HOCHWERTIG | 650 m² HALLE | 800 m² AUSSTELLUNG

ID: 998947DetailsGarching, repräsentatives Produktionsgebäude mit hochwertigen Büroflächen

ID: 93135Detailsca. 400 m² große, ebenerdige Lager-Produktionshalle mit Meisterbüro in Top Lage

ID: 1036679DetailsDirekt am Autobahnkreuz Ulm/Elchingen - Neubau multifunktionaler Logistik- und Produktionsflächen

ID: 994300DetailsLOGISTIK | RAMPEN | FREIFLÄCHE

ID: 1008605DetailsLager-/Logistik | Neubau | Rampen | teilbar | ebenerdig

ID: 1016255DetailsGEWERBEPARK | ERSTBEZUG | TOP-LAGE

ID: 996681DetailsBremen, ca. 1.300 m² Lager-/ Logistikfläche zu vermieten

ID: 1032273DetailsMünchen - Nord, Hallen- und Freiflächen in Bestlage zu vermieten

ID: 101077DetailsPROVISIONSFREI | GEWERBEPARK | FLEXIBEL

ID: 1000973DetailsArnsdorf | ca. 9.000 m² | Lager & Logistik | Betonrampe & ebenerdig | teilbar ab 2.000

ID: 1009874DetailsRepräsentativer Gewerbepark

ID: 1005086Detailsca. 1.350 m² große, ebenerdige Hallenfläche mit Büro

ID: 1035432DetailsPRODUKTION | LAGER | RAMPE

ID: 991522DetailsGarching, Neubau von ca. 8.000 m² Lager-,Forschungs- und Bürofläche

ID: 1030576DetailsMunich-North, warehouse and office spaces for rent

ID: 1033335DetailsMunich-North, warehouse and office spaces for rent

ID: 1024609DetailsMunich-North, warehouse and office spaces for rent

ID: 1034331DetailsMunich-North, warehouse and office spaces for rent

ID: 1002692DetailsMunich-North, warehouse and office spaces for rent

ID: 1034768DetailsMunich-North, warehouse and office spaces for rent

ID: 1034670DetailsMunich-North, warehouse and office spaces for rent

ID: 1034767DetailsMunich-North, warehouse and office spaces for rent

ID: 1025539DetailsMunich-North, warehouse and office spaces for rent

ID: 1010949DetailsMunich-North, warehouse and office spaces for rent

ID: 1032598DetailsAugsburg, site with about 2.500 sqm for rent

ID: 9040DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031912DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031769DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031836DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1028145DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030724DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030615DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1023871DetailsGladback, warehousing space for wholesale or retail for rent

ID: 95769DetailsGladback, warehousing space for wholesale or retail for rent

ID: 1013489DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1025426DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1026621DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1022435DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1023380DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1014315DetailsNeuss, approx. 1,295 sqm warehouse space in a business park for rent

ID: 997156DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1017665DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1019585Details

Do you have a question? Leave your contact details here and we will call you back!

Press Release

Munich region: REALOGIS analyses the market for logistics and industrial properties in 2023

Munich, 18 January 2024 – Take-up in the logistics and industrial property rental and owner-occupier market in Munich can reverse the negative trend of the previous year. This is revealed by Realogis, Germany’s leading consultancy for industrial and logistics properties and business parks.

