HOCHWERTIG | 650 m² HALLE | 800 m² AUSSTELLUNG

ID: 998947DetailsGarching, repräsentatives Produktionsgebäude mit hochwertigen Büroflächen

ID: 93135Detailsca. 400 m² große, ebenerdige Lager-Produktionshalle mit Meisterbüro in Top Lage

ID: 1036679DetailsDirekt am Autobahnkreuz Ulm/Elchingen - Neubau multifunktionaler Logistik- und Produktionsflächen

ID: 994300DetailsLOGISTIK | RAMPEN | FREIFLÄCHE

ID: 1008605DetailsLager-/Logistik | Neubau | Rampen | teilbar | ebenerdig

ID: 1016255DetailsGEWERBEPARK | ERSTBEZUG | TOP-LAGE

ID: 996681DetailsBremen, ca. 1.300 m² Lager-/ Logistikfläche zu vermieten

ID: 1032273DetailsMünchen - Nord, Hallen- und Freiflächen in Bestlage zu vermieten

ID: 101077DetailsPROVISIONSFREI | GEWERBEPARK | FLEXIBEL

ID: 1000973DetailsArnsdorf | ca. 9.000 m² | Lager & Logistik | Betonrampe & ebenerdig | teilbar ab 2.000

ID: 1009874DetailsRepräsentativer Gewerbepark

ID: 1005086Detailsca. 1.350 m² große, ebenerdige Hallenfläche mit Büro

ID: 1035432DetailsPRODUKTION | LAGER | RAMPE

ID: 991522DetailsGarching, Neubau von ca. 8.000 m² Lager-,Forschungs- und Bürofläche

ID: 1030576DetailsMunich-North, warehouse and office spaces for rent

ID: 1033335DetailsMunich-North, warehouse and office spaces for rent

ID: 1024609DetailsMunich-North, warehouse and office spaces for rent

ID: 1034331DetailsMunich-North, warehouse and office spaces for rent

ID: 1002692DetailsMunich-North, warehouse and office spaces for rent

ID: 1034768DetailsMunich-North, warehouse and office spaces for rent

ID: 1034670DetailsMunich-North, warehouse and office spaces for rent

ID: 1034767DetailsMunich-North, warehouse and office spaces for rent

ID: 1025539DetailsMunich-North, warehouse and office spaces for rent

ID: 1010949DetailsMunich-North, warehouse and office spaces for rent

ID: 1032598DetailsAugsburg, site with about 2.500 sqm for rent

ID: 9040DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031912DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031769DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031836DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1028145DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030724DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030615DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1023871DetailsGladback, warehousing space for wholesale or retail for rent

ID: 95769DetailsGladback, warehousing space for wholesale or retail for rent

ID: 1013489DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1025426DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1026621DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1022435DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1023380DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1014315DetailsNeuss, approx. 1,295 sqm warehouse space in a business park for rent

ID: 997156DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1017665DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1019585Details

Do you have a question? Leave your contact details here and we will call you back!

