HOCHWERTIG | 650 m² HALLE | 800 m² AUSSTELLUNG

ID: 998947DetailsGarching, repräsentatives Produktionsgebäude mit hochwertigen Büroflächen

ID: 93135Detailsca. 400 m² große, ebenerdige Lager-Produktionshalle mit Meisterbüro in Top Lage

ID: 1036679DetailsDirekt am Autobahnkreuz Ulm/Elchingen - Neubau multifunktionaler Logistik- und Produktionsflächen

ID: 994300DetailsLOGISTIK | RAMPEN | FREIFLÄCHE

ID: 1008605DetailsLager-/Logistik | Neubau | Rampen | teilbar | ebenerdig

ID: 1016255DetailsGEWERBEPARK | ERSTBEZUG | TOP-LAGE

ID: 996681DetailsBremen, ca. 1.300 m² Lager-/ Logistikfläche zu vermieten

ID: 1032273DetailsMünchen - Nord, Hallen- und Freiflächen in Bestlage zu vermieten

ID: 101077DetailsPROVISIONSFREI | GEWERBEPARK | FLEXIBEL

ID: 1000973DetailsArnsdorf | ca. 9.000 m² | Lager & Logistik | Betonrampe & ebenerdig | teilbar ab 2.000

ID: 1009874DetailsRepräsentativer Gewerbepark

ID: 1005086Detailsca. 1.350 m² große, ebenerdige Hallenfläche mit Büro

ID: 1035432DetailsPRODUKTION | LAGER | RAMPE

ID: 991522DetailsGarching, Neubau von ca. 8.000 m² Lager-,Forschungs- und Bürofläche

ID: 1030576DetailsMunich-North, warehouse and office spaces for rent

ID: 1033335DetailsMunich-North, warehouse and office spaces for rent

ID: 1024609DetailsMunich-North, warehouse and office spaces for rent

ID: 1034331DetailsMunich-North, warehouse and office spaces for rent

ID: 1002692DetailsMunich-North, warehouse and office spaces for rent

ID: 1034768DetailsMunich-North, warehouse and office spaces for rent

ID: 1034670DetailsMunich-North, warehouse and office spaces for rent

ID: 1034767DetailsMunich-North, warehouse and office spaces for rent

ID: 1025539DetailsMunich-North, warehouse and office spaces for rent

ID: 1010949DetailsMunich-North, warehouse and office spaces for rent

ID: 1032598DetailsAugsburg, site with about 2.500 sqm for rent

ID: 9040DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031912DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031769DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031836DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1028145DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030724DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030615DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1023871DetailsGladback, warehousing space for wholesale or retail for rent

ID: 95769DetailsGladback, warehousing space for wholesale or retail for rent

ID: 1013489DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1025426DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1026621DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1022435DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1023380DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1014315DetailsNeuss, approx. 1,295 sqm warehouse space in a business park for rent

ID: 997156DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1017665DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1019585Details

Do you have a question? Leave your contact details here and we will call you back!

Press Release

Setback for the Hamburg logistics market

- This year’s result for all market participants around 22% lower than top result of 2021

- Only slightly below five-year average

- Big boxes responsible for three-quarters of all new lettings

- Top seven lessees account for 40% of take-up

- Restraint on the investment and project development market

- Muted forecast for 2023

- Hamburg South leads the region ranking once again

- Retail overtakes logistics to top the sector ranking

- Two size segments are responsible for around 80% of take-up

- Prime rent climbs by 16.4%

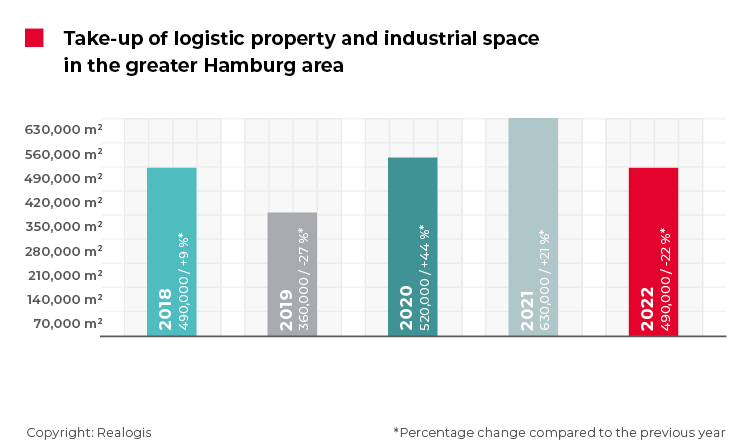

Hamburg, 13 January 2023 – The Hamburg market for warehouse, logistics and industrial space failed to maintain the previous year’s strong result of 630,000 m² of rental space brokered by all market participants, slipping by a considerable 22.2% to 490,000 m². This is revealed by Realogis, Germany’s leading consultancy for industrial and logistics properties and business parks, in its latest market report.