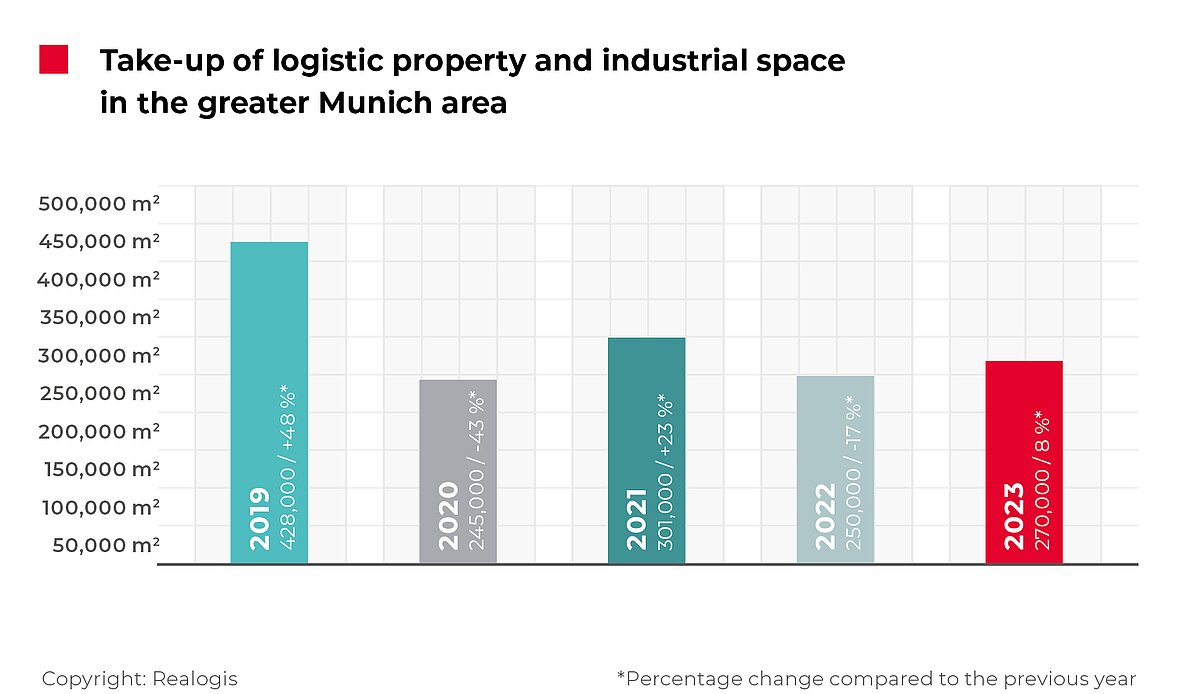

With a total take-up of 270,000 m² achieved by all market participants, the Munich rental and owner-occupier market for logistics and industrial properties grew by 8% or 20,000 m² in 2023, up from 250,000 m² in 2022.

The average take-up of the past five years currently stands at 298,800 m², so 2023 saw a 9.6% shortfall on that figure. In terms of the last 5 annual take-ups, the annual result occupies third position in the middle of the rankings. 2019 and 2021 were higher at 428,000 m² and 301,000 m² respectively, while 2022 and 2020 were lower at 250,000 m² and 245,000 m² respectively.

In 2023, lettings in existing properties accounted for 161,000 m² or 59.6% of total take-up. However, compared with 211,200 m² or 84.5%, they suffered a significant drop of 50,200 m² in absolute terms (-23.8%) and also lost in importance in relative terms with a decline of 24.9 percentage points.

"Brownfields, i.e. the use of sites that have had previous developments on them, did not record any transactions in the reporting period – in contrast to previous years that each saw up to seven projects developed. Instead, owner-occupier and rental transactions in new buildings on greenfield sites in particular significantly increased their importance for the Munich market in 2023 as a whole," reports Nicolas Werner, Managing Director of Realogis Immobilien München GmbH. The total annual take-up of new-build projects was 109,000 m², meaning that the segment grew by a significant 70,200 m² compared to the previous year, representing an almost threefold increase (2022: 38,800 m², +180%). New builds gained 24.9 percentage points in terms of their relative importance in the overall annual result.

Realogis registered a total of 73 deals in the market in the reporting period from January to December 2023. 15 or 21% have a contract term of 10 years or longer, 55% or 40 contracts have a term of between 5 and 9 years and 18 or 25% have a term of less than 5 years. The average term of all contracts is 5.7 years, according to Realogis.

A look at the user structure clearly shows that more space was taken up by owner-occupiers than in 2022. Around 27.6% or 74,600 m² of take-up can be attributed to properties owned by users. Compared with 14,000 m² or a share of 5.6% in 2022 as a whole, this is an increase of 60,600 m². The main drivers behind this are the two top take-ups, one by Group 7 of 60,000 m² and the other by the Raben Group of 11,000 m² (together 71,000 m² or 95%).

