under review.

Biggest deals

TST GmbH, HH South, approx. 21,300 m² (New build), Logistics

Pandora Group, HH East, approx. 15,000 m² (New build), Manufacturing

Media-Saturn, HH South, approx. 14,600 m² (Existing property), Retail

IGEPA Group, HH East, approx. 13.500 m² (Existing property), Logistics

H-TEC SYSTEMS, HH East, approx. 11,400 m² (New build), Manufacturing

Rentals account for the vast majority of take-up: Around 92% or 201,500 m² of take-up was attributable to properties that did not belong to the users, whereas owner-occupiers accounted for just 8% or 18,500 m². By comparison, owner-occupiers were responsible for around one-third of take-up in the same period of the previous year, with a figure of 80,000 m² or 32% in this category.

In terms of building type, business parks accounted for the majority of take-up in H1 2023 at 144,200 m² or 65.5%. This significant increase of 86,700 m² meant that take-up was 2.5 times higher than the figure of 57,500 m² recorded in H1 2022. The relative share of take-up attributable to business parks also rose dramatically by 42.5 percentage points.

Big-box properties accounted for take-up of 75,800 m² or 34.5%. As well as constituting a significant reduction of 106,700 m² in absolute terms after 182,500 m² in the same period of the previous year, this meant the relative share of the market attributable to big-box properties declined by 38.5 percentage points. This property type accounted for around three out of every four square meters taken up in the previous year, whereas the corresponding figure for this year is around one-third. In absolute terms, the downturn of 106,700 m² in this area is almost entirely responsible for the lower half-year result (91%; the remaining -9% or -10,000 m² is attributable to properties that were not previously allocable).

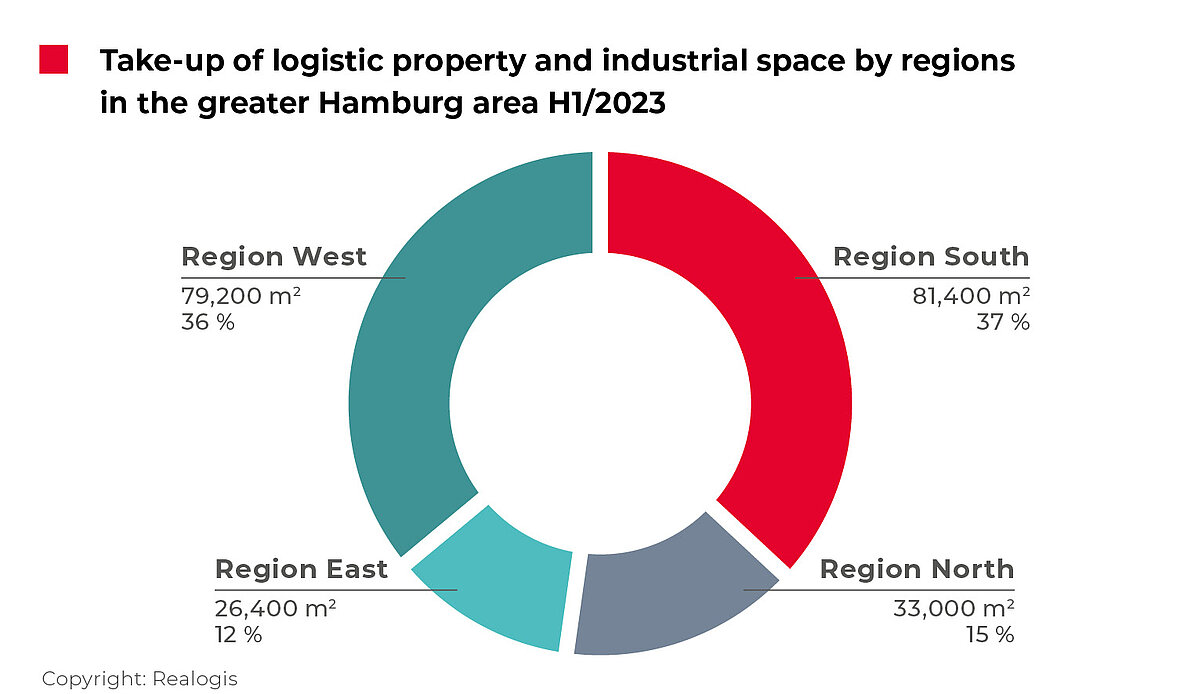

Regional ranking: Hamburg South region only narrowly ahead

Having been consistently ranked first since H1 2019, the Hamburg South region continued to head the regional ranking in the first half of the current year, accounting for 81,400 m² or 37% of total take-up. However, its lead narrowed considerably, with take-up declining significantly in absolute terms (36,100 m² or -30.7%) as well as in relative terms (-10 percentage points) compared with the figure of 117,500 m² or 47% in H1 2022.

