HOCHWERTIG | 650 m² HALLE | 800 m² AUSSTELLUNG

ID: 998947DetailsGarching, repräsentatives Produktionsgebäude mit hochwertigen Büroflächen

ID: 93135Detailsca. 400 m² große, ebenerdige Lager-Produktionshalle mit Meisterbüro in Top Lage

ID: 1036679DetailsDirekt am Autobahnkreuz Ulm/Elchingen - Neubau multifunktionaler Logistik- und Produktionsflächen

ID: 994300DetailsLOGISTIK | RAMPEN | FREIFLÄCHE

ID: 1008605DetailsLager-/Logistik | Neubau | Rampen | teilbar | ebenerdig

ID: 1016255DetailsGEWERBEPARK | ERSTBEZUG | TOP-LAGE

ID: 996681DetailsBremen, ca. 1.300 m² Lager-/ Logistikfläche zu vermieten

ID: 1032273DetailsMünchen - Nord, Hallen- und Freiflächen in Bestlage zu vermieten

ID: 101077DetailsPROVISIONSFREI | GEWERBEPARK | FLEXIBEL

ID: 1000973DetailsArnsdorf | ca. 9.000 m² | Lager & Logistik | Betonrampe & ebenerdig | teilbar ab 2.000

ID: 1009874DetailsRepräsentativer Gewerbepark

ID: 1005086Detailsca. 1.350 m² große, ebenerdige Hallenfläche mit Büro

ID: 1035432DetailsPRODUKTION | LAGER | RAMPE

ID: 991522DetailsGarching, Neubau von ca. 8.000 m² Lager-,Forschungs- und Bürofläche

ID: 1030576DetailsMunich-North, warehouse and office spaces for rent

ID: 1033335DetailsMunich-North, warehouse and office spaces for rent

ID: 1024609DetailsMunich-North, warehouse and office spaces for rent

ID: 1034331DetailsMunich-North, warehouse and office spaces for rent

ID: 1002692DetailsMunich-North, warehouse and office spaces for rent

ID: 1034768DetailsMunich-North, warehouse and office spaces for rent

ID: 1034670DetailsMunich-North, warehouse and office spaces for rent

ID: 1034767DetailsMunich-North, warehouse and office spaces for rent

ID: 1025539DetailsMunich-North, warehouse and office spaces for rent

ID: 1010949DetailsMunich-North, warehouse and office spaces for rent

ID: 1032598DetailsAugsburg, site with about 2.500 sqm for rent

ID: 9040DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031912DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031769DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031836DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1028145DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030724DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030615DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1023871DetailsGladback, warehousing space for wholesale or retail for rent

ID: 95769DetailsGladback, warehousing space for wholesale or retail for rent

ID: 1013489DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1025426DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1026621DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1022435DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1023380DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1014315DetailsNeuss, approx. 1,295 sqm warehouse space in a business park for rent

ID: 997156DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1017665DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1019585Details

Do you have a question? Leave your contact details here and we will call you back!