Market report Munich full year 2022

- About the logistics market in the economic region

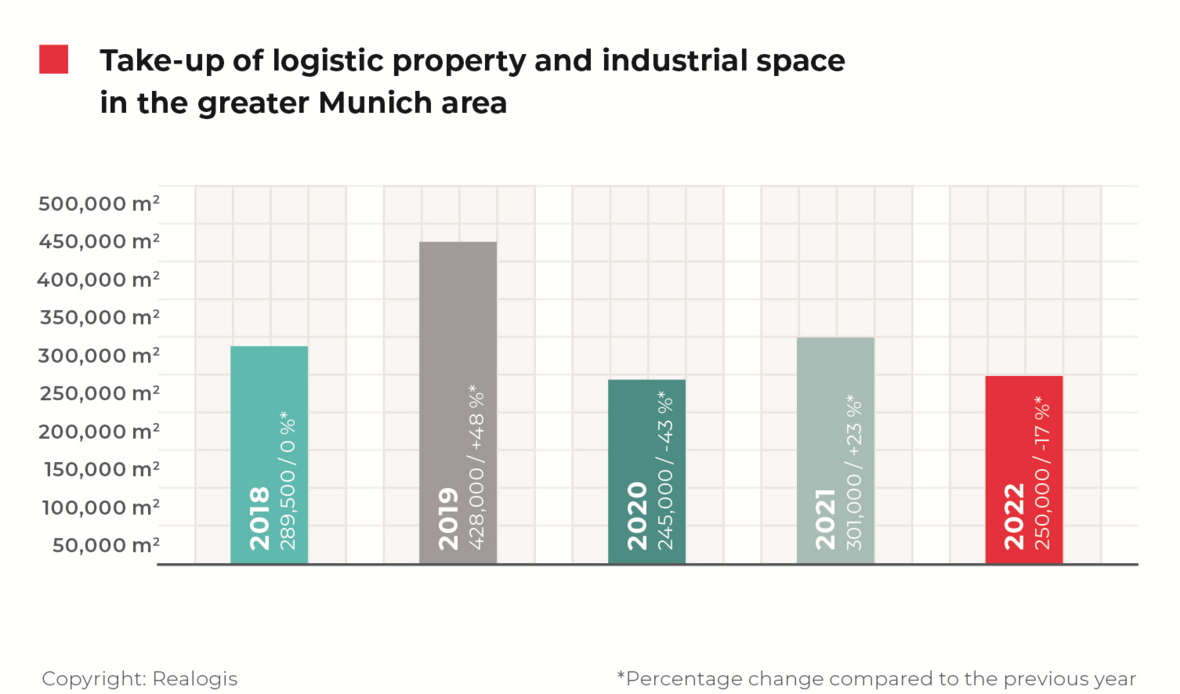

Munich logistics market impacted by decline in letting space

The Munich market’s strong result for warehouse, logistics and industrial space for rent of 301,000 m² in 2021 was followed by a significant decline. With take-up of 250,000 m² generated by all market participants in 2022 as a whole, the drop-off amounted to 16.9%. According to our analysis, the take-up achieved from January to December 2022 represents the second-worst result of the last five years.

Only 2020 was slightly worse at 245,000 m². The 2022 result is also 17.4% below the five-year average of 302,700 m². However, this includes the year with the highest take-up ever recorded: 2019 bumped up the average with its result of 428,000 m² thanks to the major deal with Krauss Maffei (210,000 m² in Parsdorf). Even discounting this outlier, the latest result is lower than the average of 271,375 m² by around 8% – still significant, but less extreme.