In relative terms, owner-occupier contracts increased by 22 percentage points, so that they now account for slightly more than one in four square metres taken up (27.6% share of total take-up). Lettings account for 195,400 m² or 72.4% and thus continue to be key for the overall market. However, compared with 236,000 m² or 94.4% in 2022, they lost importance in absolute and relative terms (-40,600 m² or -17.2 percentage points).

Significant increase in importance of big box logistics properties

Big box logistics properties enjoyed a large take-up in 2023 with a market share of 31.1% or 84,000 m². The top contracts signed by Group 7 (60,000 m²), Yaskawa (10,000 m²) and Dachser (10,000 m²) account for the majority of take-up, totalling 80,000 m² or around 95%.

Business parks (2023: 68,500 m²; 2022: 98,800 m²) and other properties (2023: 117,500 m²; 2022: 156,200 m²) recorded an accumulated take-up of 186,000 m² representing a market share of 68.9% in 2023. Compared with 250,000 m² in 2022, the two categories combined fell by -64,000 m² or 25.6%.

"The market is currently lacking properties that are immediately available, especially in the 10,000 m² and above range. Based on our analysis, major project developments in the Munich metropolitan region starting in 2024 will create a total of 40,000 m² of speculative new-build space. However, most of this won't come onto the market until 2025," announced Nicolas Werner. "Furthermore, built-to-suit projects totalling 60,000 m² are in the planning stage."

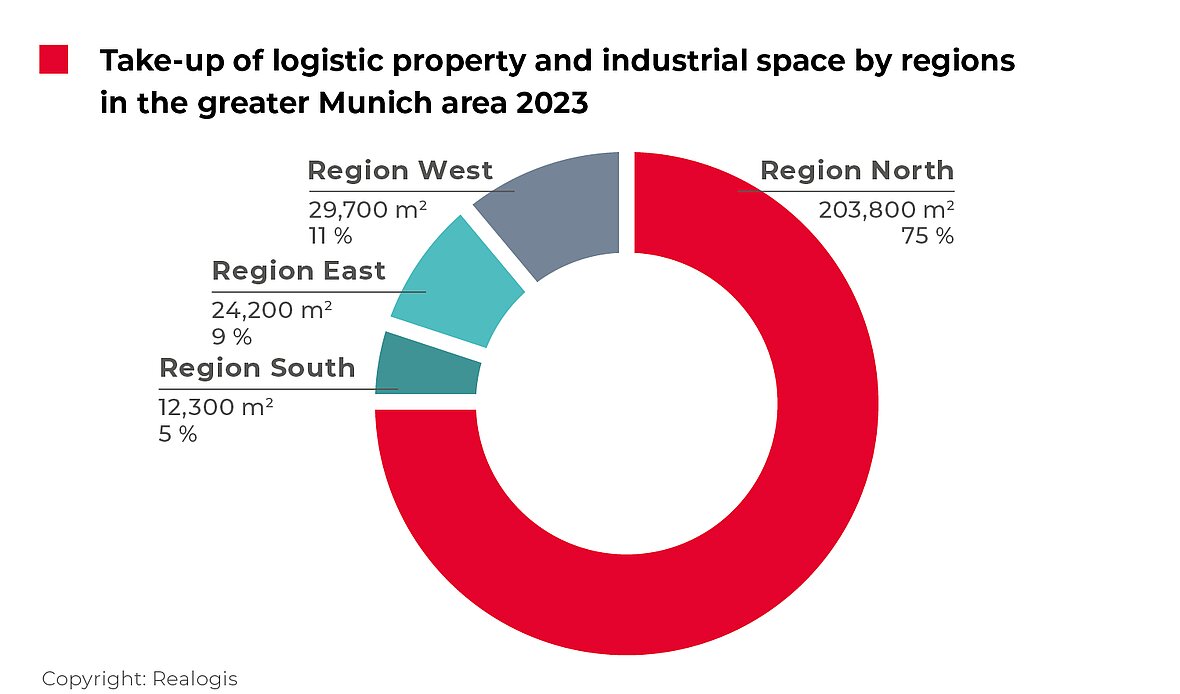

Clear focus on the North region

The distribution of take-up by region is stable compared to the previous year, with no changes to be seen in the rankings. As in previous years, the North region has the highest take-up with 203,800 m² or 75.5% (2022: 94,700 m² or 37.9%). It is the only one of the regions to see an increase in take-up in absolute terms, and this with a very distinct +109,100 m², which is more than double the previous year's figure (+115%). This is also +63% higher than the long-term average of 124,920 m² in the North region.

