HOCHWERTIG | 650 m² HALLE | 800 m² AUSSTELLUNG

ID: 998947DetailsGarching, repräsentatives Produktionsgebäude mit hochwertigen Büroflächen

ID: 93135Detailsca. 400 m² große, ebenerdige Lager-Produktionshalle mit Meisterbüro in Top Lage

ID: 1036679DetailsDirekt am Autobahnkreuz Ulm/Elchingen - Neubau multifunktionaler Logistik- und Produktionsflächen

ID: 994300DetailsLOGISTIK | RAMPEN | FREIFLÄCHE

ID: 1008605DetailsLager-/Logistik | Neubau | Rampen | teilbar | ebenerdig

ID: 1016255DetailsGEWERBEPARK | ERSTBEZUG | TOP-LAGE

ID: 996681DetailsBremen, ca. 1.300 m² Lager-/ Logistikfläche zu vermieten

ID: 1032273DetailsMünchen - Nord, Hallen- und Freiflächen in Bestlage zu vermieten

ID: 101077DetailsPROVISIONSFREI | GEWERBEPARK | FLEXIBEL

ID: 1000973DetailsArnsdorf | ca. 9.000 m² | Lager & Logistik | Betonrampe & ebenerdig | teilbar ab 2.000

ID: 1009874DetailsRepräsentativer Gewerbepark

ID: 1005086Detailsca. 1.350 m² große, ebenerdige Hallenfläche mit Büro

ID: 1035432DetailsPRODUKTION | LAGER | RAMPE

ID: 991522DetailsGarching, Neubau von ca. 8.000 m² Lager-,Forschungs- und Bürofläche

ID: 1030576DetailsMunich-North, warehouse and office spaces for rent

ID: 1033335DetailsMunich-North, warehouse and office spaces for rent

ID: 1024609DetailsMunich-North, warehouse and office spaces for rent

ID: 1034331DetailsMunich-North, warehouse and office spaces for rent

ID: 1002692DetailsMunich-North, warehouse and office spaces for rent

ID: 1034768DetailsMunich-North, warehouse and office spaces for rent

ID: 1034670DetailsMunich-North, warehouse and office spaces for rent

ID: 1034767DetailsMunich-North, warehouse and office spaces for rent

ID: 1025539DetailsMunich-North, warehouse and office spaces for rent

ID: 1010949DetailsMunich-North, warehouse and office spaces for rent

ID: 1032598DetailsAugsburg, site with about 2.500 sqm for rent

ID: 9040DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031912DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031769DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031836DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1028145DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030724DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030615DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1023871DetailsGladback, warehousing space for wholesale or retail for rent

ID: 95769DetailsGladback, warehousing space for wholesale or retail for rent

ID: 1013489DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1025426DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1026621DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1022435DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1023380DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1014315DetailsNeuss, approx. 1,295 sqm warehouse space in a business park for rent

ID: 997156DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1017665DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1019585Details

Do you have a question? Leave your contact details here and we will call you back!

Press Release

Top markets: REALOGIS market analysis for logistics and industrial property top 8 in 2023