Facts

- Take-up of 250,000 m² represents decline of 16.9%

- Almost 85% of all lettings occurred in existing properties

- Potential for brownfield developments

- 18% fewer leases concluded

- Business parks and other properties playing an ever-greater role

- Average lease term at 6.3 years

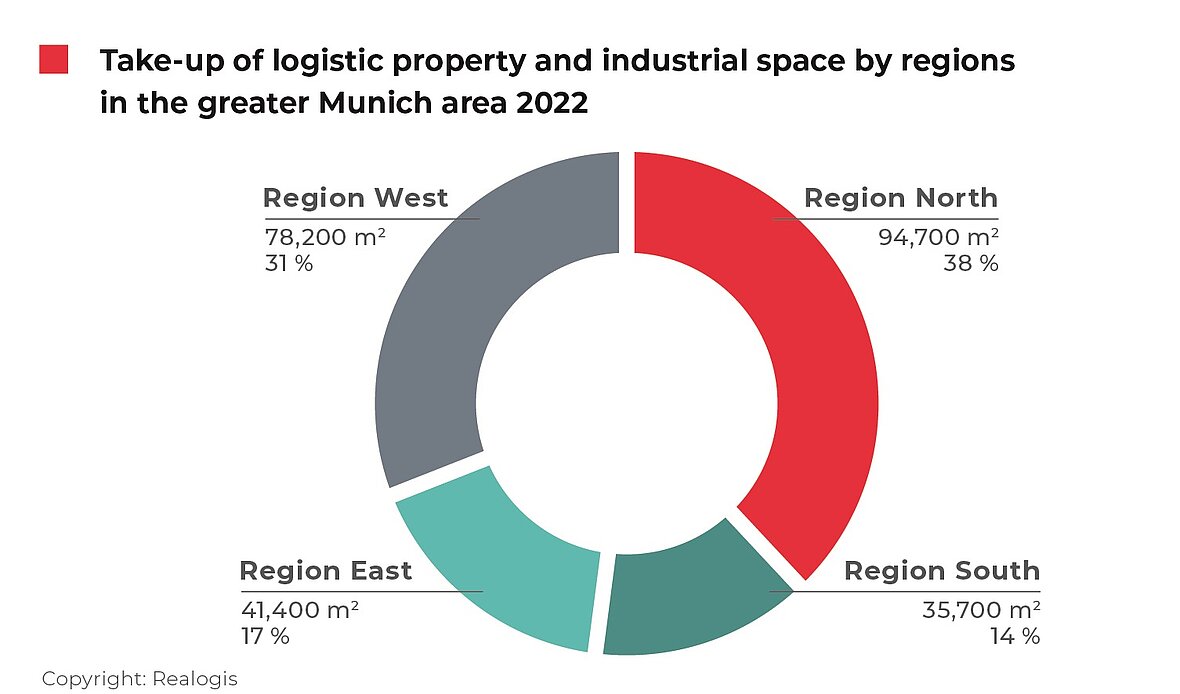

- Munich North still ‘number one’ in terms of take-up

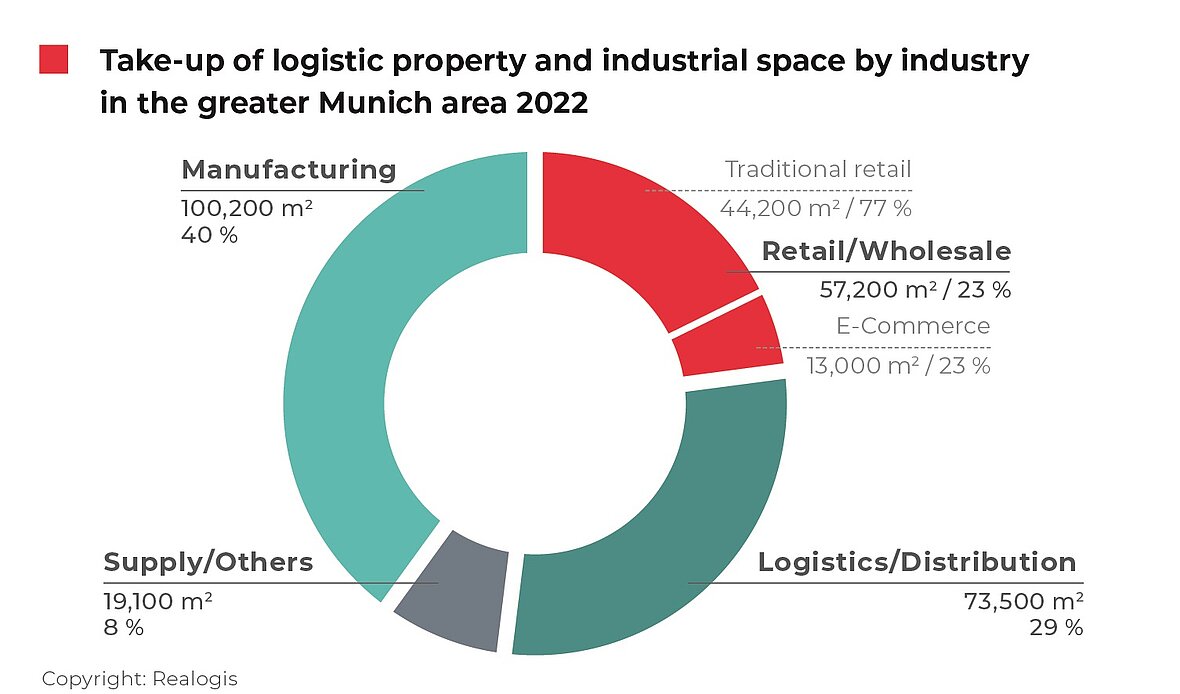

- Manufacturing overtakes logistics to top sector ranking

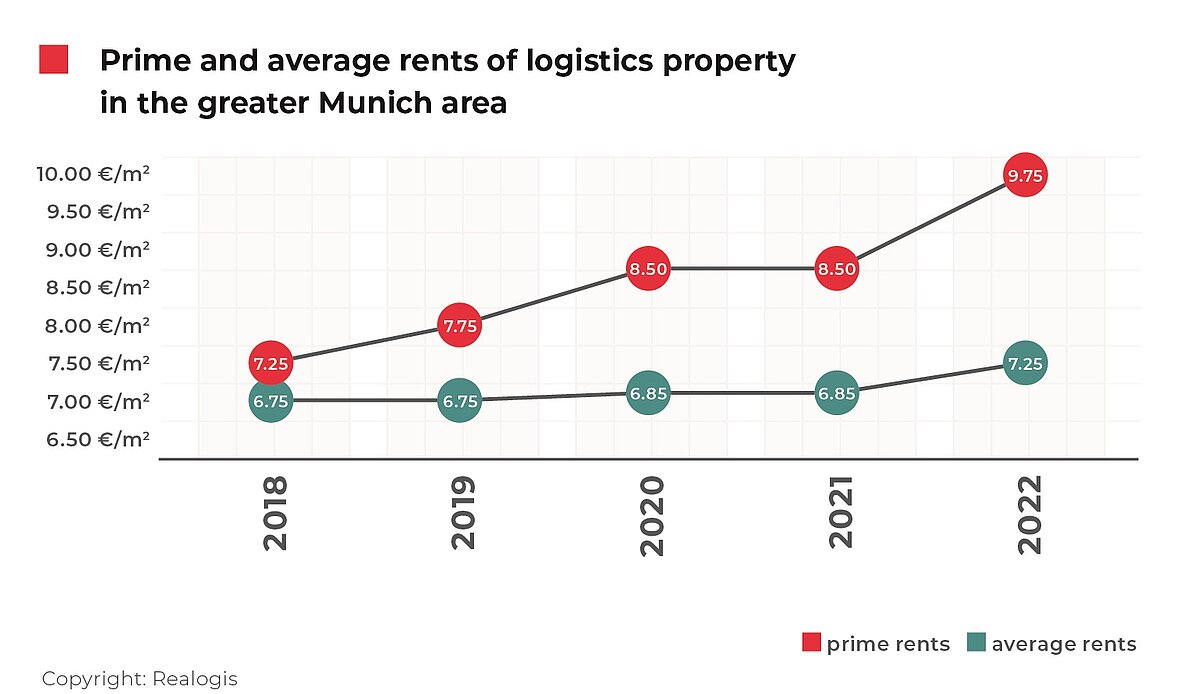

- Prime rent rises by a considerable 14.7% to new high of EUR 9.75/m²

Lessors with highest take-up in full-year 2022

The six largest deals involving warehouse, logistics and industrial properties in the Munich market together accounted for 83,700 m², or a third of total take-up:

Major Deals

Winning BLW, Penzberg (Munich south), approx. 28,000 m² (existing property), manufacturing

DHL, Germering (Munich west), approx. 14,000 m² (new build), logistics

Proton Motor Fuel Cell GmbH, Fürstenfeldbruck (Munich west), approx. 13,200 m² (existing property), manufacturing

Mynaric, Triebwerk (Munich west), approx. 11,000 m² (existing property), manufacturing

FS.COM, Kirchheim (Munich east), approx. 8,800 m² (existing property), e-commerce

Rhenus Archive Services, Karlsfeld (Munich north), approx. 8,700 m², existing property, logistics

Almost 85% of all lettings occurred in existing properties

Most of the result for 2022 contributed by existing propertieswith 211,200 m², or 84.5%, followed by new buildings with 38,800 m², or 15.5%. This is a continuation of the trend of the previous years from 2018 to 2021 – with the exception of 2019.

