HOCHWERTIG | 650 m² HALLE | 800 m² AUSSTELLUNG

ID: 998947DetailsGarching, repräsentatives Produktionsgebäude mit hochwertigen Büroflächen

ID: 93135Detailsca. 400 m² große, ebenerdige Lager-Produktionshalle mit Meisterbüro in Top Lage

ID: 1036679DetailsDirekt am Autobahnkreuz Ulm/Elchingen - Neubau multifunktionaler Logistik- und Produktionsflächen

ID: 994300DetailsLOGISTIK | RAMPEN | FREIFLÄCHE

ID: 1008605DetailsLager-/Logistik | Neubau | Rampen | teilbar | ebenerdig

ID: 1016255DetailsGEWERBEPARK | ERSTBEZUG | TOP-LAGE

ID: 996681DetailsBremen, ca. 1.300 m² Lager-/ Logistikfläche zu vermieten

ID: 1032273DetailsMünchen - Nord, Hallen- und Freiflächen in Bestlage zu vermieten

ID: 101077DetailsPROVISIONSFREI | GEWERBEPARK | FLEXIBEL

ID: 1000973DetailsArnsdorf | ca. 9.000 m² | Lager & Logistik | Betonrampe & ebenerdig | teilbar ab 2.000

ID: 1009874DetailsRepräsentativer Gewerbepark

ID: 1005086Detailsca. 1.350 m² große, ebenerdige Hallenfläche mit Büro

ID: 1035432DetailsPRODUKTION | LAGER | RAMPE

ID: 991522DetailsGarching, Neubau von ca. 8.000 m² Lager-,Forschungs- und Bürofläche

ID: 1030576DetailsMunich-North, warehouse and office spaces for rent

ID: 1033335DetailsMunich-North, warehouse and office spaces for rent

ID: 1024609DetailsMunich-North, warehouse and office spaces for rent

ID: 1034331DetailsMunich-North, warehouse and office spaces for rent

ID: 1002692DetailsMunich-North, warehouse and office spaces for rent

ID: 1034768DetailsMunich-North, warehouse and office spaces for rent

ID: 1034670DetailsMunich-North, warehouse and office spaces for rent

ID: 1034767DetailsMunich-North, warehouse and office spaces for rent

ID: 1025539DetailsMunich-North, warehouse and office spaces for rent

ID: 1010949DetailsMunich-North, warehouse and office spaces for rent

ID: 1032598DetailsAugsburg, site with about 2.500 sqm for rent

ID: 9040DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031912DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031769DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031836DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1028145DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030724DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030615DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1023871DetailsGladback, warehousing space for wholesale or retail for rent

ID: 95769DetailsGladback, warehousing space for wholesale or retail for rent

ID: 1013489DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1025426DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1026621DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1022435DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1023380DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1014315DetailsNeuss, approx. 1,295 sqm warehouse space in a business park for rent

ID: 997156DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1017665DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1019585Details

Do you have a question? Leave your contact details here and we will call you back!

Press Release

Hamburg region: Realogis analyses the market for logistics and industrial property market in 2023

- 38.8%: Take-up sees dramatic slump

- User companies reluctant to invest due to uncertainty

- Hardly any ESG-compliant products available

- Similar result expected in 2024

- Existing properties dominate the market

- Big-box properties experience high bloodletting - business parks attract large influx