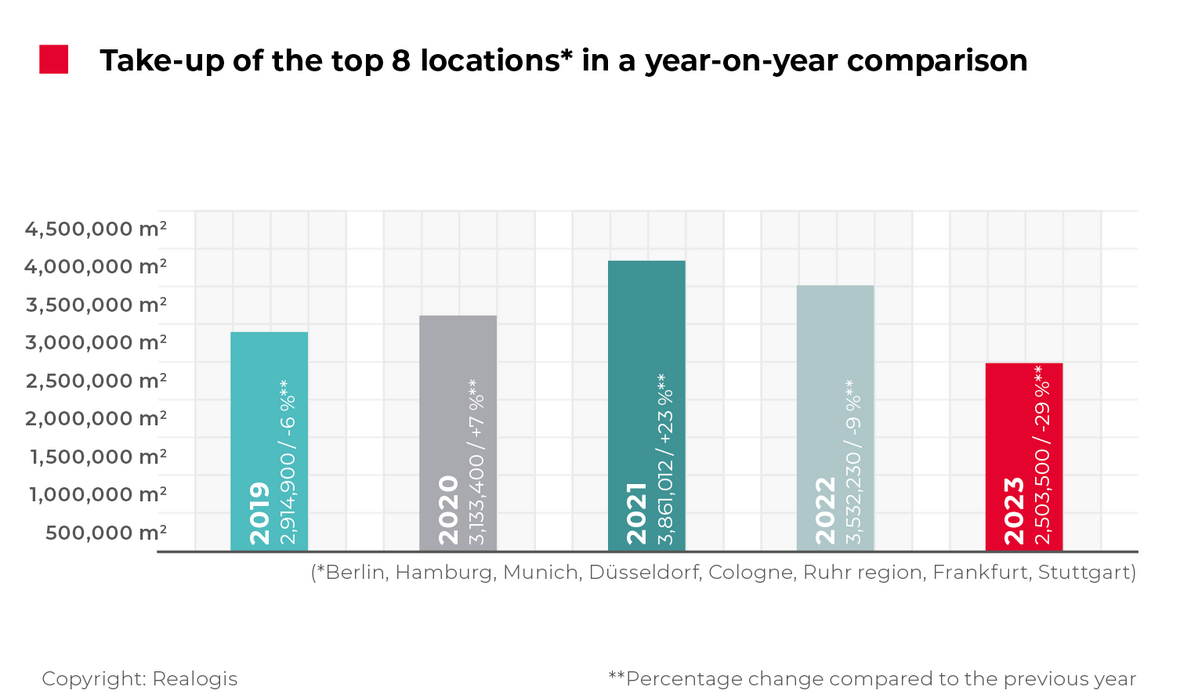

Slump on Germany’s top eight logistics locations– Drop of roughly 30% in new lettings and owner-occupancy

Munich, 16 February 2024 — Germany’s top eight locations for logistics and industry in Germany once again experienced a decline in lettings and owner-occupancy. According to Realogis — Germany’s leading consulting firm for industrial, logistics and commercial properties — new leases were signed for 2.5 million m² of space in total in the top eight by all market players in 2023. The eight leading German markets are the Ruhr area and the metropolitan regions of Hamburg, Frankfurt, Berlin, Munich, Cologne, Düsseldorf and Stuttgart.

“The trend that began in 2022 continued to gain traction. Take-up of logistics/industrial space and business parks slumped by a substantial 29.1% in 2023. Compared to a total letting volume of 3.5 million m² in 2022, this marks an absolute decline of around one million square metres. In other words, the nationwide drop-off is equivalent to the total take-up of all three top markets in NRW in good years,” explained Bülent Alemdag, Managing Director of Realogis Immobilien Düsseldorf GmbH.

“This development does not bode well for the German economy since losing its status as the world’s logistics champion,” Alemdag continued. “The population has grown to approximately 85 million in just a few years. But instead of providing more logistics space to supply the population and for retailers and manufacturers, the parameters for building new, modern and sustainable logistics and industrial space have simultaneously become much more difficult due to increased property prices and financing costs, for instance. The shortage of space and the increase in construction costs have caused rental prices to rise dramatically, and not every company can afford or wants to spend money on this.”

The decrease in 2022 was around 9% or 330,000 m² in absolute terms, while the change between 2023 and the record year of 2021, when the figure reached 3.86 million m², is 1.36 million m² in absolute terms, a decline of 35%. 2023 is now the weakest year as a whole in both the five-year and ten-year analysis. It is even lower than the previous record of 2.558 million m² in 2014.