Press Release

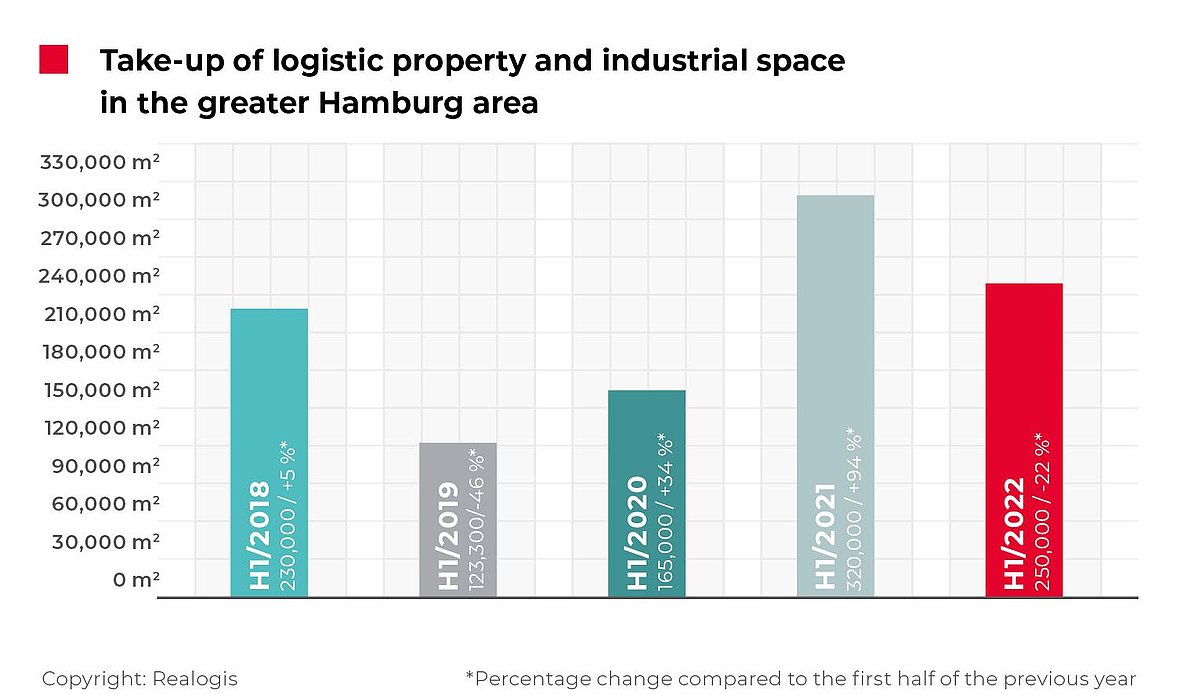

Sharp decline in take-up on the Hamburg industrial and logistics property market

- Short supply kicks in – hardly any development activity

- Every second square metre let in southern Hamburg

- Logistics ahead of retail and industry again

- Large spaces dominate at 65%

- Prime rent climbs to EUR 7.50/m² for the first time

- Outlook: stable demand expected – manufacturing sector to bounce back

“The decline is not due to demand, which remains very stable. The reason for the decline in letting business is the shortage of space across the Hamburg market area, which means there are hardly any new project developments to speak of,” reports Jörg Lojewski, Managing Director of Realogis Immobilien Hamburg GmbH.

At 162,500 m², major deals of 10,000 m² or more were a key factor in the latest result. All five top deals were over the 10,000 m² mark.

Lessors with highest take-up

Company | Region | Take-up | Type | Sector |

Pfaff Logistik GmbH | HH eastern surrounding area | 29,500 m² | Existing property | Logistics |

JYSK SE | HH South | 24,000 m² | New build | Retail |

Bechtle AG | HH South | 18,800 m² | New build | Logistics |

Fiege Logistik | HH East | 18,500 m² | New build | Logistics |

Aldi | HH eastern surrounding area | 15,000 m² | New build | Retail |

“While third-party users dominate the Hamburg market, accounting for 162,500 m² or 65% of take-up, owner-occupiers generated 80,000 m² or 32% of take-up,” explains Stefan Imken, Managing Director of Realogis Immobilien Hamburg GmbH.

Nearly three quarters of all space (73%) was let in “big boxes”. These are properties that are not located in business parks, are used for logistics and have hall space of more than 10,000 m², a height of at least 10 m and an office share of less than 20%. They accounted for 182,500 m². At 23% or 57,500 m², business parks account for just under a quarter of the space, and none of the remaining 10,000 m² was situated in big boxes or traditional business parks.

