HOCHWERTIG | 650 m² HALLE | 800 m² AUSSTELLUNG

ID: 998947DetailsGarching, repräsentatives Produktionsgebäude mit hochwertigen Büroflächen

ID: 93135Detailsca. 400 m² große, ebenerdige Lager-Produktionshalle mit Meisterbüro in Top Lage

ID: 1036679DetailsDirekt am Autobahnkreuz Ulm/Elchingen - Neubau multifunktionaler Logistik- und Produktionsflächen

ID: 994300DetailsLOGISTIK | RAMPEN | FREIFLÄCHE

ID: 1008605DetailsLager-/Logistik | Neubau | Rampen | teilbar | ebenerdig

ID: 1016255DetailsGEWERBEPARK | ERSTBEZUG | TOP-LAGE

ID: 996681DetailsBremen, ca. 1.300 m² Lager-/ Logistikfläche zu vermieten

ID: 1032273DetailsMünchen - Nord, Hallen- und Freiflächen in Bestlage zu vermieten

ID: 101077DetailsPROVISIONSFREI | GEWERBEPARK | FLEXIBEL

ID: 1000973DetailsArnsdorf | ca. 9.000 m² | Lager & Logistik | Betonrampe & ebenerdig | teilbar ab 2.000

ID: 1009874DetailsRepräsentativer Gewerbepark

ID: 1005086Detailsca. 1.350 m² große, ebenerdige Hallenfläche mit Büro

ID: 1035432DetailsPRODUKTION | LAGER | RAMPE

ID: 991522DetailsGarching, Neubau von ca. 8.000 m² Lager-,Forschungs- und Bürofläche

ID: 1030576DetailsMunich-North, warehouse and office spaces for rent

ID: 1033335DetailsMunich-North, warehouse and office spaces for rent

ID: 1024609DetailsMunich-North, warehouse and office spaces for rent

ID: 1034331DetailsMunich-North, warehouse and office spaces for rent

ID: 1002692DetailsMunich-North, warehouse and office spaces for rent

ID: 1034768DetailsMunich-North, warehouse and office spaces for rent

ID: 1034670DetailsMunich-North, warehouse and office spaces for rent

ID: 1034767DetailsMunich-North, warehouse and office spaces for rent

ID: 1025539DetailsMunich-North, warehouse and office spaces for rent

ID: 1010949DetailsMunich-North, warehouse and office spaces for rent

ID: 1032598DetailsAugsburg, site with about 2.500 sqm for rent

ID: 9040DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031912DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031769DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031836DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1028145DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030724DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030615DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1023871DetailsGladback, warehousing space for wholesale or retail for rent

ID: 95769DetailsGladback, warehousing space for wholesale or retail for rent

ID: 1013489DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1025426DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1026621DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1022435DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1023380DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1014315DetailsNeuss, approx. 1,295 sqm warehouse space in a business park for rent

ID: 997156DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1017665DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1019585Details

Do you have a question? Leave your contact details here and we will call you back!

Press Release

All-time high on the Berlin logistics property market

- New builds ahead of existing properties in contrast to previous year

- NEW: Analysis of take-up by owner-occupiers/ third-party users

- Highest take-up was in surrounding area east of Berlin

- NEW: Take-up analysis by big box, business park and other

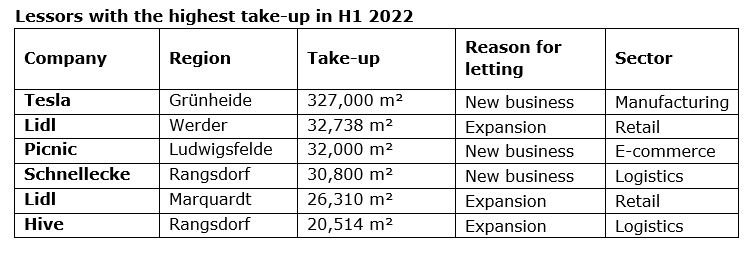

“The level of this record figure is due to the Tesla deal for 327,000 m² in Grünheide in the first quarter of 2022. But even without this deal, the first half of the year would be the strongest ever recorded at 458,300 m², which is 58.9% higher than the previous year’s figure,” reports Ben Dörks, Managing Director of Realogis Immobilien Berlin GmbH.