The region is also the only one to gain in relative importance. At +37.6 percentage points, the region's share is 75.5%, meaning that the North region accounted for more than three out of four square metres of the take-up in the overall market last year.

For the first time: all top sales in just one region

All of the top sales on the Munich industrial and logistics property market were located in the North region in 2023. Its accumulated take-up totalled 121,000 m² or 59% and included the largest deal of the year conducted by Group 7 for 60,000 m².

Lessors with the highest take-up in FY 2023

Company | Market | Region | Take-up | Type | Sector |

Group 7 | North | Schwaig | 60,000 m² | New build | Logistics |

Siemens Mobility | North | Allach | 30,000 m² | Existing property | Industry |

Raben | North | Garching | 11,000 m² | Existing property | Logistics |

Yaskawa | North | Allershausen | 10,000 m² | New build | Industry |

Dachser | North | Allershausen | 10,000 m² | New build | Logistics |

The West region submarket remains in second place with 29,700 m² or 11% (2022: 78,200 m² or 31.3%), but became less important both in absolute terms (-48,500 m² or -62%) and in relative terms (-20.3 percentage points).

The East region follows in third place in terms of take-up with 24,200 m² or 9% (2022: 41,400 m² or 16.6%). In absolute terms, this represents a delta of 17,200 m² or 42% and a proportionate loss of importance of 7.6%.

The South region is in last place with 12,300 m² or a 4.6% pro rata take-up (2022: 35,700 m² or 14.3%; the second most significant slump of all submarkets in absolute terms at 23,400 m² or -66%; this submarket lost 9.7 percentage points pro rata).

