HOCHWERTIG | 650 m² HALLE | 800 m² AUSSTELLUNG

ID: 998947DetailsGarching, repräsentatives Produktionsgebäude mit hochwertigen Büroflächen

ID: 93135Detailsca. 400 m² große, ebenerdige Lager-Produktionshalle mit Meisterbüro in Top Lage

ID: 1036679DetailsDirekt am Autobahnkreuz Ulm/Elchingen - Neubau multifunktionaler Logistik- und Produktionsflächen

ID: 994300DetailsLOGISTIK | RAMPEN | FREIFLÄCHE

ID: 1008605DetailsLager-/Logistik | Neubau | Rampen | teilbar | ebenerdig

ID: 1016255DetailsGEWERBEPARK | ERSTBEZUG | TOP-LAGE

ID: 996681DetailsBremen, ca. 1.300 m² Lager-/ Logistikfläche zu vermieten

ID: 1032273DetailsMünchen - Nord, Hallen- und Freiflächen in Bestlage zu vermieten

ID: 101077DetailsPROVISIONSFREI | GEWERBEPARK | FLEXIBEL

ID: 1000973DetailsArnsdorf | ca. 9.000 m² | Lager & Logistik | Betonrampe & ebenerdig | teilbar ab 2.000

ID: 1009874DetailsRepräsentativer Gewerbepark

ID: 1005086Detailsca. 1.350 m² große, ebenerdige Hallenfläche mit Büro

ID: 1035432DetailsPRODUKTION | LAGER | RAMPE

ID: 991522DetailsGarching, Neubau von ca. 8.000 m² Lager-,Forschungs- und Bürofläche

ID: 1030576DetailsMunich-North, warehouse and office spaces for rent

ID: 1033335DetailsMunich-North, warehouse and office spaces for rent

ID: 1024609DetailsMunich-North, warehouse and office spaces for rent

ID: 1034331DetailsMunich-North, warehouse and office spaces for rent

ID: 1002692DetailsMunich-North, warehouse and office spaces for rent

ID: 1034768DetailsMunich-North, warehouse and office spaces for rent

ID: 1034670DetailsMunich-North, warehouse and office spaces for rent

ID: 1034767DetailsMunich-North, warehouse and office spaces for rent

ID: 1025539DetailsMunich-North, warehouse and office spaces for rent

ID: 1010949DetailsMunich-North, warehouse and office spaces for rent

ID: 1032598DetailsAugsburg, site with about 2.500 sqm for rent

ID: 9040DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031912DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031769DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031836DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1028145DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030724DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030615DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1023871DetailsGladback, warehousing space for wholesale or retail for rent

ID: 95769DetailsGladback, warehousing space for wholesale or retail for rent

ID: 1013489DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1025426DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1026621DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1022435DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1023380DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1014315DetailsNeuss, approx. 1,295 sqm warehouse space in a business park for rent

ID: 997156DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1017665DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1019585Details

Do you have a question? Leave your contact details here and we will call you back!