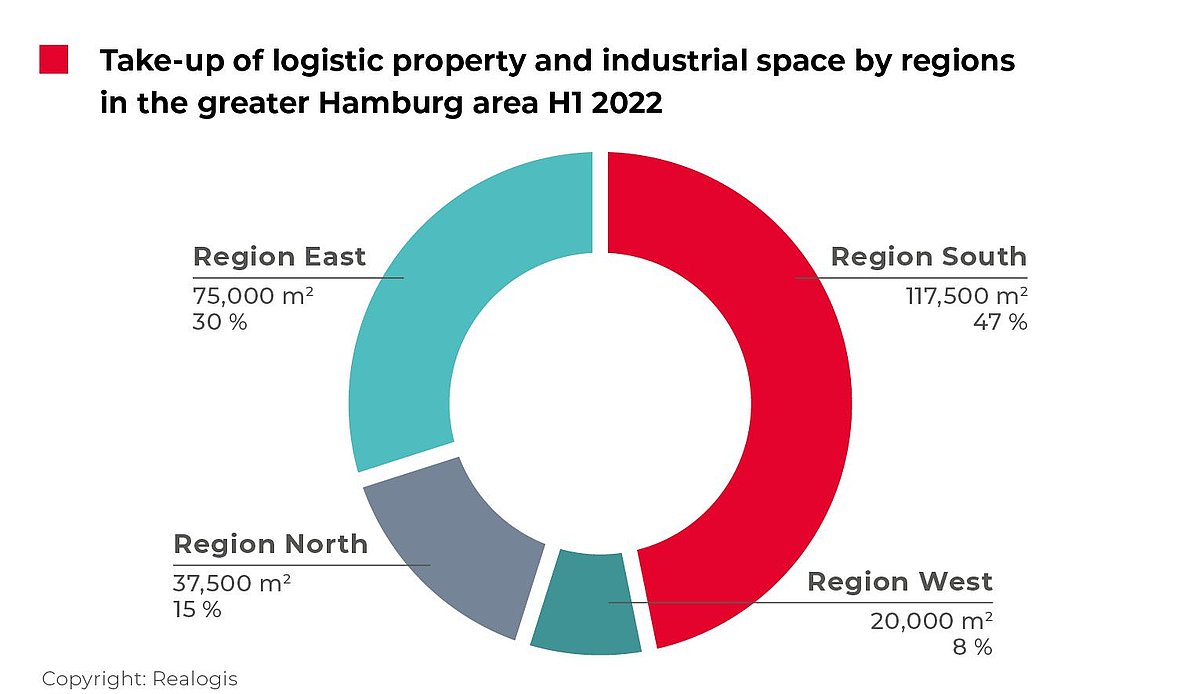

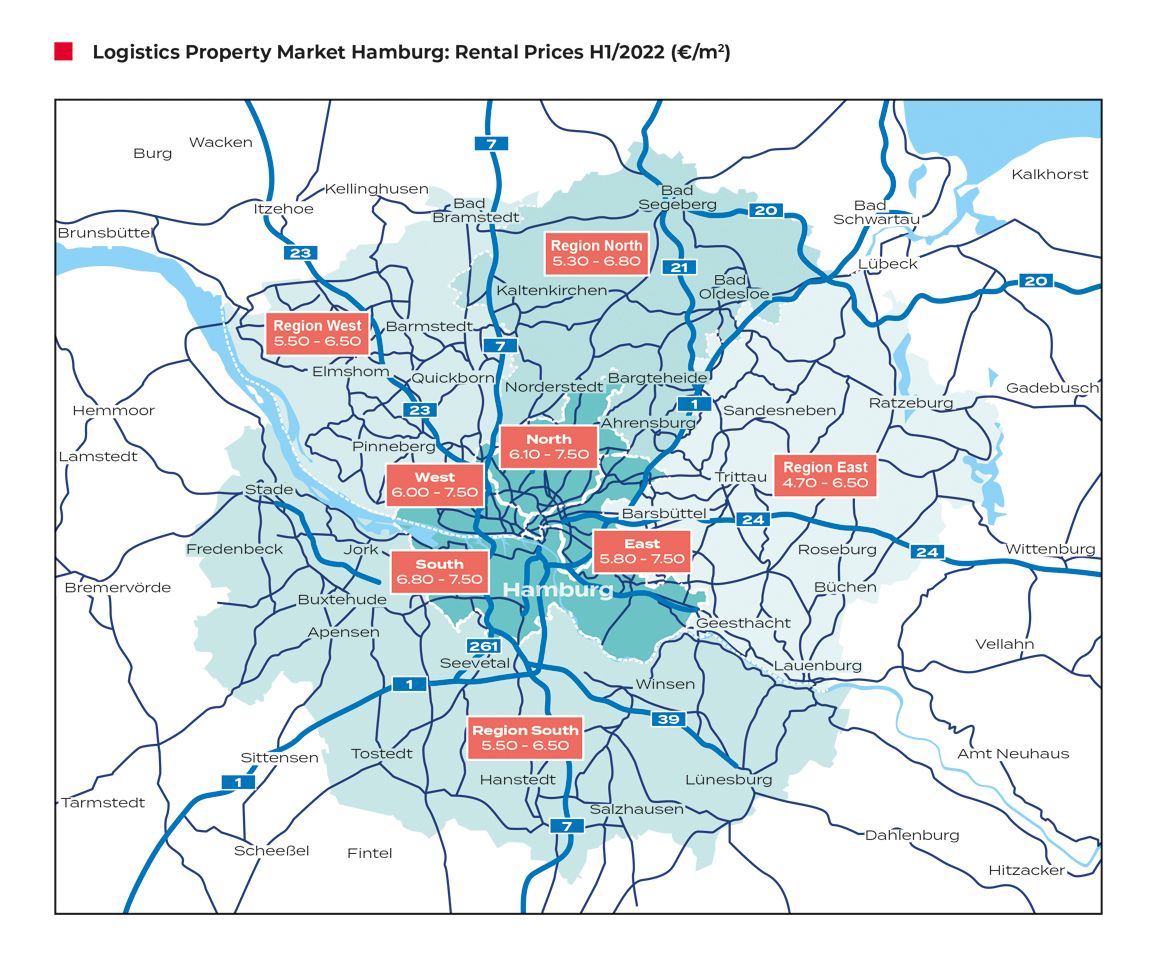

Take-up by region: ranking as in 2021

The South region, the long-established leader, again recorded the highest take-up in the first half of 2022 with a total of 117,500 m² or 47%, accounting for nearly every second square metre let. Compared with the previous year, the South region saw its importance increase slightly by +1.4 percentage points, from 146,000 m² or 45.6%. Two of the top five deals were concluded in the southern surrounding area: the Danish retail chain JYSK SE leased 24,000 m², followed by Bechtle AG with 18,800 m².

The remaining ranking positions are also unchanged: as in the previous year, the East region came second with 75,000 m², representing a share of 30%, compared with 95,000 m² or 29.7% previously. The biggest and the two smallest top take-ups made a key contribution to the total take-up (63,000 m² or 84%): Pfaff Logistik GmbH with 29,500 m², Fiege Logistik with 18,500 m² and Aldi with 15,000 m².

As it did last year, the North region came third with 37,500 m² or 15% (H1 2021: 69,000 m² or 21.6%). It saw the biggest relative decline out of all regions, with pro rata take-up down 6.6 percentage points. In absolute terms, it posted a decrease of 45.6%, the heaviest of all regions year-on-year.

The West region again brought up the rear in the last half-year with 20,000 m² or 8% (H1 2021: 10,000 m² or 3.1%), with take-up also increasing in absolute terms.