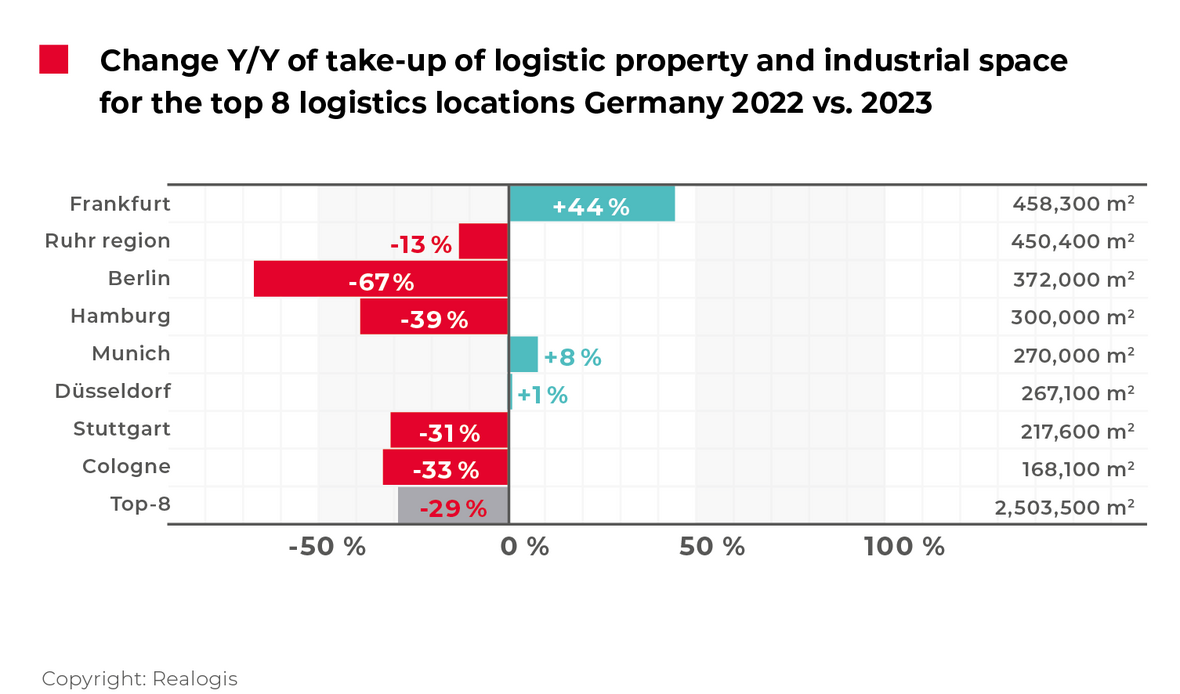

The past year as a whole brought double-digit declines in take-up for a majority of the top eight markets:

- The Ruhr region: down 13.3%

- Stuttgart: down 31.1%

- Cologne: down 32.6%

- Hamburg: down 38.8%

- Berlin: down 66.9%

Only two of the top eight markets reported growth, with Frankfurt at 44.3% and Munich at 8%. The top eight market of Düsseldorf was flat with a marginal increase of less than 1% (0.7%).

Ranking of top eight markets: Frankfurt takes lead in take-up

Frankfurt took the lead for the year as a whole, accounting for 18.3% of take-up in the top eight (458,300 m²). It has risen be three spots to fourth place, with growth of 44.3% from 317,700 m² or 9%. After 519,430 m² or 14.7% in the previous year, the Ruhr region is still in second place but now with 18.0% or 450,400 m² (down 13.3%). Berlin, last year’s number one, follows in third place with 372,000 m² or 14.9%, down from 1.12 million m² (a drop of 66.9%).

Hamburg takes fourth place in 2023 with 300,000 m² or 12%, dropping from third at 490,000 m² or 13.9% (a decline of 38.8%). Munich is ranked fifth with 270,000 m² or 10.8%, moving up from seventh and last but one place when it claimed 250,000 m² or 7.1% (increase of 8%). After 265,200 m² or 7.5% in the previous year, Düsseldorf is a non-mover in sixth place with 267,100 m² or 10.7% (growth of 0.7%).

Stuttgart drops to seventh with 217,600 m² or 8.7%, down from fifth place with 316,000 m² or 8.9% (a decline of 31.1%). Cologne again brought up the rear with 168,100 m² or 6.7%, down from 249,400 m² or 7.1% (a drop of 32.6%).

Five-year average missed by 21.5%

The figure for 2023 falls a hefty 21.5% short of the current five-year average of 3.189 million m². Looking at the averages of the individual markets, Düsseldorf alone matched the five-year average, or at least had the smallest shortfall of all markets, at 0.2%. Three markets missed their respective averages only moderately by less than 10%. These are Frankfurt (down 3.6%), Stuttgart (down 4.2%) and Munich (down 9.6%), which all came relatively close to the five-year average, though they were unable to reach it. The following four markets achieved less, in some cases far less, than 80% of their five-year average take-up: Cologne (down 25.3%), the Ruhr region (down 26.7%), Hamburg (down 34.8%) and Berlin (down 40.1%).

Berlin accounts for 63.2% of the deficit of 1.19 million m² in the past year (down 752,500 m² year-on-year), Hamburg for 15.9% (down 190,000 m²), Stuttgart for 8.3% (down 98,400 m²), Cologne for 6.8% (down 81,300 m²) and the Ruhr region for 5.8% (down 69,030 m²). The growth in Frankfurt (up 140,600 m²), Munich (up 20,000 m²) and Düsseldorf (up 1,900 m²) of 162,500 m² in total failed to make up for the deficit, resulting in a net difference of 1.028 million m² from 2022 to 2023.