Market report Frankfurt half year 2023

- About the logistics market in the economic region

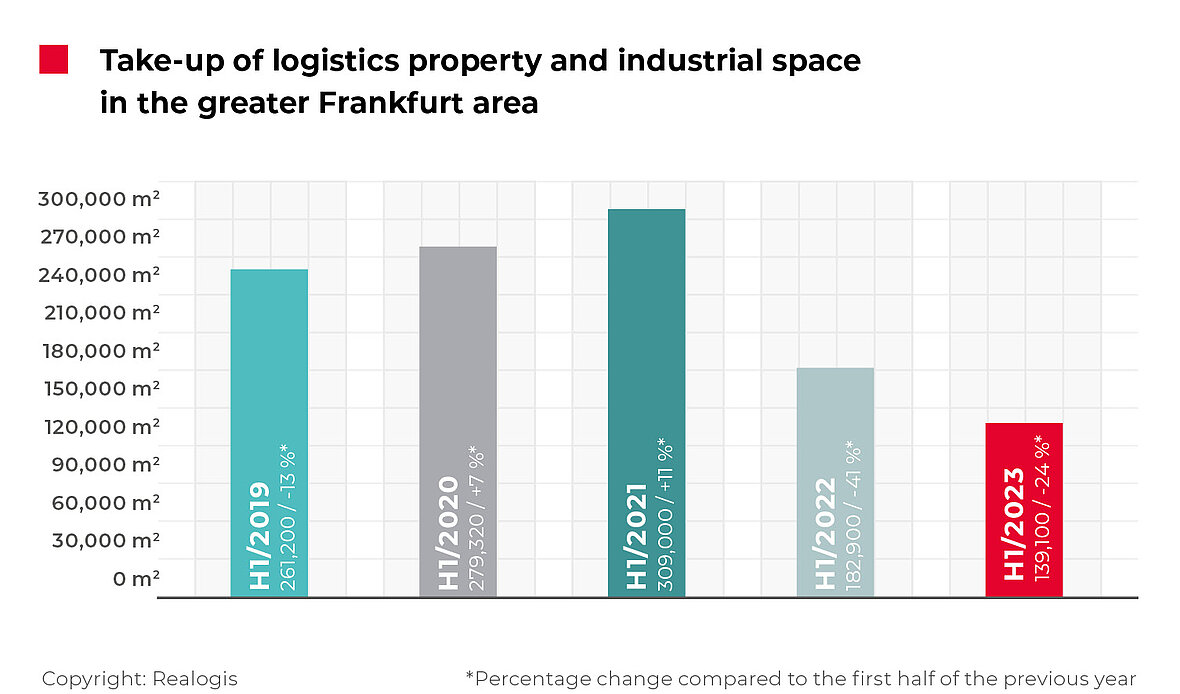

Frankfurt’s logistics and industrial property market significantly declines again

The Frankfurt rental and owner-occupied market for logistics and industrial properties continued the previous year’s negative trend in the first half of 2023. The take-up by all market participants declined by 23.9% compared with the first half of 2022 to 139,100 m².

Following the first half of 2021, which was the strongest first half of a year in the last ten years with 309,000 m², this is the second decline in a row. The trend has weakened slightly, but the current result is still below that of the same period of the previous year. The first half of 2023 therefore reached a new low. In terms of take-up, we have not seen a weaker first half of a year in ten years.

This is also shown by the average of the first halves of the last five years, which is currently 234,304 m². The figure for H1 2023 was 40.6% lower.

Facts

- New low: Take-up of just under 140,000 m²

- Rhine-Main South and Rhine-Main East markets dominate

- Sector ranking: Take-up by logistics/ distribution

- Take-up of large spaces declines by two-thirds compared with the first half of the previous year

- Moderate increase in prime rent to EUR 7.60/m²

Market activity was dominated by rental contracts in existing properties with 93,400 m² or a share of 67.1%. Like in the first halves of previous years (with the exception of H1 2022 with 135,500 m²), the result is therefore around the 100,000 mark.

In the first six months, lettings in new builds accounted for 34,700 m² or 24.9%. This is the crystallisation of a trend that began in the first half of last year. Compared with take-up of 200,000 m² in H1 2021, new build take-up collapsed by 78.1% to 43,900 m² in H1 2022 and has now dropped a further 21% to 34,700 m².

The reasons for this primarily lie in the heavily reduced availability of greenfield sites at the same time as high land prices and construction costs.

In H1 2023, brownfield developments contributed a total of 11,000 m² or 7.9%, including one of the top deals: Bringmeister GmbH signed a lease for 10,000 m² of space at the former Holzwerk Rütgers site in Hanau.

Biggest deals

Müller - Die lila Logistik SE, Rhine-Main-South, approx. 16,580 m² (Existing property), Logistics

DE NORA Deutschland GmbH, Rhine-Main-East, approx. 10,300 m² (New build), Manufacturing

Bringmeister GmbH, Rhine-Main-East, approx. 10,000 m² (Brownfield), E-commerce

Thermo Fisher Scientific Germany B.V. & Co. KG, Rhine-Main-East, approx. 8,000 m² (New build), Manufacturing

Aviapharm GmbH, Rhine-Main-South, approx. 6,700 m² (New build), Logistics

Barsan Global Logistik GmbH, Rhine-Main-South, approx. 6,000 m² (New build), Logistics

In the reporting period, we observed a total of 36 deals by all market participants in the reporting period, down by 14 or -28% on the first half of 2022. The average contract term of all registered leases is 6.5 years.