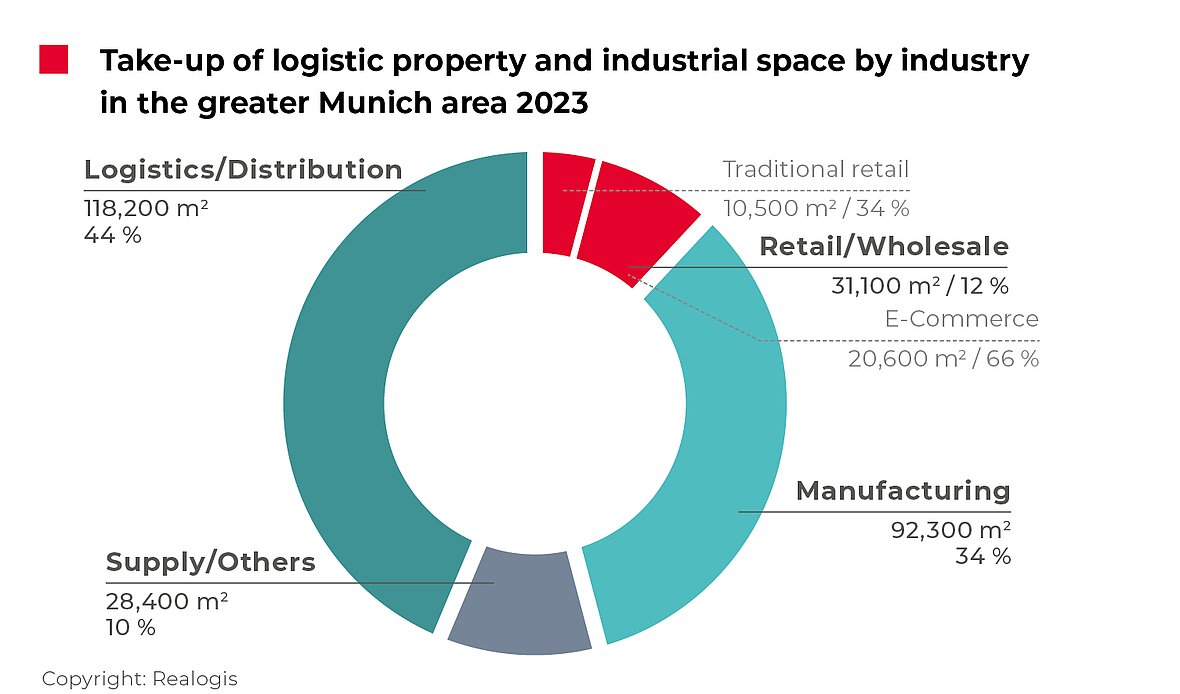

Industry ranking: logistics/distribution back in 1st place

With 118,200 m² or 43.8% in the past year as a whole, logistics/distribution regained the top spot in terms of take-up in the sectors that it last held in 2021, moving up from the second place it occupied in 2022 with 73,500 m² or 29.4%.

"2023 was an above-average year for the logistics/distribution sector in the metropolitan region," notes Nicolas Werner. On the one hand, the result is 28% higher than its 5-year average of 92,320 m² while on the other a significant absolute increase of 44,700 m² or 60.8% and a relative increase of 14.4 percentage points were recorded.

In addition, three of the top deals, totalling 81,000 m² and including the highest, concluded by Group 7, of 60,000 m², are attributable to this sector.

The second strongest demand, at 92,300 m² or 34.2%, was seen from companies in the manufacturing sector, which still required the most space – 100,200 m² or 40.1% – in 2022. This represents a slight decline of 7,900 m² (-7.9%) in absolute terms, with retail the only other sector to experience the same trend. Manufacturing thus shed 5.9 percentage points in relative terms. With a -26% fall, the sector is also below its own 5-year average of 125,000 m². Of the top deals, the lettings by Siemens Mobility (30,000 m²) and Yaskawa (10,000 m²) are allocated to this sector and contribute a total of 40,000 m² or 43%.

Retail remains in third place with 31,100 m² or 11.5% (dropping from 57,200 m² or 22.9% in 2022, this is the most significant absolute decline, totalling 26,100 m² or -45.6% and thus losing close to a half of its previous values). At 46.8%, the retail sector is also well below its 5-year average of 58,600 m². Within the sector, the decline can be attributed in particular to the sub-category of traditional retail. In a year-on-year comparison, this now occupies only second place with figures of 10,500 m² or 33.8%, falling from 44,200 m² and 77.3% and no longer setting the pace (-33,700 m² or -76.2% and also 74% below its own 5-year average of around 40,000 m²).

In contrast, e-commerce accounted for 20,600 m² and thus around two thirds of take-up (66.2%) within the retail sector (+7,600 m² or +58.5% and around 11% higher than its own 5-year average of 18,580 m²).

The miscellaneous category "Other" remains in last place with 28,400 m² or 10.5% (2022: 19,100 m² or 7.6%).