The annual average for the past five years is currently 335,840 m², and the development in the first six months was also exceeded by an impressive 133.8%. “The Tesla deal alone would almost be enough to reach the five-year average in Berlin,” says Ben Dörks.

New builds ahead of existing properties in contrast to previous year

Overall, leases for 655,600 m² of space for new builds were concluded from January to June this year, corresponding to a market share of 83.5%. This figure thus increased more than sixfold compared to the same period of the previous year (H1 2021: 98,900 m², 34.3% of the total market).

Existing space accounted for 129,700 m² or 16.5%, as compared to 189,500 m² or 65.7% in the same period of the previous year (a 31.6% decline in absolute terms). But even without Tesla, the previous year’s ratio of new builds to existing properties would have been inverted. “Not including the Tesla deal, new builds accounted for 71.7% of take-up and existing properties for 28.3%,” explains Ben Dörks.

NEW: Analysis of take-up by owner-occupiers/ third-party users

In its latest Berlin market report, Realogis analyses for the first time how much space is attributable to letting and how much to own use.

In the first half of the year, the ratio of third-party use/letting to the owners’ own use of industrial and logistics space was almost evenly balanced. Realogis registered a total of seven leases with owner-occupiers, together accounting for space of 393,400 m² or 50.1% of total take-up. 49.9% or 391,900 m² related to space not owned by the user. This third-party user category is much more commonly represented, with a total of 62 leases. Not including the Tesla deal, the market would have been a clear “third-party user” market at 85.5%.

NEW: Take-up analysis by big box, business park and other

Another new aspect included by Realogis is an analysis of the properties by use/building type. According to the logistics property expert, 210,300 m² or 17 of the total of 69 deals in the first half of 2022 were attributable to modern “big box” logistics, i.e. the category of large spaces of 10,000 m² or more, with logistics as the main type of use and an office share of no more than 20%.

Business parks accounted for 59,000 m² or 28 deals. Realogis defines a business park as a contiguous business district that is developed and implemented by private enterprises with a uniform concept and whose infrastructure is used jointly by the companies based there.

516,000 m² or 24 deals are attributable neither to traditional business parks nor to big box logistics. These include Tesla with 327,000 m², while the remaining 189,000 m² was mostly let in smaller stand-alone buildings, either as entire individual properties or parts of properties.