At 36% or 79,200 m², the West region was only just behind the South region in second place, having been ranked fourth with take-up of 20,000 m² or 8% in H1 2022. It was the only region to record growth in absolute terms (a fourfold increase of 59,200 m²) and also saw the strongest increase in its relative share of the market (up 28 percentage points).

The North region remained in third place with take-up of 33,000 m² or 15%, compared with 37,500 m² or 15% in the same period of the previous year. Unlike all of the other regions, this meant take-up in the North region was largely stable (down 4,500 m² or 12% year-on-year).

Last year’s second-placed region East, brought up the rear after experiencing the biggest decline in take-up – from 75,000 m² to 26,400 m² (12 %), down 48,600 m² or -64.8% – and the most pronounced reduction in its relative share at -18 percentage points. This is unusual since the region had been consistently ranked second since H1 2019, averaging around 25% of total take-up during this time.

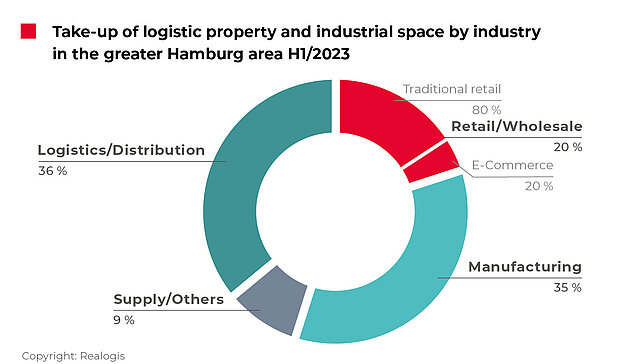

Sector ranking: Strong growth in manufacturing

Since H1 2016, logistics/ distribution has consistently been the biggest sector of the Hamburg market in terms of take-up. In the period from January to June 2023, it accounted for take-up of 79,600 m² or 36.2%, compared with 147,500 m² or 59% in H1 2022. This meant logistics/ distribution was the sector with the biggest downturn in absolute terms (67,900 m² or -46%), while its relative share of the market also declined by a substantial 22.8 percentage points. The two top deals by TST GmbH and IGEPA Group accounted for 34,800 m² or 44% of take-up.

Manufacturing saw the strongest sector growth, with take-up of 76,660 m² or 34.8% representing the highest figure since our records began. Compared with the prior-year figure of 10,000 m² or 4%, the second-placed sector in the current ranking recorded growth in terms of absolute take-up (a more than sevenfold increase of 66,600 m²) as well as its relative share of the market (up 30.8 percentage points).

The two top deals by the Pandora Group and H-Tec Systems collectively accounted for 26,400 m² or 34% of take-up in the sector.

At 44,000 m² or 20%, third place was taken by the retail sector, where take-up decreased by 38,500 m² (-47%) in absolute terms and by 13 percentage points in terms of relative share (H1 2022: 82,500 m² or 33%). Traditional retail was the main contributor, accounting for 35,200 m² or 80% of take-up in the sector. Of this figure, 14,600 m² or 41% was attributable to the major deal secured by Media-Saturn. E-commerce companies were responsible for the remaining 8,800 m² or 20%.

The miscellaneous category “Other” again ranked last with take-up of 19,800 m² and a market share of 9% (H1 2022: 10,000 m², 4%).

The reduction in total take-up in H1 2023 was due largely to the downturn in demand in the logistics/ distribution sector (-67,900 m² or 64% of the cumulative reduction in take-up), followed by the retail sector (-38,500 m² or 36%).

This might also be interesting for you:

To the market report Germany

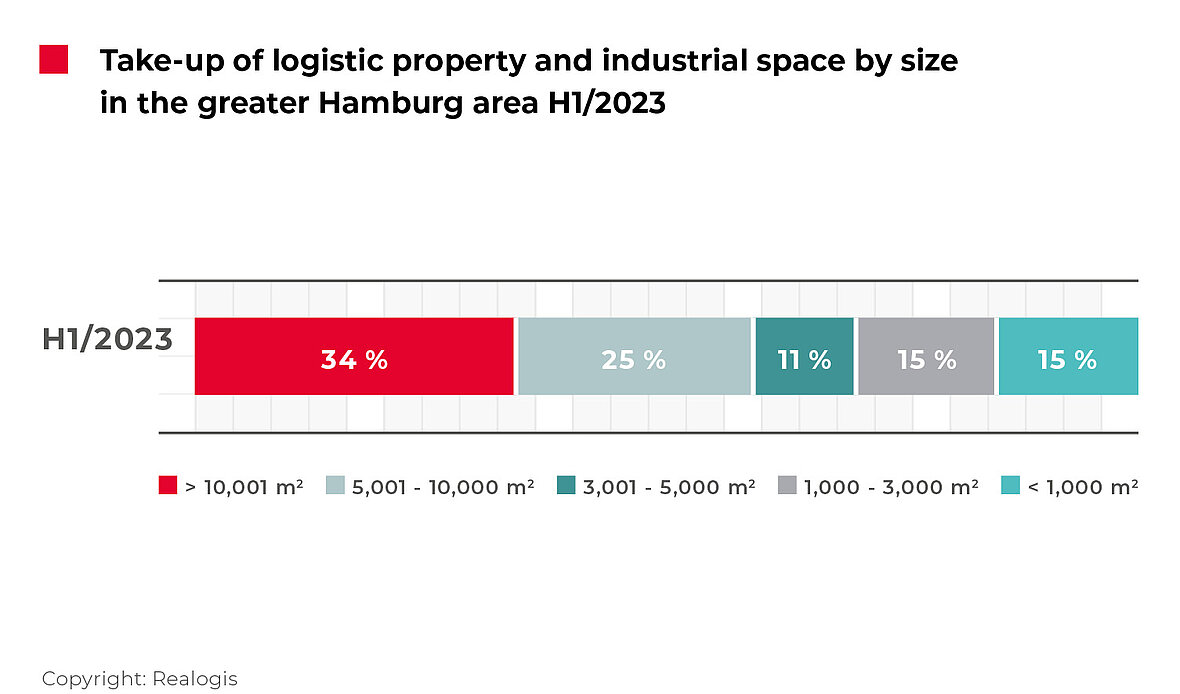

Size classes: Units between 5,001 and 10,000 m² up 15 percentage points

As in the previous year, large units of 10,001 m² or more were the biggest size class in the first half of 2023, accounting for take-up of 75,800 m² or 34%. While large spaces remain the most important size class on the Hamburg market, however, a comparison with the prior-year figure of 162,500 m² or 65% shows that this was the only size class to see a downturn in take-up in absolute terms (-86,700 m² or -53.4%) as well as a 31 percent reduction in its relative share.

Larger spaces between 5,001 and 10,000 m² accounted for 25% of take-up or 55,000 m² in the first six months of the current year, taking second place (H1 2022: 25,000 m² or 10%). This increase of 30,000 m² meant that take-up more than doubled compared with the same period of the previous year, while the size class also saw the biggest relative increase of +15 percentage points.

Medium-sized to larger spaces between 3,001 and 5,000 m² took last place at 24,200 m² or 11% (H1 2022: 20,000 m² or 8%).

Smaller spaces between 1,000 and 3,000 m² accounted for take-up of 33,000 m² or 15% (H1 2022: 17,500 m² or 7%, third place). The smallest spaces of less than 1,000 m² were ranked fourth with take-up of 32,000 m² or 15% (H1 2022: 25,000 m² or 10%).