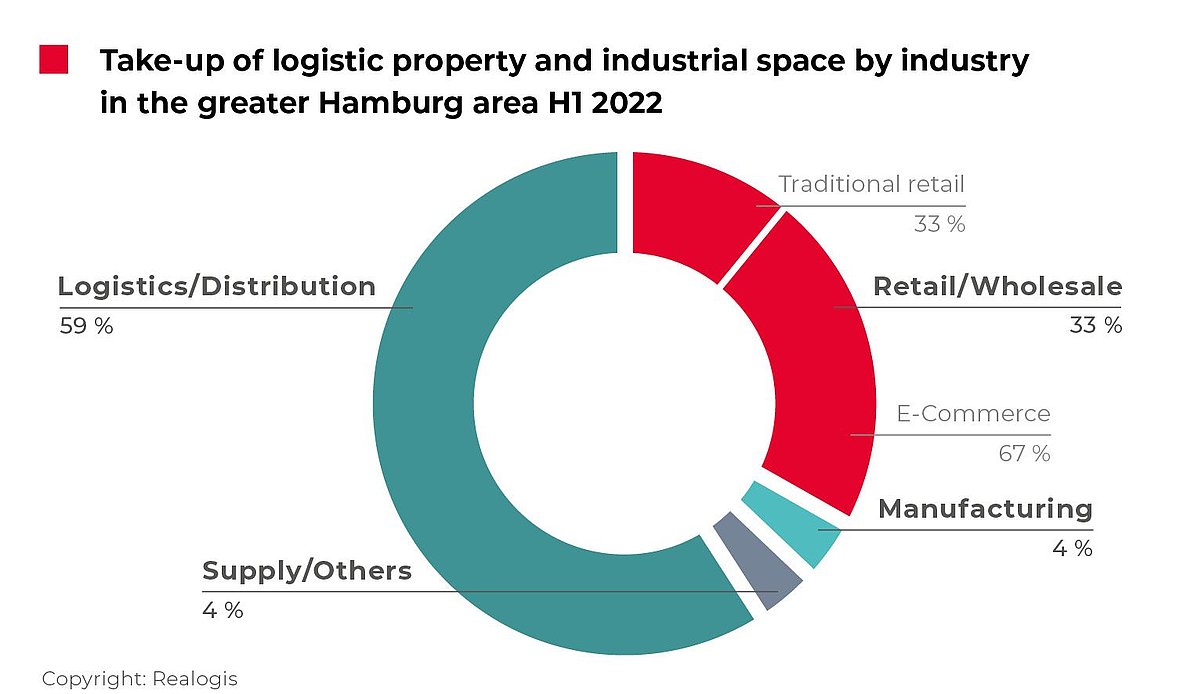

Logistics ahead of retail and industry again

Logistics/distribution has been posting the highest take-up on the Hamburg industrial and logistics property market since the first half of 2016. Take-up in the sector currently amounts to 147,500 m² or a share of 59%. Compared with previous first half-years, this is the highest percentage share, followed by H1 2018, where it came to 58% or 133,400 m².

Three of the top five contributions to take-up came from this sector: in total, Pfaff Logistik GmbH, Bechtle AG and Fiege Logistik posted 66,800 m² or 45.3%.

Retail has been in second place since H1 2016. This sector recorded a combined 82,500 m² or 33% of total take-up. Traditional retail was the main contributor here with 55,000 m² or 66.7%, while e-commerce amounted to 27,500 m² or 33.3%. In total, the top deals by JYSK SE and Aldi accounted for 39,000 m² or 70.9% of take-up by traditional retail.

Manufacturing and the miscellaneous category “Other” came joint third with 10,000 m² or 4% each: none of the current top deals were made in these sectors. At -12 percentage points, manufacturing saw the sharpest decline in relative share, by more than 40,000 m² in absolute terms (H1 2021: 51,200 m² or 16%).