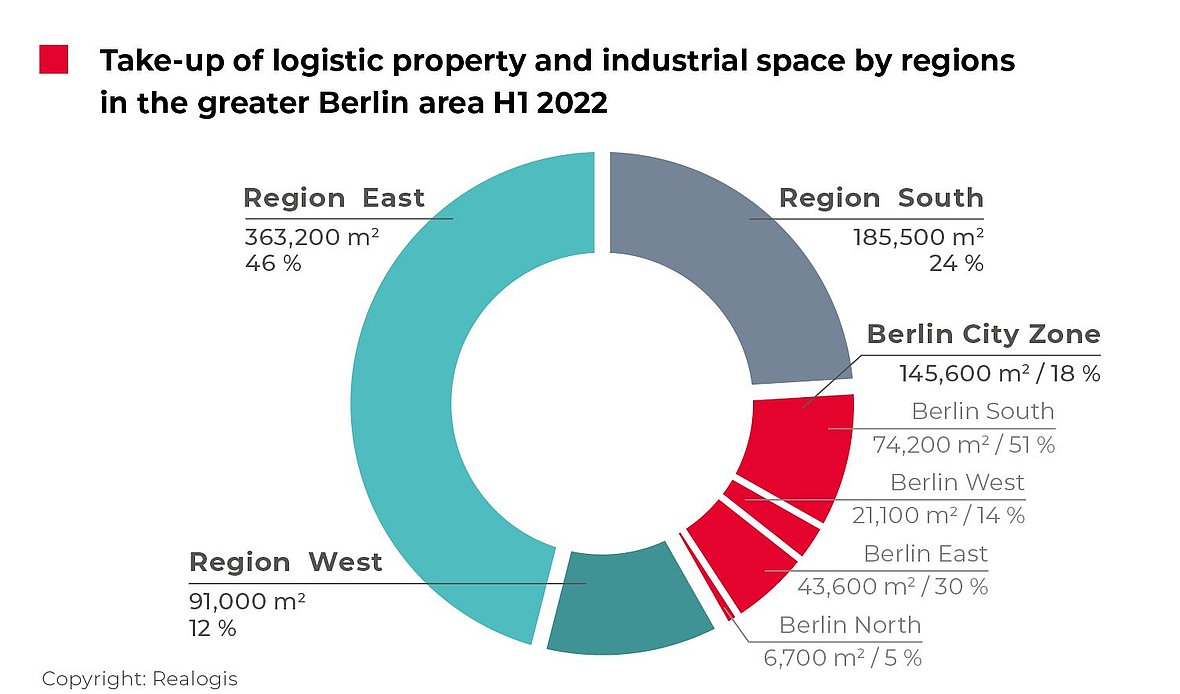

Highest take-up was in surrounding area east of Berlin

The highest take-up in H1 2022 was recorded by the surrounding area east of Berlin with a share of just under 46.2% or 363,200 m². This region posted the strongest relative increase of 32.2 percentage points compared to H1 2021 (pro rata take-up in H1 2022), primarily due to the Tesla deal in Grünheide.

In second place was the surrounding area south of Berlin with a share of 23.6% or 185,000 m² of total take-up. The surrounding area south of Berlin lost ground in terms of relative importance with a decline of 16.4 percentage points (due to the major Tesla deal), but increased its take-up by 61.9% in absolute terms.

Three of the top deals are attributable to the surrounding area south of Berlin and contribute around 44.9% of this region’s take-up with a total of 83,314 m²:

- Picnic with 32,000 m² (new business) in Ludwigsfelde

- Schnellecke with 30,800 m² (new business) in Rangsdorf

- Hive with 20,514 m² (expansion) in Rangsdorf

In third place is the city of Berlin with a share of 18.6% or 145,600 m², which thus increased by around 45,000 m² in absolute terms (around 44.3%). However, it lost the most ground out of all regions in terms of its relative share of take-up, with a year-on-year decline of 16.5 percentage points (H1 2021: share of city of Berlin of 35%; 100,900 m²). This is attributable to the strong result (due to Tesla).

Within the city of Berlin’, the inner-city area in the south dominated with 51% of take-up or 74,200 m², thus increasing by 18.9 percentage points year-on-year (H1 2021: 32.1% or 32,400 m²). Eastern Berlin accounted for 29.9% or 43,600 m² and northern Berlin for 4.6% or 6,700 m².

In fourth place out of all regions (city of Berlin and surrounding areas to the north, east, south and west) was the surrounding area to the west with a share of 11.6% or 91,000 m². At over 32,738 m² and 26,310 m², the two Lidl deals in Werder and Marquardt together account for the majority of take-up in the region with a total of 59,048 m² or 64.9% (second- and fifth-biggest deals in the first half of 2022).

There were no deals in the surrounding area to the north.