According to our assessment, this trend will also continue in 2023. There will be no new buildings within 30 kilometres. Due to a lack of opportunities, tenants will increasingly remain in their existing properties and renew their leases. In the reporting period, leases for over 50,000 m² were already renewed in Munich North at rents of more than EUR 10/m² (we do not include renews in our analysis).

Business parks and other properties playing an ever-greater role

With regard to the division of rented properties into big boxes and business parks, the biggest share was attributable to the business parks category at 93,800 m², or 37.5%. We define a business park as a contiguous business district that is developed and implemented with a uniform concept and whose infrastructure is used jointly by the companies based there.

There were no new lettings in big-boxproperties – i.e. properties upwards of 10,000 m² mainly used for logistics and with an office share of no more than 20%. This shows that not enough space is being provided for large, modern properties – such as those needed by retailers of fast-moving consumer goods and by the manufacturing industry – in the Greater Munich area. And this is despite high demand and a large number of requests.

Potential for brownfield developments

We think, that there will be more brownfield developments in the Munich region in the next five to ten years. There is potential for several hundred thousand square metres – but they are either still active manufacturing sites, old logistics/warehouse spaces with ongoing tenancy agreements, or opportunities for the conversion of existing properties.

Other space not allocated to either of these categories accounted for 156,200 m², or 62.5% of the total letting volume in 2022.

Letting market dominated by third-party users

At 236,000 m² or 94.4%, the vast majority of space was rented by third-party users. Just a single deal contributed 5.6%, or 14,000 m², to the result for owner-occupiers, i.e. companies that use properties that they also own. This deal by DHL for 14,000 m² in Germering (Munich West) was the second-largest in the reporting period.

18% fewer leases concluded overall

In 2022 as a whole, we registered 90 concluded leases – 20 deals, or 18%, fewer than in the previous year (FY 2021: 110).

The average lease term was 6.3 years. A little more than a quarter – i.e. 25 deals, or 28% – was attributable to short-term leases of one to four years. 39%, or 35 deals, related to medium- or longer-term leases of five to nine years, while long-term leases of ten years or more accounted for around a third of the deals, or 30 leases.

Munich North still ‘number one’ in terms of take-up

As in previous years (except for 2019), Munich North tops the region ranking in terms of take-up. At 94,700 m², or 37.9%, the region saw a slight decline in its relative share of 3.7 percentage points, compared with 41.6%, or 125,200 m², in 2021. However, this is an absolute decline of 24 %.

Despite its leading position, Munich North was home to only one of the top deals, namely that of Rhenus Archive Services for 8,700 m² (9.2% of the take-up). Instead, the result was decided by a large number of small to medium-sized deals, of which there were 42 in total.

This might also be interesting for you:

To the market report Germany

The West, which was in third place last year, takes second place with 78,200 m², a share of 31.3%. This geographical sub-market was the only one that saw absolute growth (by 23% from 63,800 m² in 2021 to 78,200 m²) and most clearly increased its relative share by 10.1 percentage points.

Three of the six deals were made in Munich West: DHL (14,000 m²), Proton Motor Fuel Cell GmbH (13,200 m²) and Mynaric (11,000 m²) together account for 38,200 m². They thus provided half of the take-up in the West sub-market. The second half, or 40,000 m², was provided by 20 small to medium-sized deals.