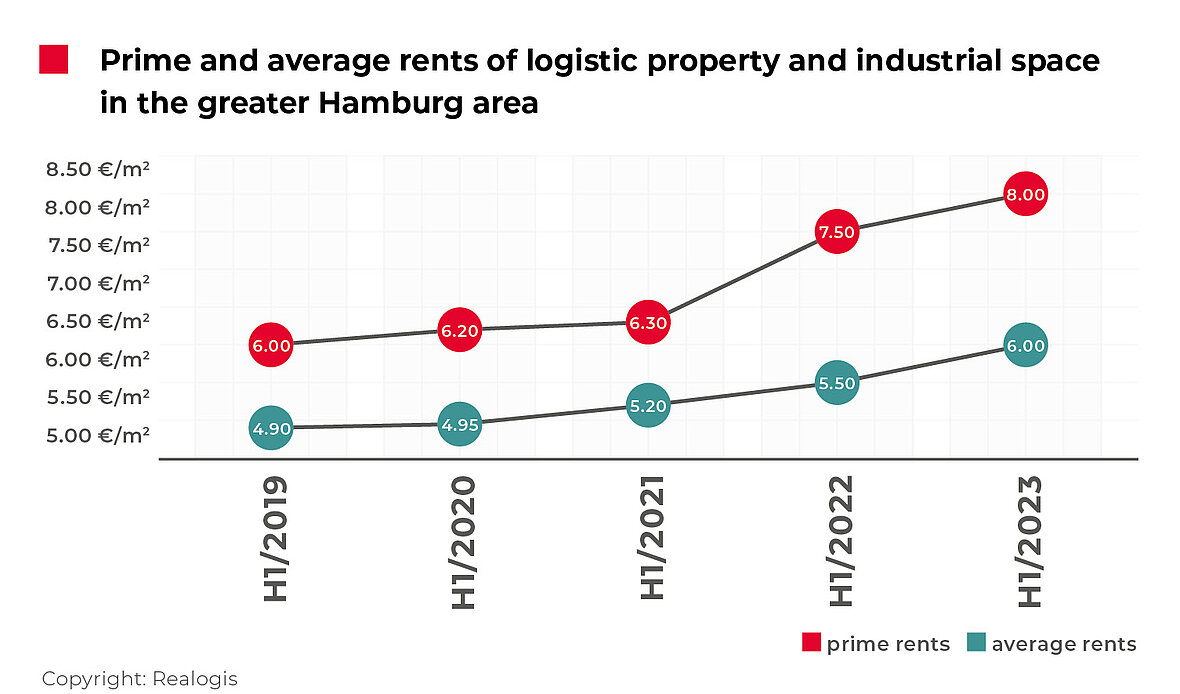

Prime rents reach new peak

Prime rents for industrial and logistics properties and units in business parks in the Hamburg metropolitan region reached their highest level to date, increasing by 6.7% to EUR 8.00/m² at the end of the first half of 2023 (H1 2022: EUR 7.50/m²). Prime rents have risen consistently since H1 2019, recording their highest growth rate of 19% in H1 2022 (from EUR 6.30/m²). The current figure is 17.6% higher than the five-year average of EUR 6.80/m².

Despite a severe shortage of available space and high construction costs, demand for high-quality logistics space remains dynamic. Properties need to be sustainable and satisfy ESG criteria as well as offering resource-saving concepts that help occupiers to lower their energy costs.

Meanwhile, average rents are outperforming prime rents in terms of growth, rising by 9.1% to a new high of EUR 6.00/m². This represents the biggest increase in the past five first half-years and means the current average rent is 13% higher than the five-year average of EUR 5.31/m².

Outlook

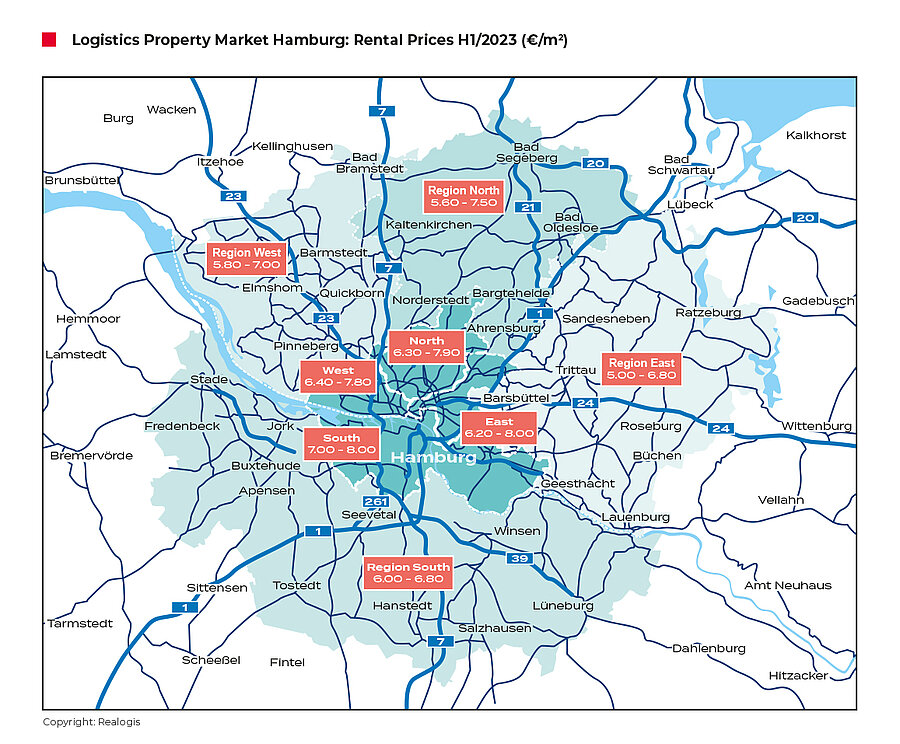

Currently there are almost no new spaces larger than 10,000 m² available. As a result, companies are having to look at sites in the wider Hamburg metropolitan region – along the A7 to Flensburg to the north, the A24 to Berlin to the east, and the A1 to Bremen to the south.

We expect full-year take-up on the Hamburg market for rental and owner-occupied logistics and industrial properties to amount to around 400,000 m² due to a shortage of high-volume space and the prevailing economic uncertainty.

To the rent price maps:

Request the complete market report as PDF