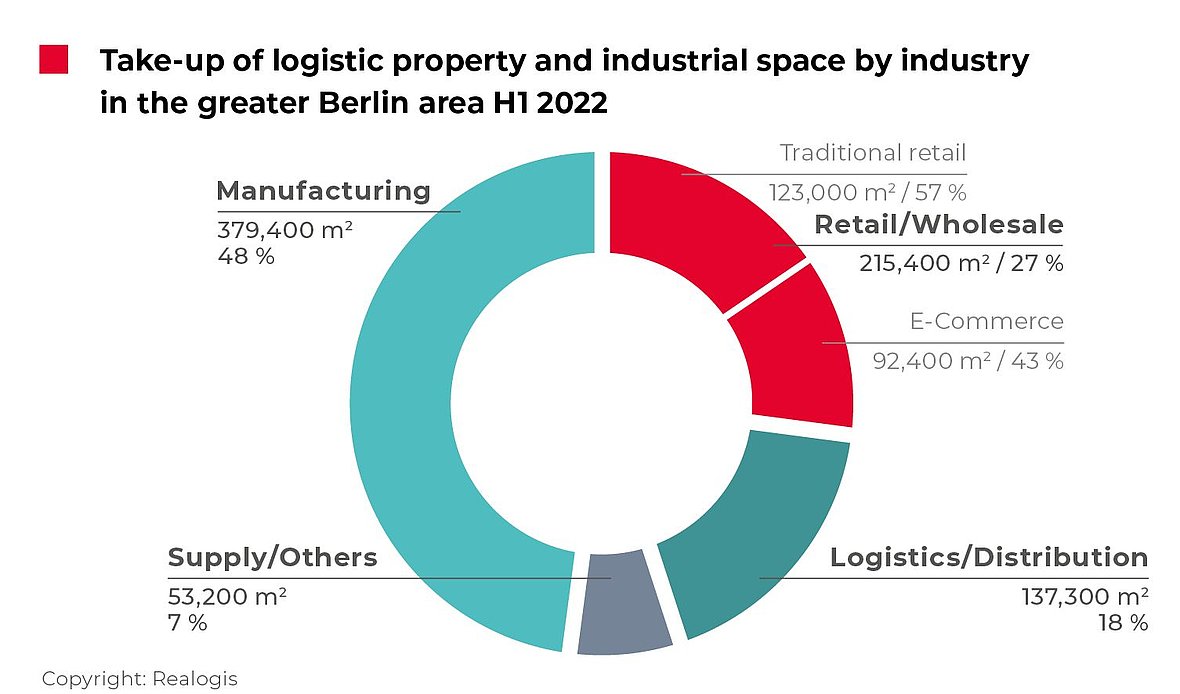

Manufacturing leads sector ranking

In the lead in terms of take-up in the first half of the year was the manufacturing sector with a share of 48.3% or 379,400 m². This was also chiefly due to the Tesla deal. After being in second place in the previous year with 89,100 m² or 30.9%, the sector more than quadrupled its absolute take-up and marked an increase of 17.4 percentage points in relative terms.

It was followed in second place by retail, which accounted for 215,400 m² or 27.4% and thus more than tripled its take-up in absolute terms and increased its relative share by 5.3 percentage points (H1 2021: 63,700 m² or 22.1%).

Three of the top deals were attributable to the retail category, together contributing 91,048 m² or around 42% of take-up. Traditional retail accounted for 123,000 m² or 57.1% of take-up. Two of the top deals – Lidl with two leases for 32,738 m² in Werder and for 26,310 m² in Marquardt – were attributable to traditional retail. With a total of 59,048 m², they accounted for around 48% of take-up in this sub-category.

In the H1 2022 reporting period, 92,400 m² of logistics space was newly let by the online retail sector in the Berlin market area. This represents 42.9% of all space taken up by retail. The top deal in the e-commerce category is Picnic with 32,000 m² or around 35%.

In third and fourth place are logistics/distribution with a share of 17.5% or 137,300 m² and the miscellaneous category “Other” with a share of 6.8% or 53,200 m².