“After two consecutive years of clear growth, this is a significant setback for the market,” says Jörg Lojewski, Managing Director of Realogis Immobilien Hamburg GmbH. “2022 was again characterised by a very limited supply of space at the same time as high underlying demand.”

However, the current figure is only 2% lower than the five-year average of 498,000 m². In 2018, exactly the same amount of space was brokered as in 2022. In 2019, take-up was only 360,000 m².

“A positive factor is the large number of high-volume deals for units of more than 20,000 m²,” reports Stefan Imken, Managing Director of Realogis Immobilien Hamburg GmbH. Big boxes – properties of 10,000 m² or more, with logistics as the main type of use and an office share of no more than 20% – made a crucial contribution to take-up. They took three-quarters of all space brokered in the reporting period, or 372,400 m².

Business parks accounted for 21% or 102,900 m². Realogis defines a business park as a contiguous business district that is developed and implemented with a uniform concept and whose infrastructure is used jointly by the companies based there.

Other space not allocated to either the big box or business park categories accounted for 3% or 14,700 m².

In 2022, more than two-thirds (328,300 m²) of the Hamburg industrial and logistics property rental market related to deals in properties not owned by the user. Around 30% or 147,000 m² was attributable to owner-occupiers and another 3% or 14,700 m² to properties of unknown ownership.

Top seven lessees account for 40% of take-up

The seven top lessees together account for space of 196,000 m², contributing 40% of total take-up. This includes the three largest deals: Aldi (42,500 m²), Airbus (30,000 m²) and Pfaff Logistik GmbH (29,500 m²). Pfaff Logistik GmbH also signed one of the seven biggest leases in the previous year 2021 with a deal for 17,500 m² south of Hamburg.

According to the Realogis analysis, five of the seven top deals, or 136,500 m², were made in new logistics buildings, including the biggest deal of the year as a whole, which saw Aldi take up 40,000 m².

Top lessees in full-year 2022 in Greater Hamburg

Company | Region | Take-up | Type | Sector |

Aldi | HH southern surrounding are | 42,500 m² | New build | Retail |

Airbus | HH South | 30,000 m² | Existing property | Manufacturing |

Pfaff Logistik GmbH | HH eastern surrounding area | 29,500 m² | Existing property | Logistics |

Picnic | HH northern surrounding area | 25,000 m² | New build | Retail |

JYSK SE | HH South | 24,000 m² | New build | Retail |

Worlée | HH East | 23,000 m² | New build | Logistics |

Sobuy | HH eastern surrounding area | 22,000 m² | New build | Retail |

Restraint on the investment and project development market

“Investors and project developers are deferring many of their pre-purchase checks. The reasons include interest rate policy and in some cases uncertainty over the calculation of construction costs,” explains Jörg Lojewski.

“Usage-based ancillary costs, especially for gas and electricity, are becoming ever more important to users’ decision-making,” says Jörg Lojewski. “Current owners of older buildings are therefore compelled to optimise their properties. Institutional developers’ new buildings are mostly being built only with PV systems and alternatives to gas heating, such as heat pumps,” says Jörg Lojewski.

Forecast for 2023

“The development of the Hamburg logistics market in 2023 will depend in particular on economic development, for which a minor recession has been predicted. Moreover, it remains to be seen how energy costs will develop over the course of the year,” says Stefan Imken. “Nevertheless, the signs for the warehouse and logistics asset class in Hamburg, including the metropolitan areas, are positive. We assume that retail – especially e-commerce – will increase its presence in the Hamburg market. The proximity to the container terminals and the very good infrastructure are pivotal here.”

Due to the reduced supply, Realogis expects all market participants to achieve total take-up of around 400,000 m² in 2023.