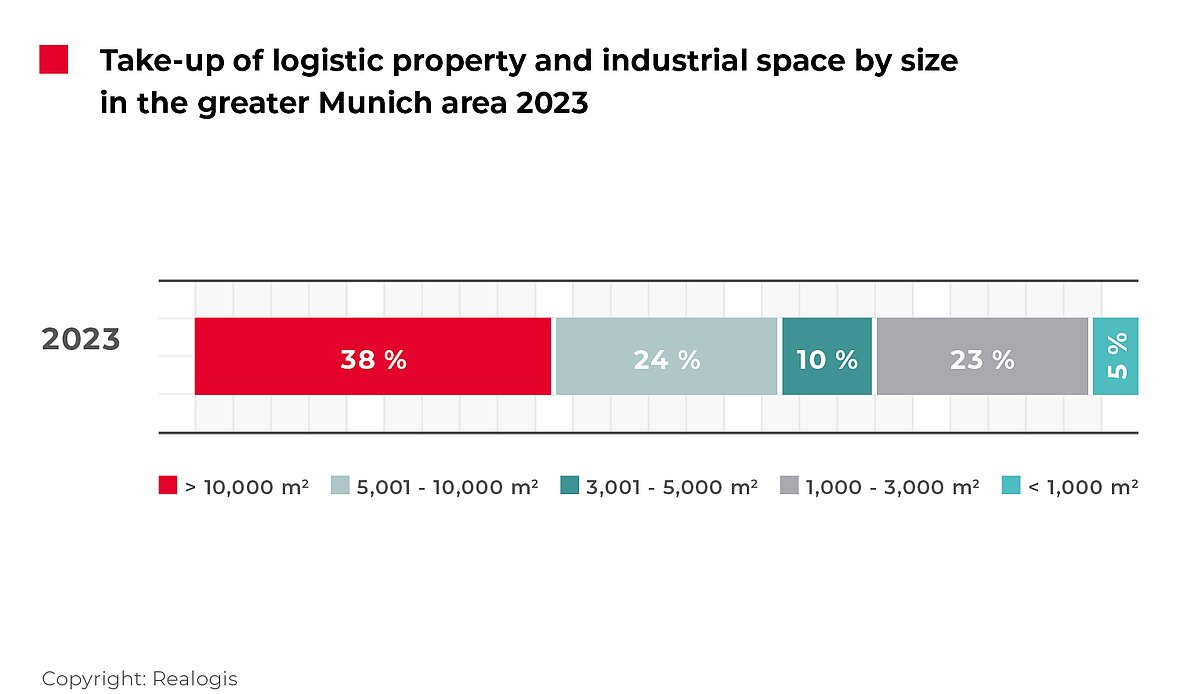

Concentration on large areas

Only the two largest categories were able to increase take-up in 2023. The segment for large spaces of 10,001 m² or more took top spot in the past full year with 101,000 m² or 37.4% and thus climbed three places compared to the previous year (2022: 66,200 m² or 26.5%). The contracts signed by Group 7 (60,000 m²), Siemens Mobility (30,000 m²) and the Raben Group (11,000 m²) are responsible for the total take-up in this size category.

Of all the space categories, large spaces saw the most significant growth in absolute terms, recording an increase of 34,800 m² (+53%). Proportionally, they also gained the most space with an increase of 10.9 percentage points. However, the 5-year average of 114,400 m² was missed by 11.7%.

Larger spaces between 5,001 and 10,000 m² ranked second with 63,900 m² or 23.7%, moving up one place from third place with 44,400 m² or 17.8%. In absolute terms, the increase was 19,500 m² (+44%), while this category gained 5.9 percentage points in proportionate take-up share, and the 5-year average of 58,520 m² was topped by 9.2%. The largest deals include Yaskawa and Dachser, each with 10,000 m² and an accumulated share of 31% within the segment.

Medium to large spaces between 3,001 and 5,000 m² are still in fourth place with 27,950 m² or 10.4% (2022: 36,100 m² or 14.4%; absolute loss: 8,150 m² or -23%; proportionate: -4.1 percentage points).

The size category of small to medium-sized spaces between 1,000 and 3,000 m², which ranked first in the same period of the previous year, lost two places with currently 63,200 m² or 23.4% (2022: 88,800 m² or 35.5%; the most significant decline of all categories with 25,600 m² or -29% and also the most significant proportionate loss of importance with -12.1 percentage points share of take-up).

The smallest spaces of less than 1,000 m² continue to rank last in the past full year at 13,950 m² or 5.2% (2022: 14,500 m² or 5.8%; slight absolute decline of 500 m² or 4%).