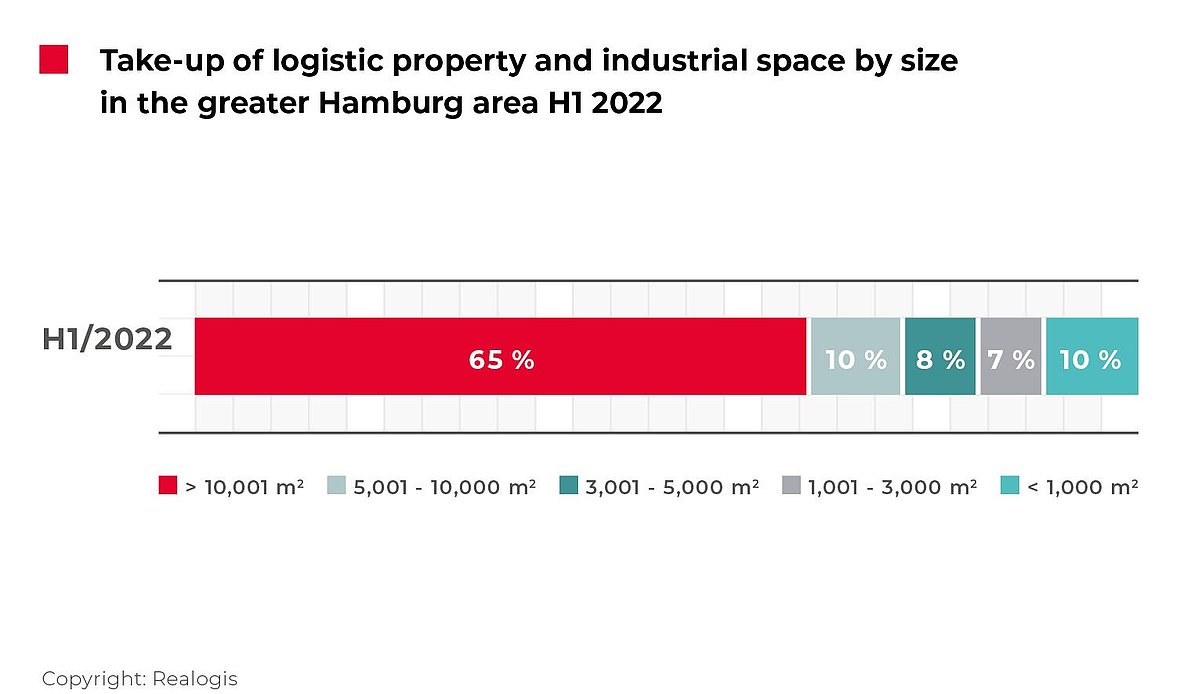

Large spaces dominate at 65%

As in the same period of the previous year, all top deals were concluded in the 10,000 m² and above size category, which helped to secure first place for this category once again, with 162,500 m² or 65% (H1 2021: 169,600 m²).

In the last six months, larger spaces between 5,001 and 10,000 m² accounted for 10% of space or 25,000 m², taking second place (H1 2021: 48,000 m² or 15%).

Medium-sized to larger spaces between 3,001 and 5,000 m² currently occupy third place with 20,000 m² or 8% (H1 2021: 28,800 or 9%). Smaller spaces between 1,001 and 3,000 m² came bottom with 17,500 m² or 7% (H1 2021: 57,600 m² or 18%; -11 percentage points or a decrease of just under 70% in absolute terms).

The only size category where take-up increased in absolute terms is the smallest spaces of less than 1,000 m². With total take-up of 25,000 m² or 10% of the total market, they posted a rise of 56.3% (H1 2021: 16,000 m² or 5%), taking joint second place alongside larger spaces.