The logistics and industrial property market was overwhelmingly a rental market with 136,500 m² or a share of 98.1%. Owner-occupiers were responsible for only 2,600 m².

In terms of building type, lettings in business parks with 55,100 m² or 39.6% (H1 2022: 79,700 m² or 43.6%) were ahead of the ‘other properties’ category with 43,400 m² or 31.2% (H1 2022: 17,400 m² or 9.5%). Big box lettings amounted to 40,600 m² or 29.2% in the first six months (H1 2022: 85,500 m² or 46.9%).

In addition to new leases, we also included subleases in the calculation of take-up in the first half of the year for the first time. Subleases in industrial and logistics properties and business parks are playing an increasingly relevant role in the Frankfurt market. We currently expect further subleases to be signed in the coming months. This includes the deal for 16,580 m² by Müller - Die lila Logistik SE in Eppertshausen, which was the biggest in the first half of 2023 (11.9% of the total take-up in the first half of the year).

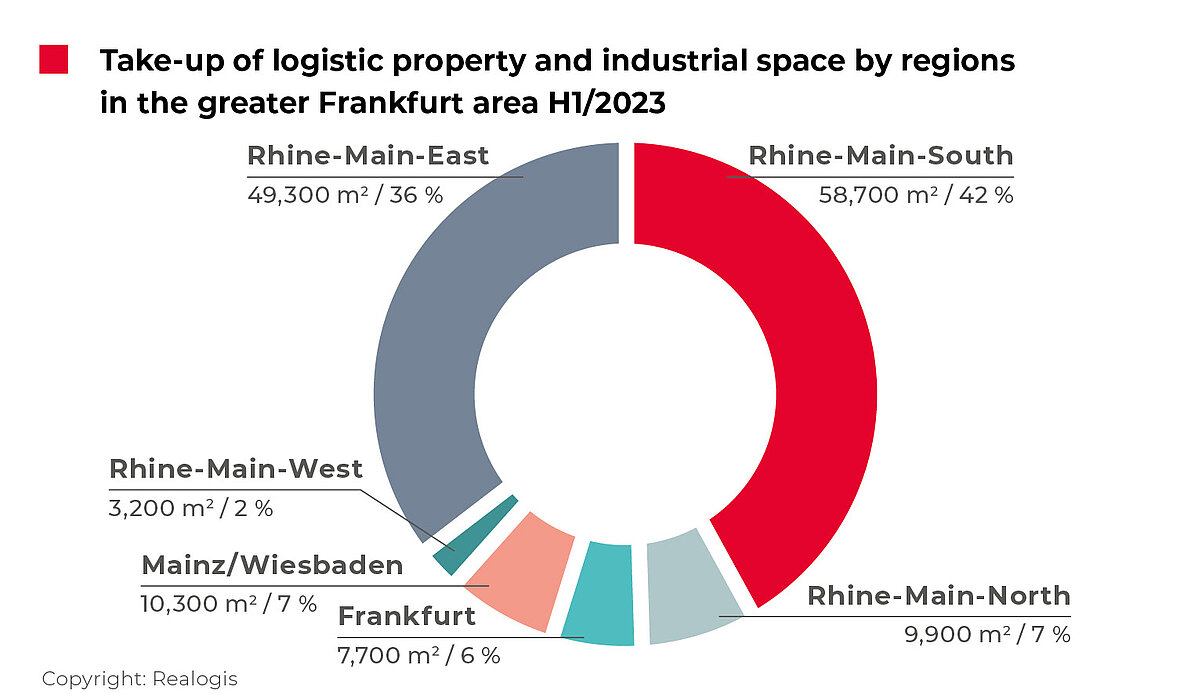

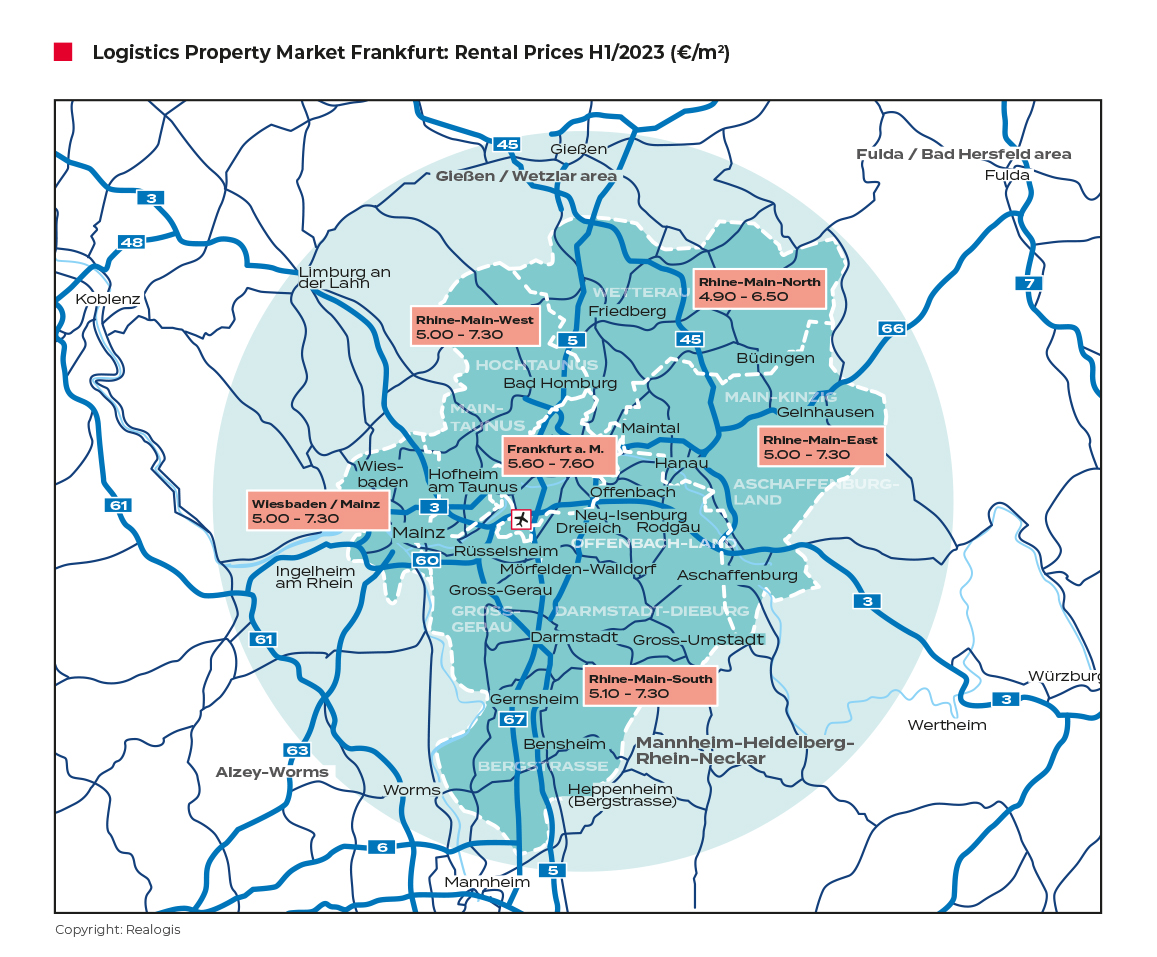

The Rhine-Main South and Rhine-Main East markets continue to dominate

Apart from the regions Rhine-Main West and Frankfurt (City), which swapped the last two places, the ranking did not change compared with the same period of the previous year. The regions were largely stable in terms of share of take-up. Consistently the most sought-after region since H1 2019, apart from in the first half of 2020, the Rhein-Main South submarket once again confirmed its leading role with 58,700 m² or 42.2% (H1 2022: 90,100 m² or 49.3%).