- Few transactions by owner-occupiers

- Regional ranking: Hamburg South remains in top place

- Logistics/distribution again tops industry rankings

- Large spaces down 68%

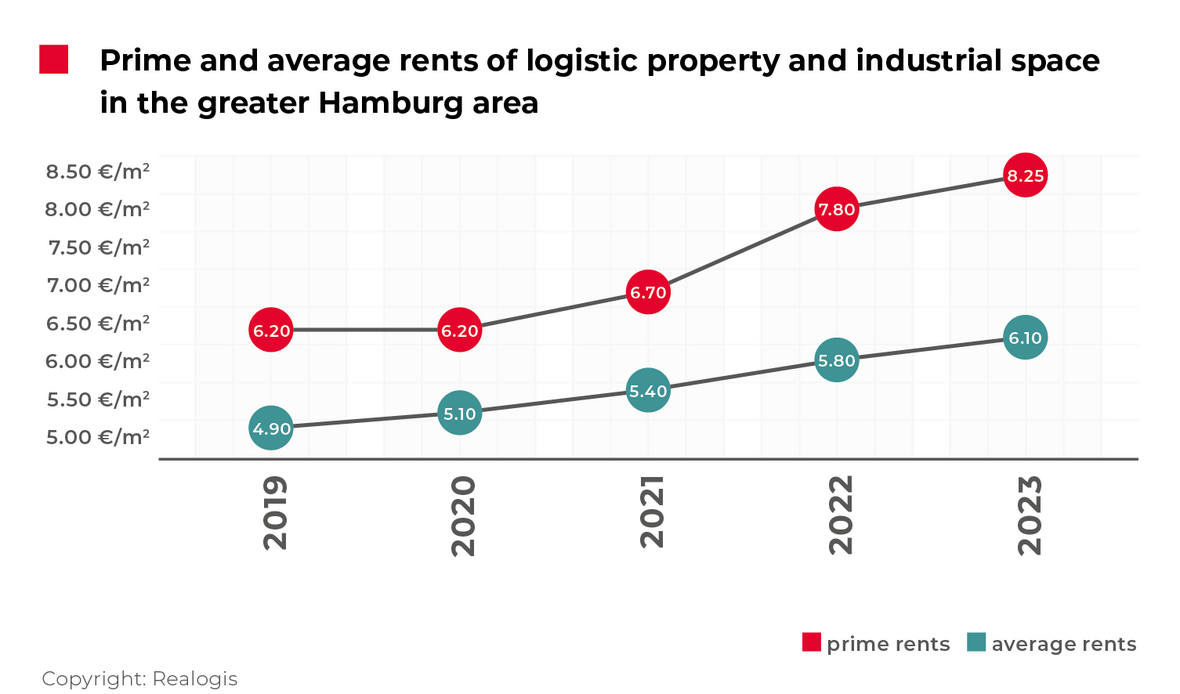

- Prime rent climbs to €8.25/m² for the first time

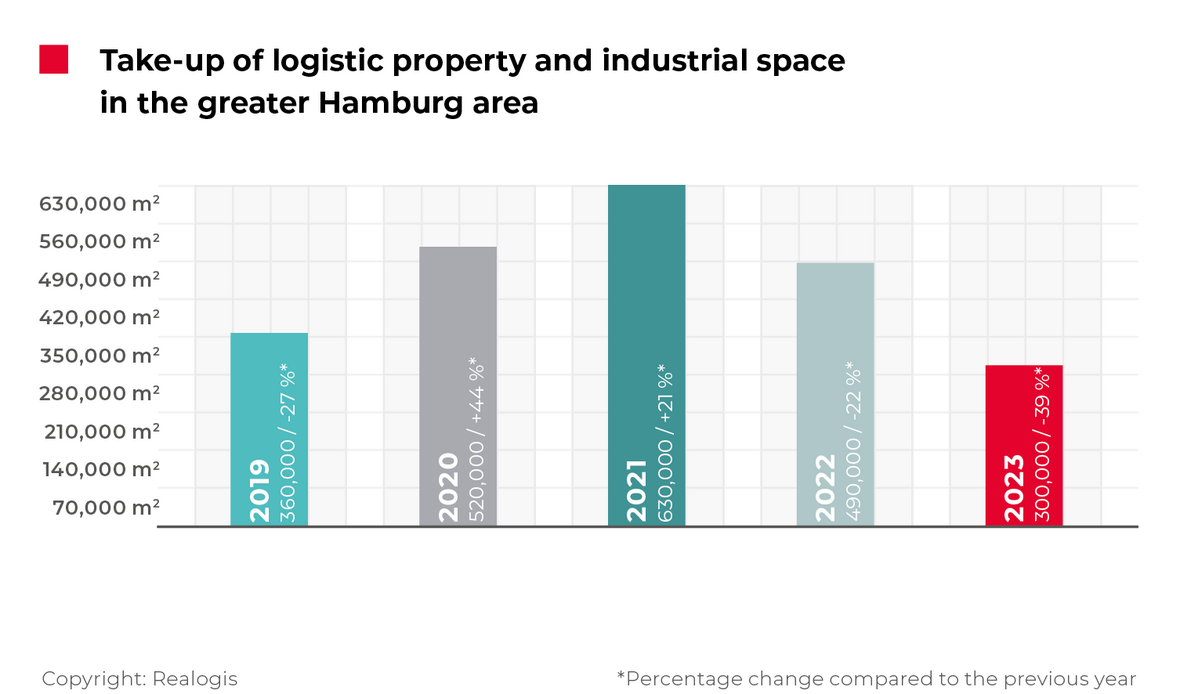

It is a clear continuation of the negative trend from 2022, which saw a drop of 22.2% or 140,000 m² to 490,000 m² of total take-up following a record year in 2021, in which take-up was 630,000 m². Over the past two years as a whole, the market has fallen by a total of 330,000 m² in newly let space. According to the Realogis analysis, the continued negative trend also meant that the five-year average take-up of 460,000 m² was missed by a significant 35%.

"The massive decline in space in Hamburg's market for owner-occupied and rented warehouse, logistics and industrial space is primarily due to an uncertain economic environment and geopolitical tensions. User companies are being cautious with their investments, securing existing space and taking a wait-and-see approach," reports Jörg Lojewski, Managing Director of Realogis Immobilien Hamburg GmbH.

"In addition, there are hardly any ESG-compliant products available to companies in the large-volume sector with plans for changes or to expand – either in existing properties or in the near future as part of newbuilds. These spaces have been absorbed by the market in recent months," warns Jörg Lojewski.

In view of the continuing high construction and financing costs, there are currently almost no new large-volume, speculative project developments. "Furthermore, there are virtually no properties available for this purpose in the Hamburg market area. Project developers are of necessity holding back on speculative newbuilds," says Stefan Imken, Managing Director of Realogis Immobilien Hamburg GmbH, outlining the situation on the market at the start of 2024.

"Inflation is expected to continue to fall. The central banks are therefore expected to start cutting interest rates from the middle of 2024 onwards. This will increase companies' willingness to invest," says Jörg Lojewski optimistically.