Big boxes and business parks still the most sought-after building category with an accumulated share of 71%

Big-box properties set the pace for lettings in the top eight in 2023 with a share of 46% or around 1.15 million m². They are followed by properties that are neither big boxes nor business parks, at 29% or 727,100 m², and then by business parks, accounting for 25% or 628,600 m². “Business parks have become more important in terms of letting performance across all locations, which is also thanks to their appeal to local authorities as well as users,” explains Julian Petri, Managing Director of Realogis Immobilien Frankfurt GmbH. Big boxes fell by 31% or 516,300 m² and other properties by 41% or 510,500 m².

Top eight markets predominantly characterised by letting versus owner-occupancy

With a share of 91.2% or 2.28 million m², the overwhelming majority of deals were for properties that are not owned by the users. Owner-occupiers accounted for 8.5% or 211,900 m². Unknown ownership structures contributed the remainder of 8,000 m² or 0.3%. In the previous year, owner-occupiers accounted for 20.2% or 712,500 m² thanks to the major Tesla deal in the top eight market of Berlin, while lettings claimed 79.4% or 2.8 million m².

Owner-occupancy and lettings each accounted for almost half of the difference between 2023 and 2022. A drop of 49% or 500,600 m² can be attributed to owner-occupiers and around 51% or 521,430 m² to lettings.

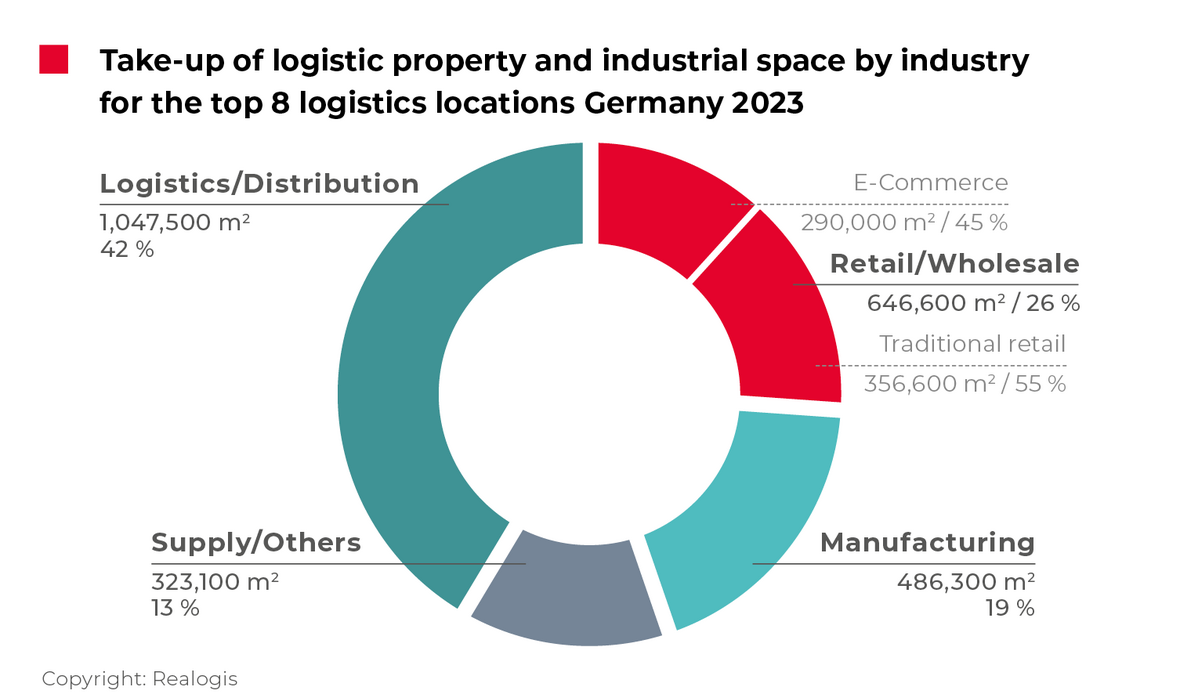

Logistics leads again – Retail cuts take-up by half – Manufacturing down by around 40%

Logistics/distribution ranks first in terms of take-up by sector, accounting for 1.05 million m² or 41.8% of take-up in the top eight (up from second place at 1.22 million m² or 34.5%). There was a decline of around 170,000 m² (down 14%) in absolute terms, though this was less severe than the drop experienced in the other sectors, in particular in retail, the previous leader. 14 of the 30 top deals accounted for 407,000 m² or 39% of take-up. The largest new leases can be credited to Group 7, which took 60,000 m² in Munich, and Yusen Logistics, which leased 50,000 m² in the Ruhr area.