In contrast, take-up in the Rhein-Main South submarket dropped by more than a third (-34.9%) year on year, and the market also saw the biggest decline in share in take-up of 7.1 percentage points. Three of the six largest deals took place in the south, totalling 29,280 m² and thus accounting for half of this submarket.

The Rhein-Main East region, where the other three top deals took place (28,300 m² or around 57% of the region’s take up), remained in second place with 49,300 m² or 35.4% (H1 2022: 50,300 m² or 27.5%).

The Rhine-Main South and Rhine-Main East markets thus continue to dominate take-up. Combined, their take-up amounts to 108,000 m² or three-quarters of total take-up (77.6%).

The Mainz/ Wiesbaden region was again in third place with 10,300 m² or 7.4% (H1 2022: 15,500 m² or 8.5%) followed by Rhine-Main North with 9,900 m² or 7.1%. Last but one was Frankfurt City with 7,700 m² or 5.5%, ahead of Rhine-Main West with 3,200 m² or 2.3%.

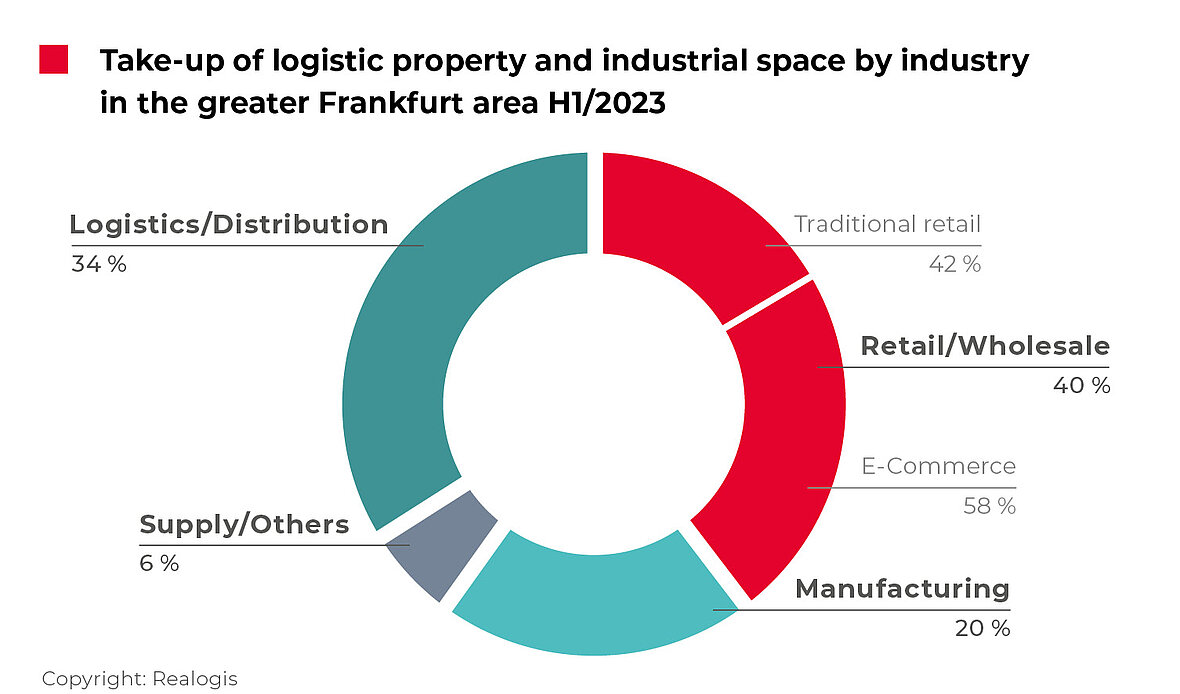

Sector ranking: Take-up by logistics/ distribution

The biggest sector in terms of take-up was retail with 55,300 m² or a share of 39.8% (H1 2022: 69,200 m² or 37.8%). More than half of retail’s take up – 57.9% – was attributable to the subcategory e-commerce with 32,000 m², to which Bringmeister GmbH contributed 10,000 m², or nearly a third (31%).