The East region is in third place with 41,400 m², or 16.6%, having previously been in second place (2021: 74,700 m², or 24.8%). The East saw the clearest year-on-year decline in relative share, dropping 8.3 percentage points. It also saw the biggest absolute loss: Down 45%, take-up nearly halved. Only one of the top deals (FS.COM, with a share of 21.3%) took place in the East region. Most of the region’s take-up came from 15 other deals (32,600 m², or 78.7%).

As in the previous year, the South region is in last place with 35,700 m², or 14.3%, compared with 37,300 m², or 12.4%. Despite the absolute decline of 4%, the region’s relative share increased slightly (up 1.9 percentage points from 12.4% to 14.3%) due to the weak performance of 2022 as a whole. The largest deal in full-year 2022, that of Winning BLW for 28,000 m², took place in the South and contributed the majority (around 80%) of the take-up. The other fifth was spread among seven other lettings.

Manufacturing tops sector ranking

For the first time since 2019, manufacturing once again tops the sector ranking by take-up with a considerable 40.1%, or 100,200 m² (compared with third place in 2021 with 70,700 m², or 23.5%). This sector thus advanced two places at once. At the same time, it is the only sector that saw absolute growth in take-up in 2022, with a significant increase of 41.7% (from 70,700 m² in 2021). Manufacturing was also the category with the greatest relative growth of 16.6 percentage points.

With 25 deals, the manufacturing sector accounts for the second-highest number of lettings, including the top deals by Winning BLW for 28,000 m² (largest deal in 2022), Proton Motor Fuel Cell GmbH (13,200 m²) and Mynaric (11,000 m²), which together contributed 52,200 m², or around half of take-up.

The logistics/distribution sector dropped one place year on year, taking second place with 73,500 m², or 29.4%, (compared with 98,600 m², or a 32.8% share in 2021). At 3.4 percentage points, its relative share decreased only slightly. It accounts for 31 deals in total, including two top deals with DHL (14,000 m²) and Rhenus Archive Services (8,700 m²), which together contributed 22,700 m², or 31%.

Retail is in third place with 57,200 m², or 22.9%. Like logistics/distribution, it has dropped one place after 78,100 m², or 25.9%, in the previous year. Only one top deal is attributable to this category: the e-commerce company FS.COM accounts for 8,800 m², or 15.4% of take-up. The remaining 48,400 m², or 84.6%, comprises 22 other deals.

As in all previous years since 2019, the retail category is dominated by traditional retail with a share of more than three-quarters or 44,200 m² of take-up. E-commerce accounts for 22.7% of take-up, or 13,000 m². Two-thirds of take-up are attributable to the FS.COM deal.

Still in last place is the “Other” category with 19,100 m², or a share of 7.6%. Compared with 53,600 m² and 17.8%, it is the category with the clearest loss in relative share (down 10.2 percentage points). While the biggest registered deal for 24,000 m² in Kirchheim, concluded by a government authority, was crucial in the previous year, none of the top deals are now in the “Other” category.