Retail, the previous leader, dropped to second in 2023 with 646,600 m². Coming from 1.24 million m², take-up almost halved compared to the same period of the previous year (down by 48.1% or around 600,000 m²).

“Retail had the most significant slump of all sectors. One of the reasons for this can be traced back to the weak consumer sentiment in the face of the higher cost of living, which is also reflected in the double-digit decline in online retail sales in Germany compared to 2022,” explains Jörg Lojewski, Managing Director of Realogis Immobilien Hamburg GmbH.

The biggest Deals in the retail category include the lease for 56,000 m² of space signed by Thalia in the Ruhr region and the 40,000 m² leased by E. Breuninger GmbH und Co. KG in Stuttgart. The sub-category of traditional retail led the way within the retail sector with 356,600 m² or 55.2% of take-up (down by 383,000 m² or 51.8% from the previous 740,000 m² or 59.4%). E-commerce accounted for 290,000 m² or 44.8%, a drop of 215,000 m² or 42.6% (from 505,300 m² or 40.6%).

Manufacturing remains in third place with 486,300 m² or 19.4%, down from 814,400 m² or 23.1%. Falling 328,100 m² or 40.3%, this sector was second only to retail in terms of the absolute decline in take-up. The biggest Deals in the manufacturing category include the leases with Vorwerk for 45,600 m² in Düsseldorf and Siemens Mobility for 30,000 m² in Munich.

In last place is the miscellaneous category “Other” with 323,100 m² or 12.9%, rising from 255,500 m² or 7.2% and thus the only sector to increase its take-up with a gain of 67,584 m² or 26.5%. The deal signed by Computacenter in Cologne contributed 26,500 m² to this (8% of take-up in the miscellaneous category).

The majority of the take-up deficit for the year as a whole can be attributed to retail, which accounts for 54.6% (down 598,374 m²), followed by manufacturing with 29.9% (down 328,117 m²) and logistics/distribution with 15.5% (down 169,823 m²).