Year on year, e-commerce is currently beating conventional retail as a lessee in the Frankfurt metropolitan region – with a gain of 42.5 percentage points in the first half of the year. On the other hand, the total take-up by companies in the traditional retail sector amounted to 23,300 m² or 42.1%, coming from 58,600 m² or 84.7% (decrease of 35,300 m² or 60% in absolute term).

The logistics/ distribution sector took second place with 47,300 m² or 34% (H1 2022: 98,700 m² or 54%), whose absolute take-up more than halved (-52%) compared with the first half of the previous year and even dropped by nearly two-thirds (-65%) compared with H1 2021. The sector also lost the most ground in terms of its share, with a drop of 20 percentage points. Three of the six top deals are attributable to logistics/ distribution. With a total of 29,280 m², rental contracts contributed around 62% of the take-up.

Manufacturing ranked third with take-up of 27,300 m² or 19.6% (H1 2022: 7,200 m² or 3.9%), making it the industry with the biggest relative growth of +15.7 percentage points. The deals by DE NORA Deutschland GmbH and Thermo Fisher Scientific Germany B.V. & Co. KG contributed a total of 18,300 m² or 67% of the sector’s take-up.

Last place goes to the previously third-placed “Other” category with 9,200 m² or 6.6% (H1 2022: 7,800 m² or 4.3%).

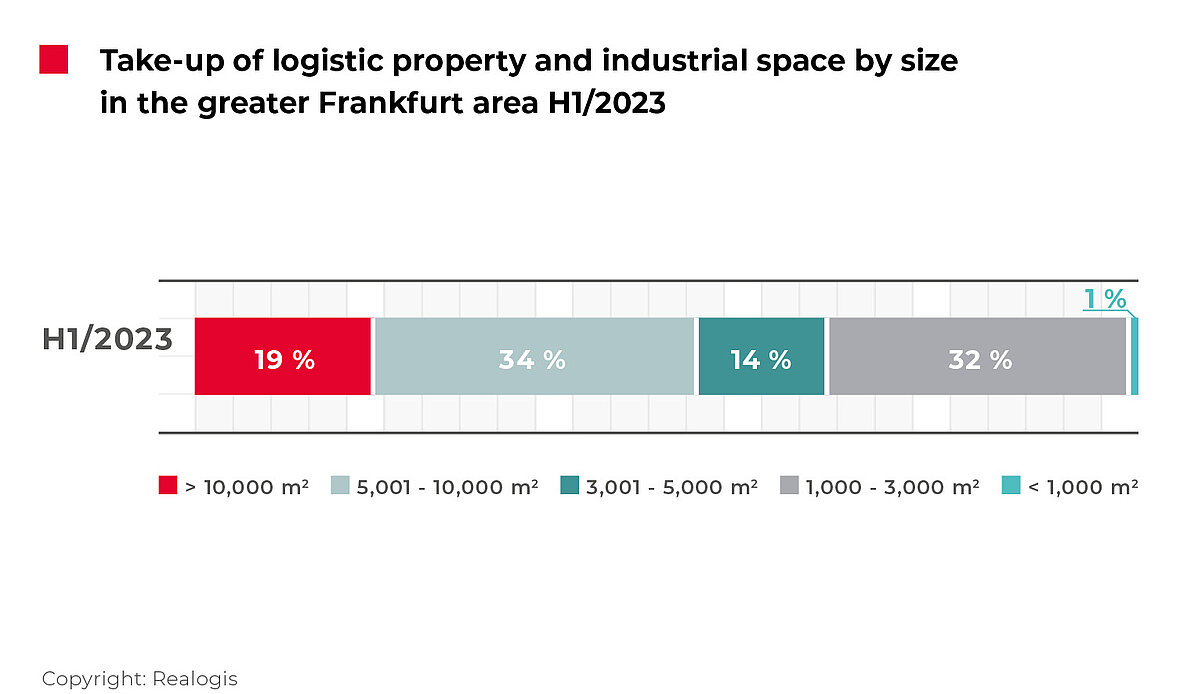

Take-up of large spaces declines by two-thirds compared with the first half of the previous year

In the first half of the year, large spaces of 10,001 m² and above accounted for only the third-most space at 26,880 m² or 19.3% (H1 2022: 85,800 m² or 46.9%). There were two deals – by Müller - Die lila Logistik SE and DE NORA Deutschland GmbH – neither of which came close to the 20,000 m² mark.