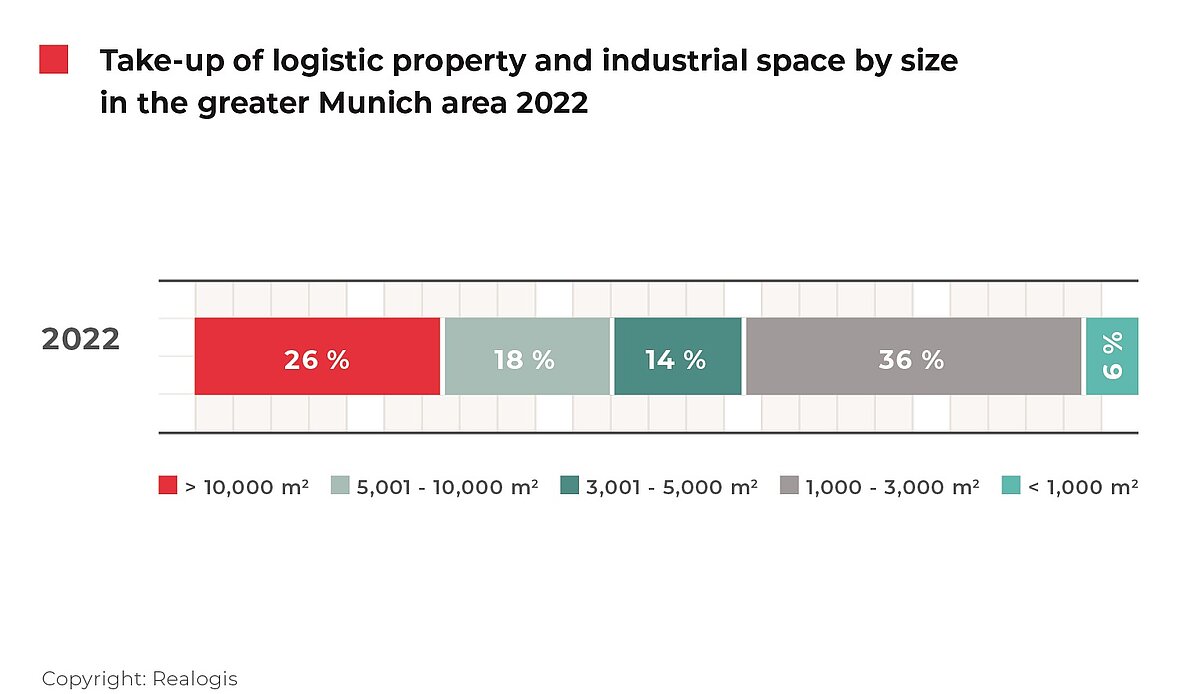

Greater Munich area dominated by small lettings

In contrast to the previous year, we saw that large spaces of 10,001 m² or more accounted for the second-highest amount of space in 2022 at 66,200 m², or 26.5% (2021: 90,600 m², 30.1%). The take-up is entirely attributable to the top four deals in 2022 by Winning BLW (28,000 m²), DHL (14,000 m²), Proton Motor Fuel Cell GmbH (13,200 m²) and Mynaric (11,000 m²). In the previous year, there were seven deals in this size class. The share of take-up decreased by 3.6 percentage points compared with 2021.

As in full-year 2021, larger spaces between 5,001 and 10,000 m² took third place with 44,400 m², or 17.8%, as against 67,000 m², or 22.3%. Two of the top deals in 2022 as a whole are attributable to this category, namely FS.COM (8,800 m²) and Rhenus Archive Services (8,700 m²), which together accounted for 17,500 m², or around 40%. Overall, six deals were recognised in this category, which is five fewer than the previous year’s eleven. This size category saw the greatest year-on-year decline in share of take-up of 4.5 percentage points.

Like last year, medium-sized spaces between 3,001 and 5,000 m² were in fourth place with a share of 14.4%, or 36,100 m², compared with 39,900 m², or 13.3%. There were nine deals in this category, two fewer than in the previous year.

Smaller spaces between 1,000 and 3,000 m² were the winning size class with a share of 35.5%, or 88,800 m². Coming from second place in 2021 as a whole, they made the clearest gain in relative share of 8.1 percentage points. Apart from spaces between 3,001 and 5,000 m², this is the only category that grew. As in the previous year, this category accounted for the highest number of deals: at 49, there was even one more than last year.

The smallest spaces of less than 1,000 m² are again in last place with 14,500 m², or 5.8% (2021: 21,100 m², or 7%). With a total of 22 deals, there were eleven fewer than in the previous year, but still the second most among all categories.

Prime and average rents rise to record highs

Prime rent has climbed by a considerable 14.7% to a new high of EUR 9.75/m². At the beginning of 2023, therefore, prime rent is clearly scratching at the EUR 10 mark. Looking at the past five years, it rose in four out of the five.

The five-year average of EUR 8.35/m² was exceeded by 16.8%.