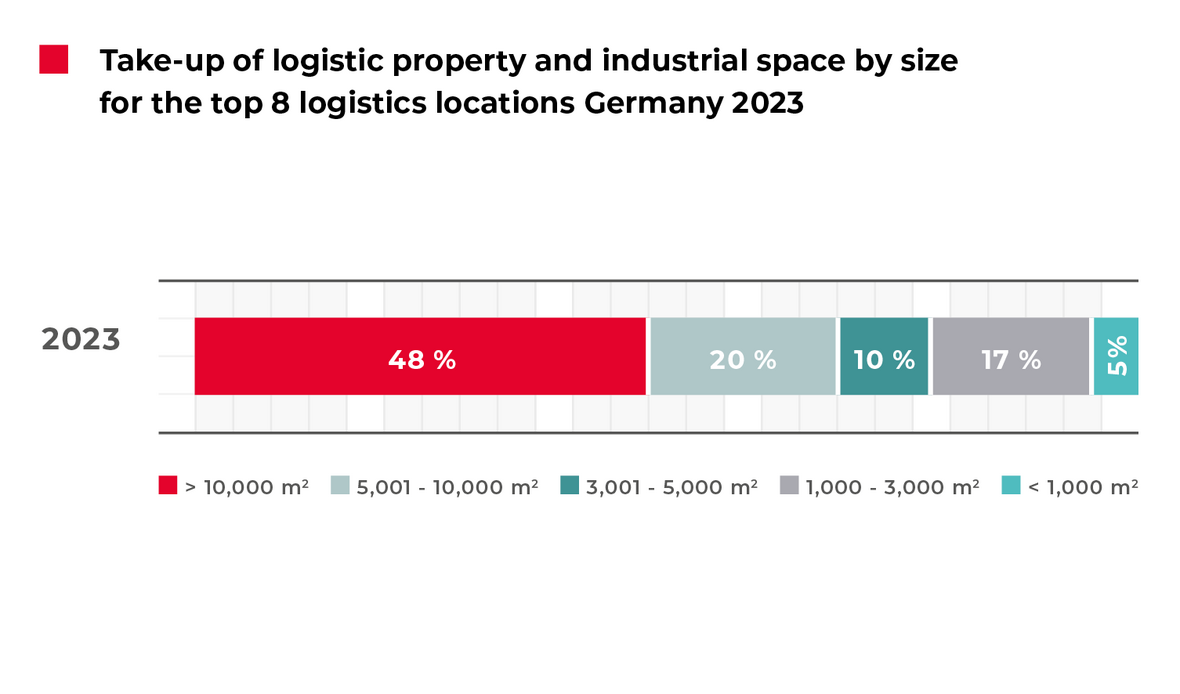

Big boxes suffer drop of 45.6% in take-up

“Large spaces of 10,001 m² or more are still the most sought-after in the top eight locations,” says Joel Adam, Managing Director of Realogis Immobilien Stuttgart GmbH. “This segment is so attractive for a large number of companies because the properties usually have a variety of multifunctional doors, rolling shutter gates and grilles, plus loading ramp solutions. So they support the efficient flow of production and goods for users.”

Large spaces accounted for 1.2 million m² or 48.6% of take-up in total in 2023 (2022: 63.4% or 2.24 million m²). The deficit of 1.02 million m² or 45.6% marks the most significant decline across all size categories.

Larger spaces between 5,001 and 10,000 m² take second place, accounting for 503,700 m² or 20.1% (2022: 424,078 m² or 12%) and are thus the only size category to achieve year-on-year growth in take-up, with 79,622 m² or 18.8%.

Medium to large spaces between 3,001 and 5,000 m² are still in second to last place, accounting for 245,250 m² or 9.8%. A year-on-year comparison shows a reduction of 45,776 m² or 15.7% (the second-largest decline in all size categories). Small to medium-sized spaces were the third most sought-after size category at 417,800 m² or 16.7% (a slight decrease of 14,260 m² or 3.3%).

At 119,400 m², micro spaces accounted for 4.8% of take-up and are therefore in last place (2022: 146,530 m² or 4.1%, a decrease of 27,130 m² or 18.5%). The weak result for the year as a whole can clearly be attributed to the lack of deals for large spaces. With a drop of around 1 million m², the size category of 10,001 m² and up is responsible for 92% of the change compared to the previous year. The declines in the other size categories totalled 87,166 m² or 8% of the difference. The increase of 79,622 m² in the category of spaces between 5,001 and 10,000 m² failed to offset this.