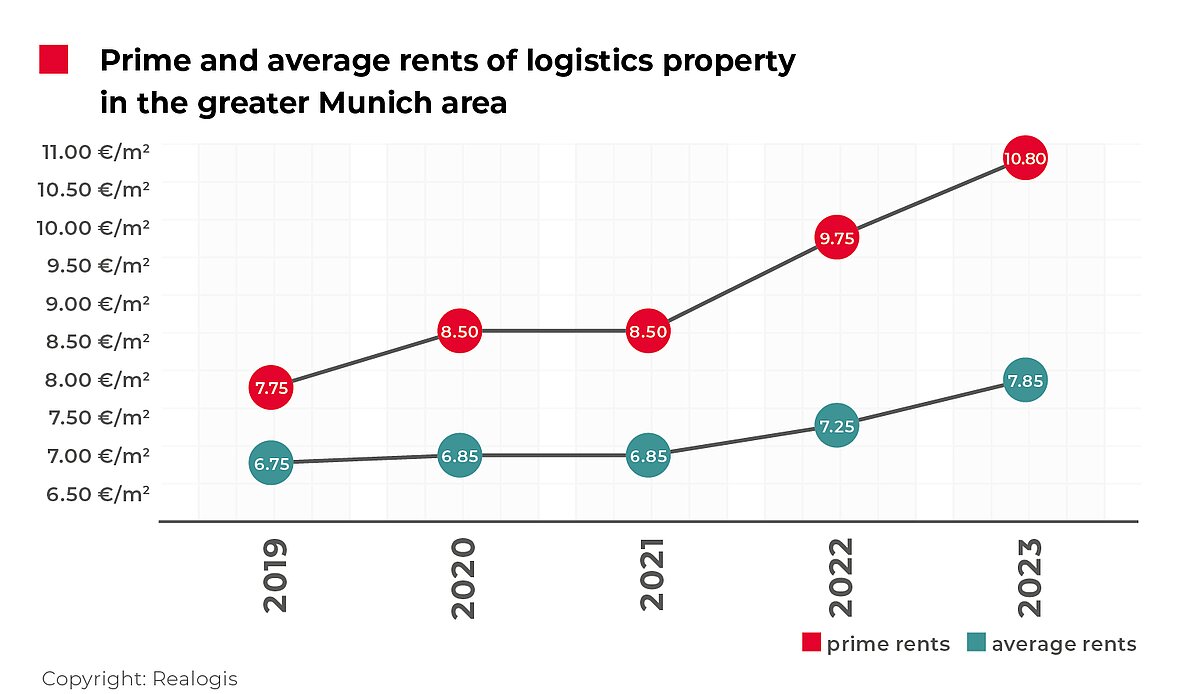

Prime rent above the €10 mark for the first time

The prime rent rose by a significant 10.8% to a new high of €10.80/m², exceeding the €10 mark for the first time for the year as a whole. The 5-year average can be exceeded by 19.2% (€9.06/m²).

The average rent is also continuing to rise, albeit more moderately than the prime rent, with an increase of 8.3% to currently €7.85/m². The 5-year average was topped by 10.4% (€7.11/m²).

REALOGIS media contact:

Silke Westermann

Senior public relations specialist

Tel: +49/211/53 88 3-440

e-mail: s.westermann@shcommunication.de

REALOGIS company contact:

REALOGIS Holding GmbH

Silja Schuppler

Marketing

Rundfunkplatz 4, 80335 Munich

Tel: +49/89/51 55 69 17

e-mail: s.schuppler@realogis.de

www.realogis.de

REALOGIS. No. 1 for industrial and logistics properties

The REALOGIS Group is Germany’s leading player for the consulting and brokering of industrial, logistics and commercial properties. Founded in 2005 as a pioneer for the asset class of logistics and industry, the owner-operated group has enjoyed healthy growth, is crisis-resistant and knows the German market like no other. In 2022 Realogis generated nearly 1.25 million m² of usable space alone in the letting segment (preliminary result). The net commission revenue of all services in the financial year 2022 are EUR 22.74 million (preliminary result).

In 2021, REALOGIS also won the German Real Estate Prize in the “Commercial Player” category, which honours companies for their outstanding commitment, creativity, innovative strength and sustainability.

Realogis is represented in the country’s seven top logistics locations of Berlin, Düsseldorf, Frankfurt am Main, Hamburg, Leipzig, Munich and Stuttgart, while a dedicated organisational unit ensures transparency in around 15 additional regional logistics markets. 70 real estate professionals advise national and international companies from the fields of logistics, e-commerce, retail and industry as well as private and institutional investors. Quick, flexible, regional, customer-oriented and with a high volume of transactions.

REALOGIS four core competencies are arranging highly creditworthy tenants for new and existing properties, assisting investors with property investments and project development of greenfields and brownfields, outstanding service for locating or selling sites, and the development and implementation of holistic property strategies.

In short, REALOGIS creates more room for its customers’ success in every sense. Further information: https://www.realogis.de/