The average rent has also increased again following the stagnation of the previous year, albeit more moderately than prime rent with growth of 5.8% to currently EUR 7.25/m². Looking at the past five years, it climbed in three out of the five.

The five-year average of EUR 6.89/m² was exceeded by 5.2%.

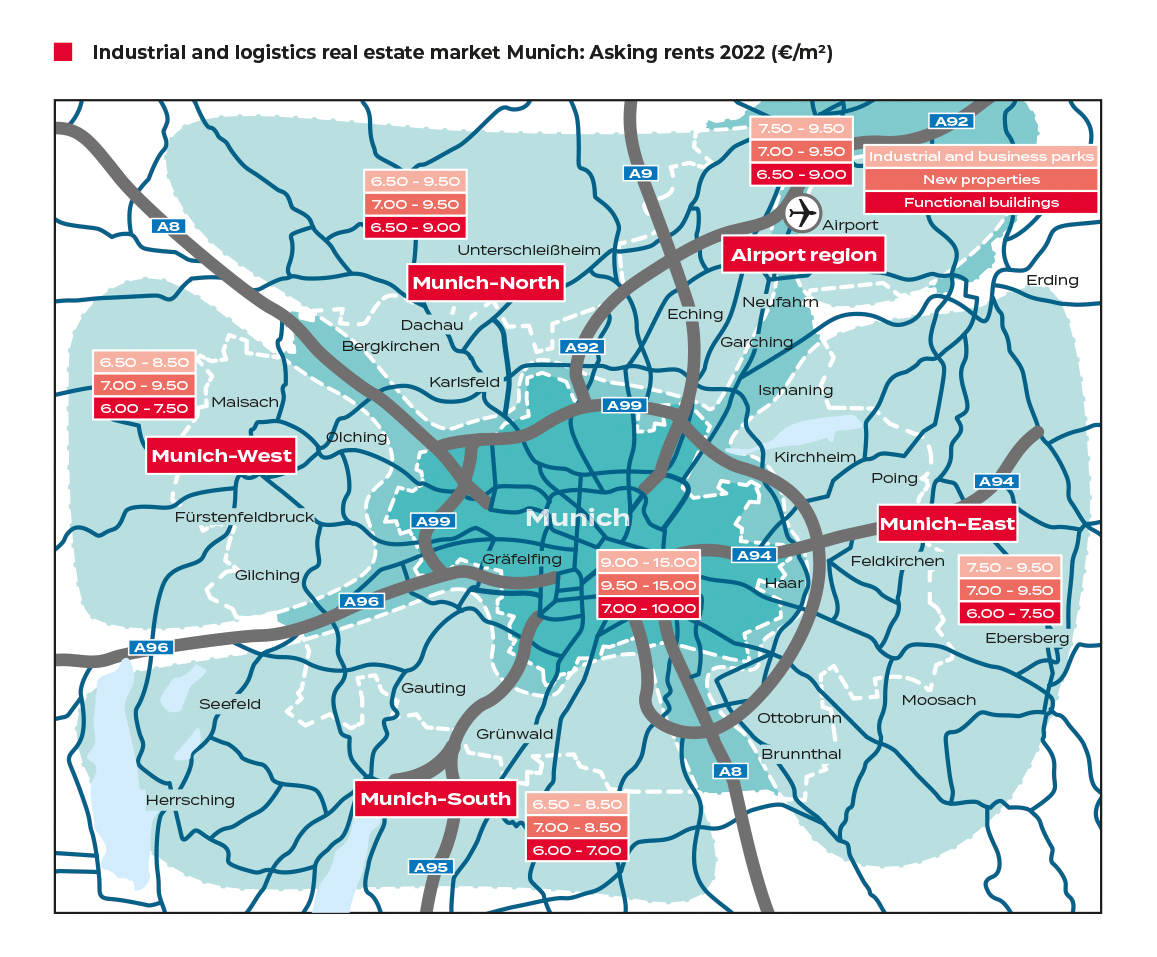

To the rent price maps:

Order the complete market report as PDF