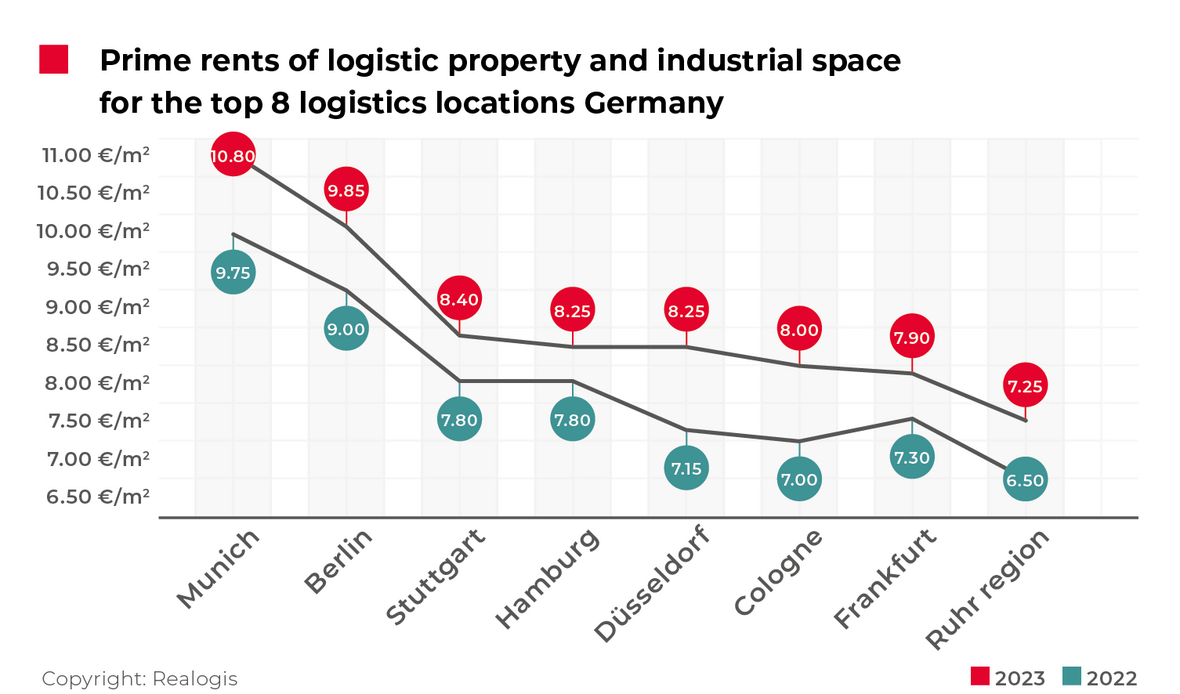

Prime rents rising on three of top eight markets

“Prices for both prime and average rents are continuing to rise on the top eight markets for logistics and industrial property. Not one market has remained flat or seen a drop in prices,” explains Nicolas Werner, Managing Director of Realogis Immobilien München GmbH

Prime rent

- Munich is still the most expensive location for prime rents at EUR 10.80/m² (up 10.8% from EUR 9.75/m²).

- Berlin again takes second place at EUR 9.85/m² (up 9.4% from EUR 9.00/m²).

- Stuttgart is in third place at EUR 8.40/m², after sharing this spot (with Hamburg) in the previous year at EUR 7.80/m², an increase of 7.7%.

- Fourth place is shared by the Hamburg market, previously in third, at EUR 8.25/m² and up from EUR 7.80/m² (up 5.8%), and the Düsseldorf market, also at EUR 8.25/m², which has climbed from seventh place to EUR 7.15/m² (up 15.4%, the highest increase across all top markets).

- In sixth place (as fourth place is shared) is the Cologne market at EUR 8.00/m² after EUR 7.00/m² (up 14.3%).

- Frankfurt is in second to last place at EUR 7.90/m², coming from EUR 7.30/m² (up 8.2%).

The market with the lowest prices in the top eight is again the Ruhr area at EUR 7.25/m² after EUR 6.50/m² (up 11.5%), which means that prime rents of less than EUR 7.00/m² can no longer be found on any market.

REALOGIS media contact:

Silke Westermann

Senior public relations specialist

Tel: +49/211/53 88 3-440

e-mail: s.westermann@shcommunication.de

REALOGIS company contact:

REALOGIS Holding GmbH

Silja Schuppler

Marketing

Rundfunkplatz 4, 80335 Munich

Tel: +49/89/51 55 69 17

e-mail: s.schuppler@realogis.de

www.realogis.de

REALOGIS. No. 1 for industrial and logistics properties

The REALOGIS Group is Germany’s leading player for the consulting and brokering of industrial, logistics and commercial properties. Founded in 2005 as a pioneer for the asset class of logistics and industry, the owner-operated group has enjoyed healthy growth, is crisis-resistant and knows the German market like no other. In 2022 Realogis generated nearly 1.25 million m² of usable space alone in the letting segment (preliminary result). The net commission revenue of all services in the financial year 2022 are EUR 22.74 million (preliminary result).

In 2021, REALOGIS also won the German Real Estate Prize in the “Commercial Player” category, which honours companies for their outstanding commitment, creativity, innovative strength and sustainability.

Realogis is represented in the country’s seven top logistics locations of Berlin, Düsseldorf, Frankfurt am Main, Hamburg, Leipzig, Munich and Stuttgart, while a dedicated organisational unit ensures transparency in around 15 additional regional logistics markets. 70 real estate professionals advise national and international companies from the fields of logistics, e-commerce, retail and industry as well as private and institutional investors. Quick, flexible, regional, customer-oriented and with a high volume of transactions.

REALOGIS four core competencies are arranging highly creditworthy tenants for new and existing properties, assisting investors with property investments and project development of greenfields and brownfields, outstanding service for locating or selling sites, and the development and implementation of holistic property strategies.

In short, REALOGIS creates more room for its customers’ success in every sense. Further information: https://www.realogis.de/