Geopolitical uncertainties and a shortage of available space remain, however. Realogis Hamburg therefore expects take-up by the end of 2024 to stay at a similar level to 2023, i.e. 300,000 m² up to a maximum of 350,000 m².

Biggest deals

Company | Region | Take-up | Type | Sector |

TST GmbH | HH South | 21,300 m² | New build | Logistics |

Nagel Group | HH East | 15,000 m² | New build | Logistics |

Pandora Group | HH East | 15,000 m² | New build | Manufacturing |

MediaMarktSaturn | HH South | 14,600 m² | Existing property | Retail |

IGEPA Group | HH East | 13,500 m² | Existing property | Retail |

Existing properties dominate the market

Lettings in existing properties were the main drivers behind the majority of the take-up in Hamburg's owner-occupier and rental market, accounting for around 70% or 208,500 m². The agreements concluded by the electronics retail chain MediaMarktSaturn for 14,600 m² and the specialist wholesaler IGEPA Group for 13,500 m² contributed a total of around 25,000 m² or 12% of the take-up of existing properties.

Newbuilds accounted for 91,500 m² of take-up, with three of the five top deals contributing a total of 51,300 m² or 56% of newbuild take-up. These include the logistics company TST GmbH with 21,300 m² as well as the jewellery company Pandora Group and the logistics company Nagel Group, each with 15,000 m².

Realogis has not registered any land use in former brownfield sites.

Big-box properties experience high bloodletting - business parks attract large influx

While big-box properties still clocked 76% or 372,400 m² in the previous year of 2022 as a whole, they currently account for only 98,500 m² or 32.8%, a drop of 273,900 m² or 74%.

In contrast, the use of business parks saw high growth in 2023. Take-up in this building class almost doubled to 67.2% or 201,500 m² in 2023, up from 102,900 m² or 21% in 2023.

Properties that were neither located in business parks nor belong to big boxes currently have no significant market share, coming in at 3% with 14,700 m².