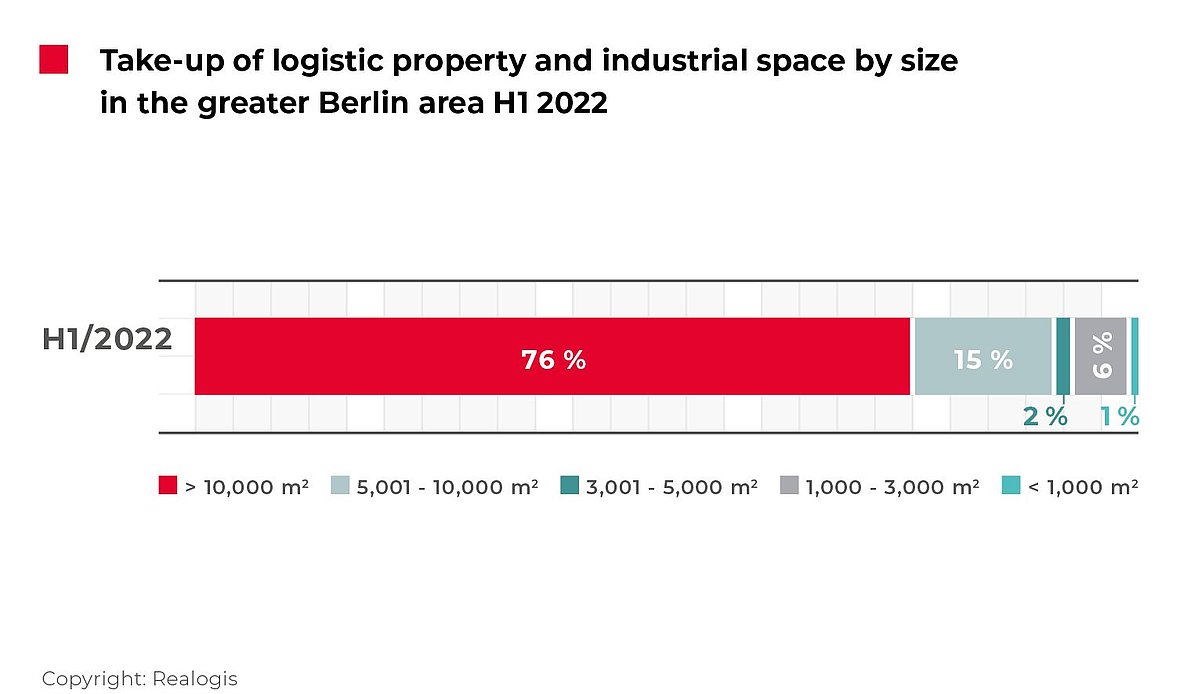

Large spaces dominate at 76.1%

Overall, Realogis registered 69 deals, 11 fewer than in the first half of 2021. The biggest share of space was accounted for by the category of areas of 10,000 m² or more at 76.1% or 597,500 m². This category had ranked second in the previous year with a share of just 29% or 81,900 m², but had the biggest increase of any size category in the first half of 2022 (up 47.1 percentage points).

There was also a strong increase in absolute terms: Compared to the same period of the previous year, more than seven times as much take-up was attributable to the largest size category in H1 2022. All of the deals with the highest take-up and particularly the Tesla deal were attributable to this segment. With a total of 469,362 m², the six biggest deals in H1 2022 contributed around 79% of take-up in the >10,000 m² category. This category had 12 of the 69 deals in the first half of the year (17%), the second-lowest figure.

Space in the 5,001 to 10,000 m² size category took second place with a share of 14.4% or 113,200 m² and 14 deals attributable to this category. Five deals – seven fewer than in the same period of the previous year – were attributable to the 3,001 to 5,000 m² size category (18,300 m² or 2.4%). The most leases were concluded in the 1,000 to 3,000 m² segment, with the 23 deals here representing 5.9% or 46,500 m². The smallest spaces of 1,000 m² or less brought up the rear with 9,800 m² or a share of 1.2%; a total of 15 deals were attributable to this segment.