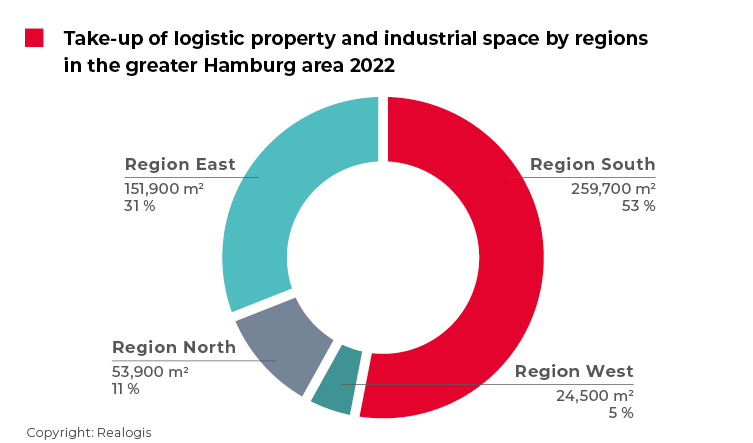

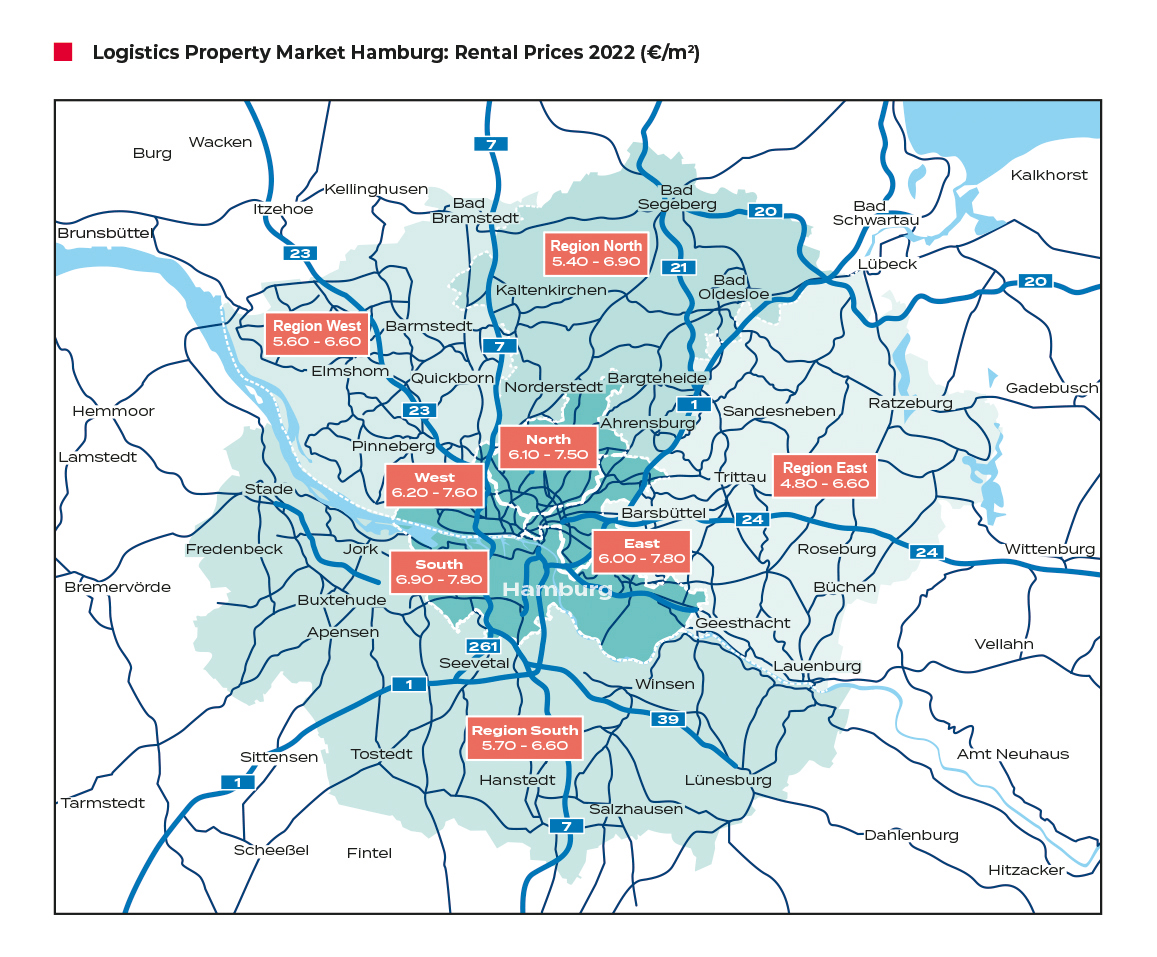

Hamburg South again the region with the highest take-up

In 2022, the most in-demand region was Hamburg South with more than half of all take-up, or 259,700 m². It has thus been in the top spot since 2018. Of all regions, it gained the most ground year on year, with its share rising 7.8 percentage points (as against 285,000 m² or 45.2% in 2021 as a whole). Due to the reduction in the overall market for industrial and logistics properties in Hamburg, all regions declined in terms of absolute take-up, but the south saw the most moderate decline at 8.9%.