Few transactions by owner-occupiers

The Hamburg market remained a predominantly letting market in 2023. Take-up of 259,000 m² or 86.3% was recorded in the books, down from 328,300 m² or 67% in 2022.

Owner-occupiers accounted for 41,000 m² or 13.7% in 2023. They played a much greater role in 2022, contributing almost one in three square metres of take-up at 147,000 m² or 67%.

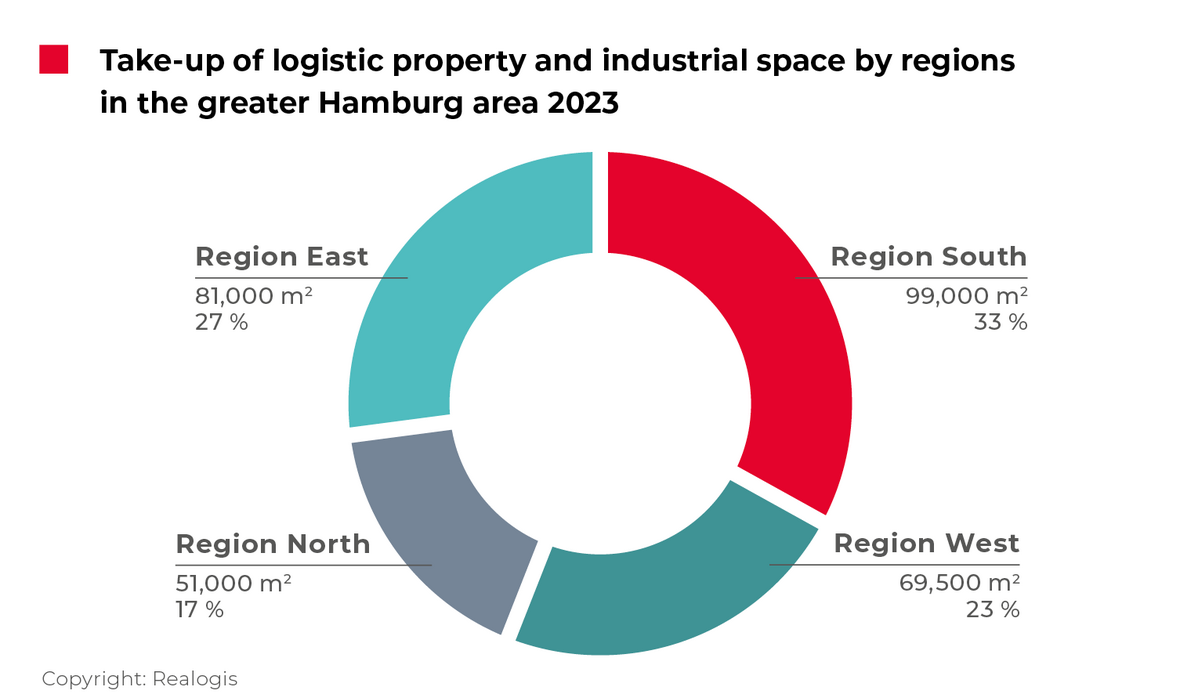

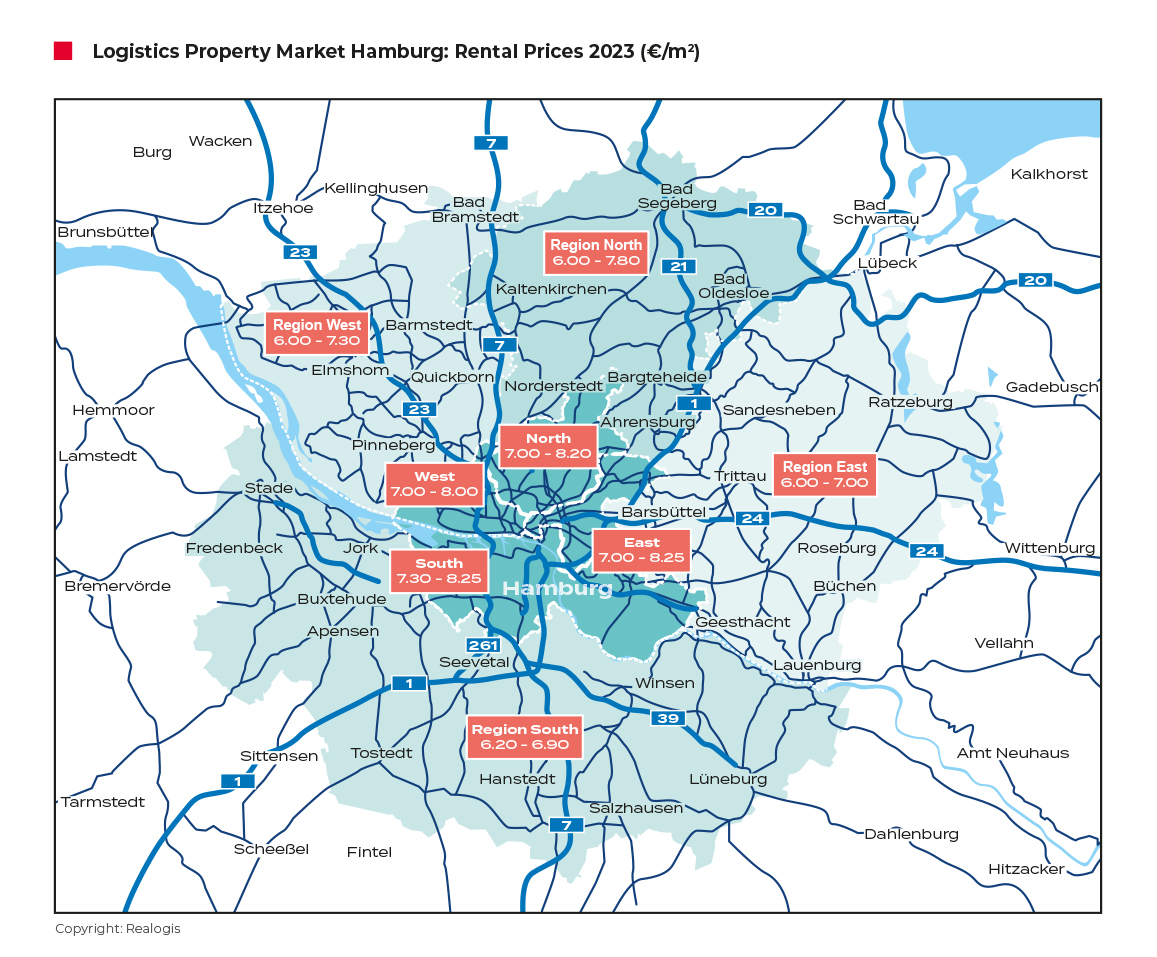

Regional ranking: Hamburg South remains in first place – but declines 61.9%

The most sought-after region in 2023 was still the south of Hamburg with 99,000 m² or 33%, albeit to a less significant degree than in the same period of the previous year when it accounted for 259,700 m² or 53%. Of all the submarkets, the south of Hamburg suffered the sharpest fall in absolute terms with a drop of 160,700 m² or 61.9%. As a result, it lost the most significant share of the market, down 20 percentage points. The extremely below-average year for this submarket as a whole is also emphasised by it falling short of the five-year average take-up of 200,000 m² by a massive 50%. Two of the top contracts were signed in the south of Hamburg: TST GmbH's deal for 21,300 m² and MediaMarktSaturn deal for 13,500 m² contributed a total of 36.3% of take-up.

Hamburg East once again took second place with 81,000 m² or 27%, losing the second-most take-up after the South in top spot, having started out at 151,900 m² or 31%. The delta is 70,900 m² or 46.7%, meaning that take-up has almost halved. In relative terms, however, the submarket lost only slightly in importance, falling by four percentage points. Three of the five top deals were signed in Hamburg East and contributed a total of 43,500 m² or 53.7% (Nagel Group with 15,000 m², Pandora Group with 15,000 m² and IGEPA Group with 13,500 m²).

Previously in last place, the western submarket now sits third with 69,000 m² or 23%, up from 24,500 m² or 5%. It is the only submarket that was able to gain in importance in 2023 (+18 percentage points), and it did this with a significant increase of 44,500 m² (+182%), thus almost tripling in size. This is not only a higher figure compared to the previous year, but also exceeds the five-year average for the Hamburg West submarket of 44,500 m² by 55%.