Spaces between 5,001 and 10,000 m² took first place in the first half of the year with 47,260 m² or 34% (H1 2022: 6,200 m² or 3.4%), which is partly attributable to four top deals.

Spaces between 3,001 and 5,000 m² ranked fourth with 18,800 m² or 13.6% (H1 2022: 32,000 m² or 17.5%). Smaller spaces between 1,000 and 3,000 m², with 44,180 m² or 31.8%, again proved highly significant for the Frankfurt market (second place) and were very stable compared with the other size categories (H1 2022: 45,400 m² or 24.8%). The smallest spaces of less than 1,000 m² contributed the least space at 1,900 m² or 1.4% (H1 2022: 13,500 m² or 7.4%).

This might also be interesting for you:

To the market report Germany

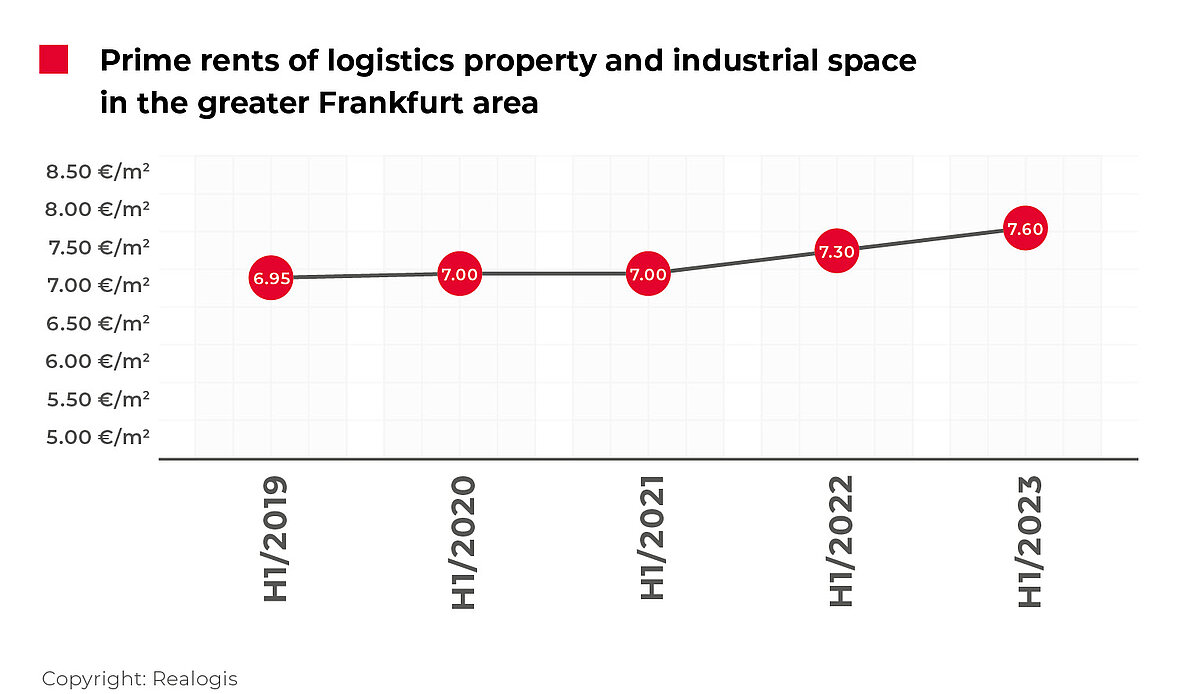

Moderate increase in prime rent to EUR 7.60/m²

The prime rent reached its highest level to date at EUR 7.60/m², compared with EUR 7.30/m² in the same period of the previous year, which equates to growth of 4.1% and continues the previous year’s trend of rising prices. The five-year average of EUR 7.17/m² was exceeded by 6%.

To the rent price maps:

Request the complete market report as PDF