Hamburg South was the location of the largest deal by Aldi for 42,500 m² (surrounding area) as well as the second-largest deal by Airbus for 30,000 m² (city) and the JYSK SE deal for 24,000 m² (city). Together, these deals amounted to 96,500 m² or a third of the region’s take-up.

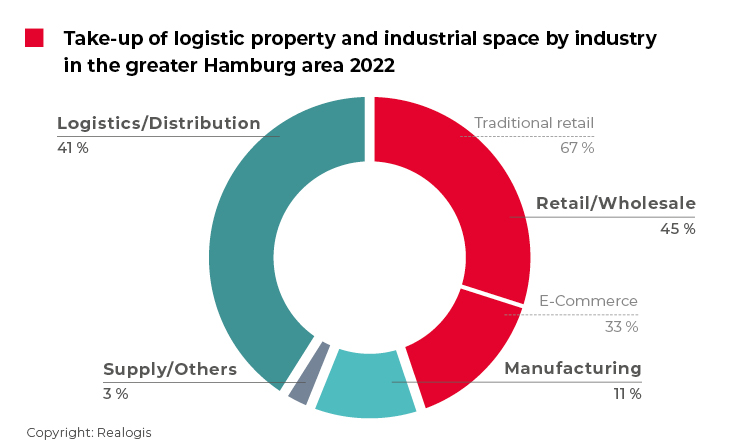

Retail overtakes logistics to top the sector ranking

Logistics/distribution is typically the leading sector in the Hamburg industrial and logistics property rental market. In 2022, however, retail tops the sector ranking with 220,500 m² or 45%. The four lessees with the highest take-up are Aldi, Picnic, JYSK SE and Sobuy, which together account for 113,500 m² or half of the take-up. Within retail, traditional retail dominates with a share of two-thirds or 147,000 m², followed by e-commerce with 73,500 m² or a share of 33%.

Coming in second is the usually first-placed logistics/distribution sector with take-up of 200,000 m² or 41%. Compared with 371,700 m² or 59% in 2021, logistics/distribution took a veritable nosedive, losing 18 percentage points of share in the sector view and almost half of its take-up in absolute terms (down 46%, 171,700 m²). The top two deals in the logistics/distribution sector are attributable to Pfaff Logistik GmbH and Worlée with cumulative take-up of 52,500 m² or 26.3%.

Since 2018, third place has consistently been held by the manufacturing sector with currently 55,000 m² or 11% after 69,300 m² and likewise a share of 11%. The sector’s relative share is therefore unchanged year on year despite an absolute decline of 21%. The top deal by Airbus accounts for 54% of the sector’s take-up.

In last place since 2018 is the “Other” category with 14,500 m² or a share of 3%. Compared with 44,100 m² and 7%, it has both lower relative share (down 4 percentage points) and lower absolute take-up (the largest decline of all sectors at 67%).

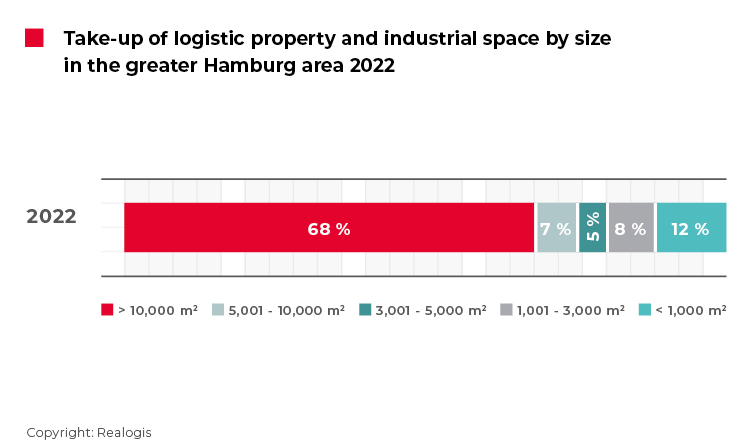

Two size segments are responsible for around 80% of take-up

As in the previous year, large spaces of 10,000 m² or more accounted for the biggest market share at 68% or 333,200 m² and further extended their lead in 2022 (up 16 percentage points from 327,600 m² or 52%). All of the top seven deals were in this category and accounted for around 60% of take-up.