Previously in third place, the Hamburg North market drops to last with 51,000 m² or 17% after starting out at 53,900 m² or 11%. In absolute terms, it has moved virtually sideways after recording only a slight decline of 2,900 m² or 5.4%. The submarket gained slightly in importance in relative terms (+ six percentage points), but not enough to hold its own against the Western submarket.

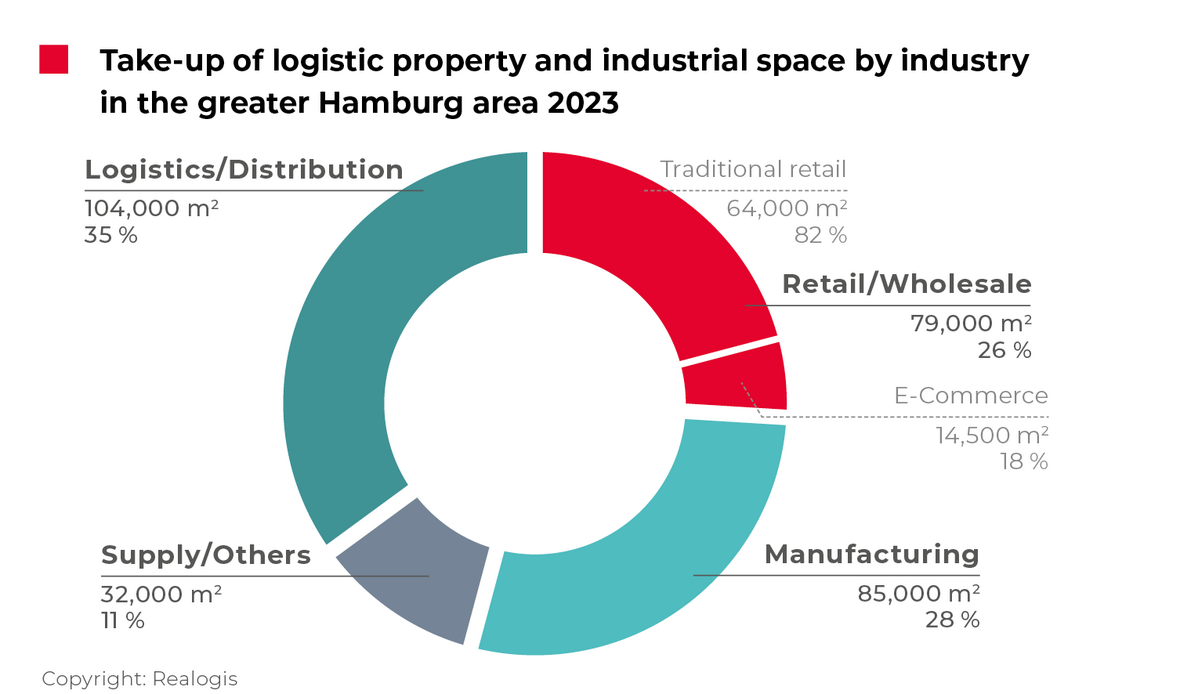

Logistics/distribution again tops industry rankings

The logistics/distribution sector leads the rankings with 104,000 m² or 34.7%, moving up from second place with 200,000 m² or 41% and taking top spot for the sixth time since 2016. In absolute terms, there was a significant year-on-year decline in take-up totalling 96,000 m² or 48%, although this was only a moderate relative decline of six percentage points. Logistics/distribution gained one place in the rankings in particular because of the significantly poorer performance produced by retail, which still held top spot in 2022 as a whole. Two top deals contributed a total of around 36,300 m² to take-up in the sector, which corresponds to around 35% (TST GmbH with 21,300 m² and Nagel Group with 15,000 m²).

It was followed by the manufacturing sector with 85,000 m² or 28.3%, up from third place with 55,000 m² or 11% in 2022. This represents the most sizeable absolute growth of 30,000 m² of all subsectors (+54.5%) and, at +17 percentage points, the most significant relative growth of all subsectors. Manufacturing was also the only subsector to perform above its five-year average in the past year (+17 % or 72,740 m²). The top deal, concluded by Pandora Group, contributed over 15,000 m² (17.6% of the sector's take-up in this category).