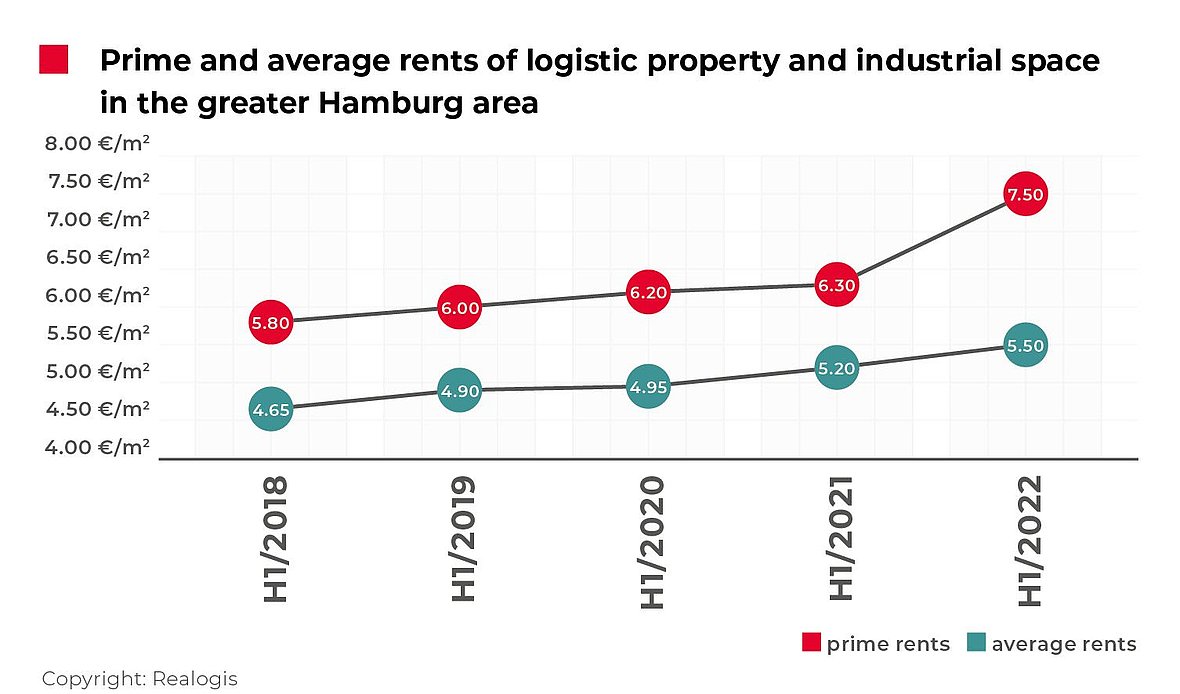

Prime rent climbs to EUR 7.50/m² for the first time

With a rise of 19%, the first half of 2022 saw the highest increase in prime rent since records began at Realogis. The highest level to date is EUR 7.50/m², compared with EUR 6.30/m² in H1 2021, which represents a significant difference of EUR 1.20/m². The five-year average of EUR 6.36/m² was exceeded by some 17.9%.

“The reason for the sharp rise in prime rent is the shortage of space and the increase in construction costs and land prices,” reports Jörg Lojewski. “Material shortages and increased material costs are making it increasingly difficult for project developers to calculate construction costs and factor them into rents. This leads to rising costs during the construction phase, which general contractors pass on to developers through price escalation clauses,” says Jörg Lojewski.

Average rent is also rising dynamically, albeit much more moderately than the development of prime rent. In the first half of 2022, it rose by 5.8% to EUR 5.50/m², from EUR 5.20/m² in H1 2021. Average rent is 9.1% higher than the current five-year average of €5.04/m².

Outlook

It remains to be seen how the war in Ukraine and the disrupted supply chains will affect the Hamburg economy, which depends on exports via its port, up until the end of the year. Realogis expects stable demand in all size categories along with shrinking supply and equally few new construction projects up until the end of 2022. For these reasons, Realogis expects total take-up of around 450,000 m² up until the end of the year.

REALOGIS press contact:

SH/Communication – Public Relations Agency

Silke Westermann

Press

Fritz-Vomfelde-Strasse 34, 40547 Düsseldorf

Tel: +49/211/53 88 3-440

e-mail: s.westermann@shcommunication.de

REALOGIS company contact:

REALOGIS Holding GmbH

Silja Schuppler

Marketing

Rundfunkplatz 4, 80335 Munich

Tel: +49/89/51 55 69 17

e-mail: s.schuppler@realogis.de

www.realogis.de

REALOGIS. No. 1 for industrial and logistics properties

The REALOGIS Group is Germany’s leading player for the consulting and brokering of industrial, logistics and commercial properties. Founded in 2005 as a pioneer for the asset class of logistics and industry, the owner-operated group has enjoyed healthy growth, is crisis-resistant and knows the German market like no other. In 2021 Realogis generated nearly 1,3 million m² of usable space alone in the letting segment. The net commission revenue of all services in the financial year 2021 are EUR 25 million.

In 2021, REALOGIS also won the German Real Estate Prize in the “Commercial Player” category, which honours companies for their outstanding commitment, creativity, innovative strength and sustainability.

Realogis is represented in the country’s seven top logistics locations of Berlin, Düsseldorf, Frankfurt am Main, Hamburg, Leipzig, Munich and Stuttgart, while a dedicated organisational unit ensures transparency in around 15 additional regional logistics markets. 70 real estate professionals advise national and international companies from the fields of logistics, e-commerce, retail and industry as well as private and institutional investors. Quick, flexible, regional, customer-oriented and with a high volume of transactions.

REALOGIS four core competencies are arranging highly creditworthy tenants for new and existing properties, assisting investors with property investments and project development of greenfields and brownfields, outstanding service for locating or selling sites, and the development and implementation of holistic property strategies.

In short, REALOGIS creates more room for its customers’ success in every sense. Further information: https://www.realogis.de/