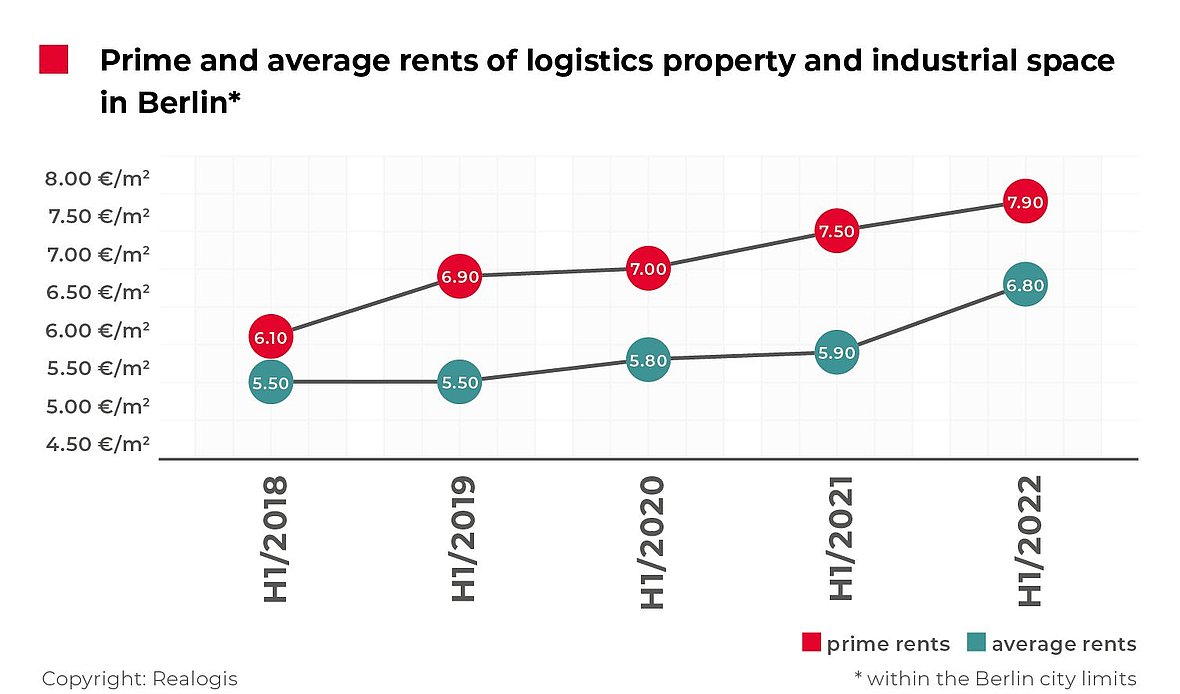

Prime rent increases to EUR 7.90

The prime rent has developed very dynamically over the past five years and reached its highest level to date at EUR 7.90/m² in the first half of 2022. It thus increased by 5.3%. By way of comparison, the highest increase in the past five years took place in H1 2018, when the prime rent rose by 19.6% from EUR 5.10/m² to EUR 6.10/m².

The current prime rent is 11.6% higher than the five-year average for the first half of the year of EUR 7.08/m².

Average rent up 15.3%

Average rent saw a similarly dynamic development, consistently becoming more expensive over the past five years with the exception of 2019 (stagnation). It most recently increased by an impressive 15.3% or almost EUR 1/m² to its highest level to date of EUR 6.80/m², after EUR 5.90/m² in H1 2021. Here, too, the highest increase was recorded in H1 2018 with growth of 22.2% from EUR 4.50/m² to EUR 5.50/m².

REALOGIS press contact:

SH/Communication – Public Relations Agency

Silke Westermann

Press

Fritz-Vomfelde-Strasse 34, 40547 Düsseldorf

Tel: +49/211/53 88 3-440

e-mail: s.westermann@shcommunication.de

REALOGIS company contact:

REALOGIS Holding GmbH

Silja Schuppler

Marketing

Rundfunkplatz 4, 80335 Munich

Tel: +49/89/51 55 69 17

e-mail: s.schuppler@realogis.de

www.realogis.de

REALOGIS. No. 1 for industrial and logistics properties

The REALOGIS Group is Germany’s leading player for the consulting and brokering of industrial, logistics and commercial properties. Founded in 2005 as a pioneer for the asset class of logistics and industry, the owner-operated group has enjoyed healthy growth, is crisis-resistant and knows the German market like no other. In 2021 Realogis generated nearly 1,3 million m² of usable space alone in the letting segment. The net commission revenue of all services in the financial year 2021 are EUR 25 million.

In 2021, REALOGIS also won the German Real Estate Prize in the “Commercial Player” category, which honours companies for their outstanding commitment, creativity, innovative strength and sustainability.

Realogis is represented in the country’s seven top logistics locations of Berlin, Düsseldorf, Frankfurt am Main, Hamburg, Leipzig, Munich and Stuttgart, while a dedicated organisational unit ensures transparency in around 15 additional regional logistics markets. 70 real estate professionals advise national and international companies from the fields of logistics, e-commerce, retail and industry as well as private and institutional investors. Quick, flexible, regional, customer-oriented and with a high volume of transactions.

REALOGIS four core competencies are arranging highly creditworthy tenants for new and existing properties, assisting investors with property investments and project development of greenfields and brownfields, outstanding service for locating or selling sites, and the development and implementation of holistic property strategies.

In short, REALOGIS creates more room for its customers’ success in every sense. Further information: https://www.realogis.de/