Currently accounting for just 79,000 m² or 26.3%, the previous leader, the retail sector, drops to third. Starting out at 220,500 m² or 45% in 2022, it lost the majority of take-up in a year-on-year comparison with a delta of 141,500 m² or 64.2%. This means that last year retail recorded around only a third of the previous year's take-up. A drop of 19 percentage points constitutes the largest slump in importance in relative terms, while the long-term five-year average of 144,240 m² has now been undershot by 45.2%.

Within the retail sector, traditional retail made the largest contribution with 64,500 m² or 81.6%, down from 147,000 m² or 67%. E-commerce currently accounts for 14,500 m² or 18.4% (2022: 73,500 m² or 33 %). The transactions concluded by MediaMarktSaturn for 14,600 m² and by the IGEPA Group for 13,500 m² contributed 36% to the take-up of retail space.

The miscellaneous category "Other" remains in last place with 32,000 m² or 10.7% (2022: 14,500 m² or 3%), which represents an increase of +17,500 m², more than double the previous year's figure and an increase of eight percentage points.

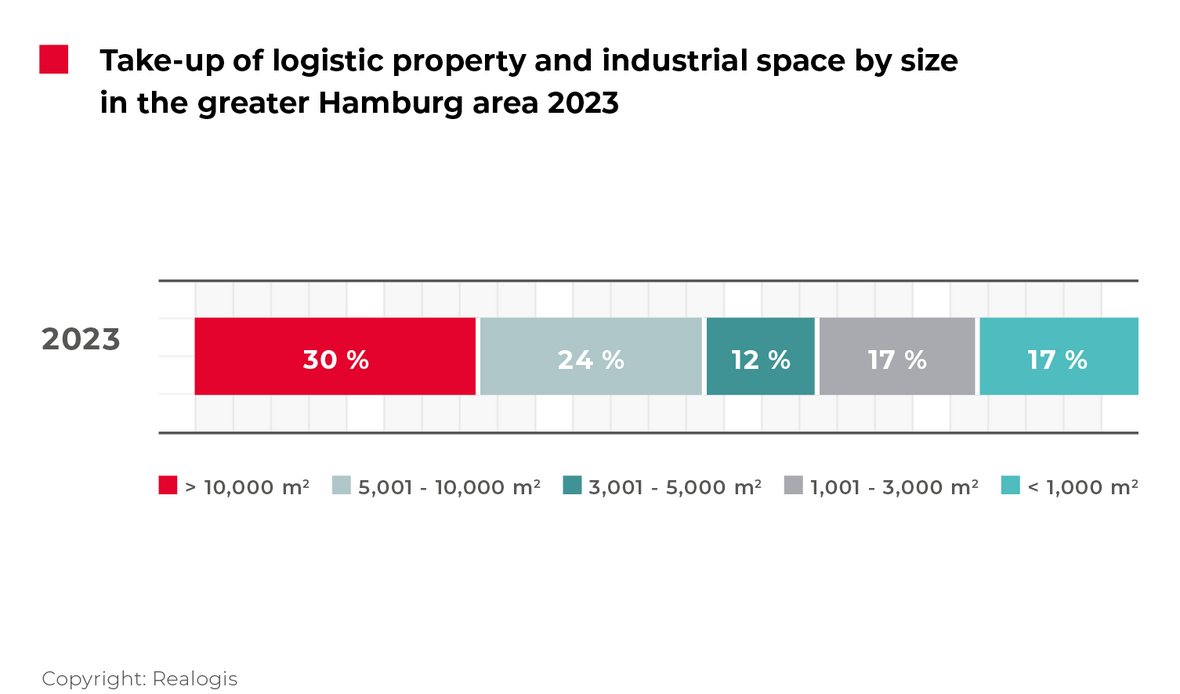

Large spaces down 68%

In 2023, as in the same period the previous year, large spaces of 10,001 m² or more accounted for the highest share of take-up at 30.3% or 90,800 m², but this is down significantly from 333,200 m² or 68%. In absolute terms, the decline in take-up is a very sizeable 242,400 m² or 72.7%, which means take-up was able to put together around only a quarter of the figures for the previous year, 2022. It also means that the relative importance of large spaces also plummeted by 37.7 percentage points. While these spaces accounted for around 7 out of 10 square metres taken up in the same period in 2022, this figure will be around only 3 out of 10 in 2023 as a whole.