The size category of spaces between 5,001 and 10,000 m² was in fourth place with 34,300m² or 7% (compared with 75,600 m² or 12%, its relative share therefore dropped 5 percentage points).

The 3,001 to 5,000 m² size category is currently in last place with 24,500 m² or 5% (compared with 44,100 m² or 7%, relative share down 2 percentage points). Medium-sized to smaller spaces between 1,001 and 3,000 m² accounted for 39,200 m² or 8% of the space and are currently in third place.

The smallest spaces of less than 1,000 m² are in second place with 58,800 m² or 12%. Together with large spaces, they cover 80% or four-fifths of the square metres let.

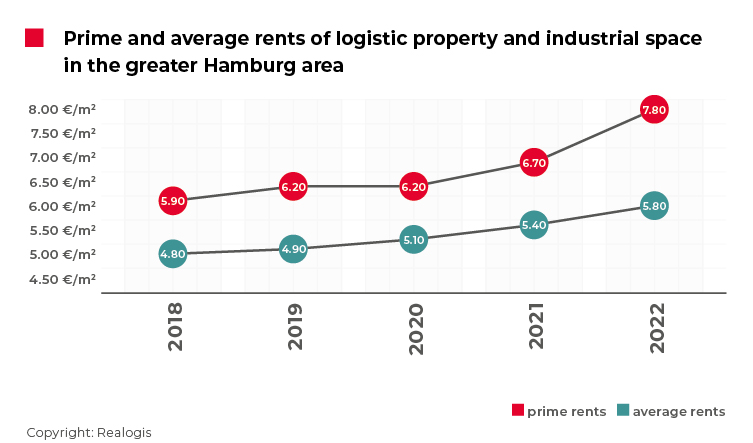

Prime rent climbs by 16.4%

“Prime rent has reached its new provisional high of EUR 7.80/m²,” says Jörg Lojewski. “Here, a shortage of space is coming up against continuously good demand, high construction costs and high purchase prices for land.”

Compared with EUR 6.70/m² at the end of 2021, the 16.4% increase in rent is the strongest growth ever recorded by Realogis. As a result, the five-year average of EUR 6.56/m² is also being exceeded by a significant 18.9%.

Average rent has also reached its latest peak with growth of 7.4% to EUR 5.80/m². Average rent is currently 7.4% above the five-year average of EUR 5.20/m².

REALOGIS media contact:

Silke Westermann

Senior public relations specialist

Tel: +49/211/53 88 3-440

e-mail: s.westermann@shcommunication.de

REALOGIS company contact:

REALOGIS Holding GmbH

Silja Schuppler

Marketing

Rundfunkplatz 4, 80335 Munich

Tel: +49/89/51 55 69 17

e-mail: s.schuppler@realogis.de

www.realogis.de

REALOGIS. No. 1 for industrial and logistics properties

The REALOGIS Group is Germany’s leading player for the consulting and brokering of industrial, logistics and commercial properties. Founded in 2005 as a pioneer for the asset class of logistics and industry, the owner-operated group has enjoyed healthy growth, is crisis-resistant and knows the German market like no other. In 2021 Realogis generated nearly 1,3 million m² of usable space alone in the letting segment. The net commission revenue of all services in the financial year 2021 are EUR 25 million.

In 2021, REALOGIS also won the German Real Estate Prize in the “Commercial Player” category, which honours companies for their outstanding commitment, creativity, innovative strength and sustainability.

Realogis is represented in the country’s seven top logistics locations of Berlin, Düsseldorf, Frankfurt am Main, Hamburg, Leipzig, Munich and Stuttgart, while a dedicated organisational unit ensures transparency in around 15 additional regional logistics markets. 70 real estate professionals advise national and international companies from the fields of logistics, e-commerce, retail and industry as well as private and institutional investors. Quick, flexible, regional, customer-oriented and with a high volume of transactions.

REALOGIS four core competencies are arranging highly creditworthy tenants for new and existing properties, assisting investors with property investments and project development of greenfields and brownfields, outstanding service for locating or selling sites, and the development and implementation of holistic property strategies.

In short, REALOGIS creates more room for its customers’ success in every sense. Further information: www.realogis.de