97% of the decline in take-up is attributable to large spaces over 10,000 m² (totalling -250,700 m²) and could not be compensated for by the growth in the other size categories (+60,700 m²).

The segment comprising larger spaces between 5,001 and 10,000 m² climbed two ranks with 71,500 m² or 23.8%, up from 34,300 m² or 7%, and ended in second place. Of all the size categories, it can claim the most significant absolute growth of 37,200 m² or 108% (more than doubling) and also the highest relative increase in importance of +16.8 percentage points.

The size category made up of medium-sized properties from 3,001 to 5,000 m² is still in last place with 36,200 m² or 12.1%, up from 24,500 m² or 5%. This size category increased by 11,700 m² (+47.8%) in absolute terms and by seven percentage points in relative terms.

Medium to smaller spaces of between 1,000 and 3,000 m² combine to account for the third most space with 51,000 m², remaining in third place but up from 39,200 m² or 8%. It can this point to an increase of 11,800 m² or 30.1% in absolute terms and nine percentage points in relative terms.

Very small spaces of less than 1,000 m² have dropped two ranks and account for 50,500 m² or 16.8% of take-up, leaving this category in fourth place. In absolute terms, it is the only size category apart from large spaces of 10,001 m² or more to lose space compared to the previous year (-8,300 m², -14.1%), although it was able to make moderate gains in relative terms (+4.8 percentage points).

Prime rent climbs to €8.25/m² for the first time

Prime rents reached a new provisional high of €8.25/m², up 5.8% from €7.80/m² in 2022. The five-year average of €7.03/m² was exceeded by a significant 17.4%.

Average rents also rose by 5.2% to €6.10/m² in 2023, reaching a new provisional high. Average rent is currently 11.7% above the five-year average of EUR 5.46/m².

"Prime and average rents are rising due to low vacancy rates and demand exceeding supply for high-quality space in existing and new buildings," notes Stefan Imken.

REALOGIS media contact:

Silke Westermann

Senior public relations specialist

Tel: +49/211/53 88 3-440

e-mail: s.westermann@shcommunication.de

REALOGIS company contact:

REALOGIS Holding GmbH

Silja Schuppler

Marketing

Rundfunkplatz 4, 80335 Munich

Tel: +49/89/51 55 69 17

e-mail: s.schuppler@realogis.de

www.realogis.de

REALOGIS. No. 1 for industrial and logistics properties

The REALOGIS Group is Germany’s leading player for the consulting and brokering of industrial, logistics and commercial properties. Founded in 2005 as a pioneer for the asset class of logistics and industry, the owner-operated group has enjoyed healthy growth, is crisis-resistant and knows the German market like no other. In 2022 Realogis generated nearly 1.25 million m² of usable space alone in the letting segment (preliminary result). The net commission revenue of all services in the financial year 2022 are EUR 22.74 million (preliminary result).

In 2021, REALOGIS also won the German Real Estate Prize in the “Commercial Player” category, which honours companies for their outstanding commitment, creativity, innovative strength and sustainability.

Realogis is represented in the country’s seven top logistics locations of Berlin, Düsseldorf, Frankfurt am Main, Hamburg, Leipzig, Munich and Stuttgart, while a dedicated organisational unit ensures transparency in around 15 additional regional logistics markets. 70 real estate professionals advise national and international companies from the fields of logistics, e-commerce, retail and industry as well as private and institutional investors. Quick, flexible, regional, customer-oriented and with a high volume of transactions.

REALOGIS four core competencies are arranging highly creditworthy tenants for new and existing properties, assisting investors with property investments and project development of greenfields and brownfields, outstanding service for locating or selling sites, and the development and implementation of holistic property strategies.

In short, REALOGIS creates more room for its customers’ success in every sense. Further information: https://www.realogis.de/