HOCHWERTIG | 650 m² HALLE | 800 m² AUSSTELLUNG

ID: 998947DetailsGarching, repräsentatives Produktionsgebäude mit hochwertigen Büroflächen

ID: 93135Detailsca. 400 m² große, ebenerdige Lager-Produktionshalle mit Meisterbüro in Top Lage

ID: 1036679DetailsDirekt am Autobahnkreuz Ulm/Elchingen - Neubau multifunktionaler Logistik- und Produktionsflächen

ID: 994300DetailsLOGISTIK | RAMPEN | FREIFLÄCHE

ID: 1008605DetailsLager-/Logistik | Neubau | Rampen | teilbar | ebenerdig

ID: 1016255DetailsGEWERBEPARK | ERSTBEZUG | TOP-LAGE

ID: 996681DetailsBremen, ca. 1.300 m² Lager-/ Logistikfläche zu vermieten

ID: 1032273DetailsMünchen - Nord, Hallen- und Freiflächen in Bestlage zu vermieten

ID: 101077DetailsPROVISIONSFREI | GEWERBEPARK | FLEXIBEL

ID: 1000973DetailsArnsdorf | ca. 9.000 m² | Lager & Logistik | Betonrampe & ebenerdig | teilbar ab 2.000

ID: 1009874DetailsRepräsentativer Gewerbepark

ID: 1005086Detailsca. 1.350 m² große, ebenerdige Hallenfläche mit Büro

ID: 1035432DetailsPRODUKTION | LAGER | RAMPE

ID: 991522DetailsGarching, Neubau von ca. 8.000 m² Lager-,Forschungs- und Bürofläche

ID: 1030576DetailsMunich-North, warehouse and office spaces for rent

ID: 1033335DetailsMunich-North, warehouse and office spaces for rent

ID: 1024609DetailsMunich-North, warehouse and office spaces for rent

ID: 1034331DetailsMunich-North, warehouse and office spaces for rent

ID: 1002692DetailsMunich-North, warehouse and office spaces for rent

ID: 1034768DetailsMunich-North, warehouse and office spaces for rent

ID: 1034670DetailsMunich-North, warehouse and office spaces for rent

ID: 1034767DetailsMunich-North, warehouse and office spaces for rent

ID: 1025539DetailsMunich-North, warehouse and office spaces for rent

ID: 1010949DetailsMunich-North, warehouse and office spaces for rent

ID: 1032598DetailsAugsburg, site with about 2.500 sqm for rent

ID: 9040DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031912DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031769DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031836DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1028145DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030724DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030615DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1023871DetailsGladback, warehousing space for wholesale or retail for rent

ID: 95769DetailsGladback, warehousing space for wholesale or retail for rent

ID: 1013489DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1025426DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1026621DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1022435DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1023380DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1014315DetailsNeuss, approx. 1,295 sqm warehouse space in a business park for rent

ID: 997156DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1017665DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1019585Details

Do you have a question? Leave your contact details here and we will call you back!

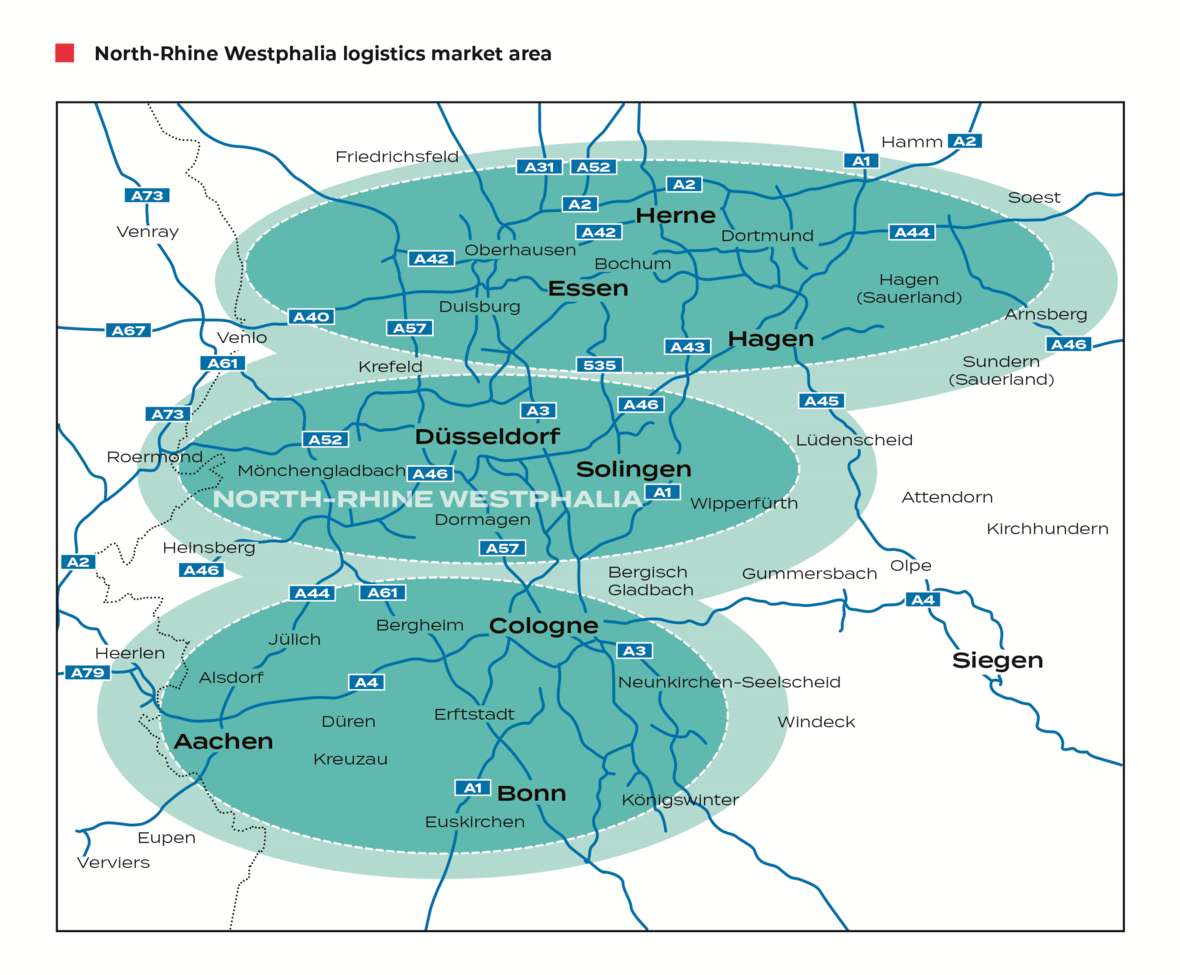

Market report North Rhine-Westphalia for H1 2022

- About the logistics market in the economic region

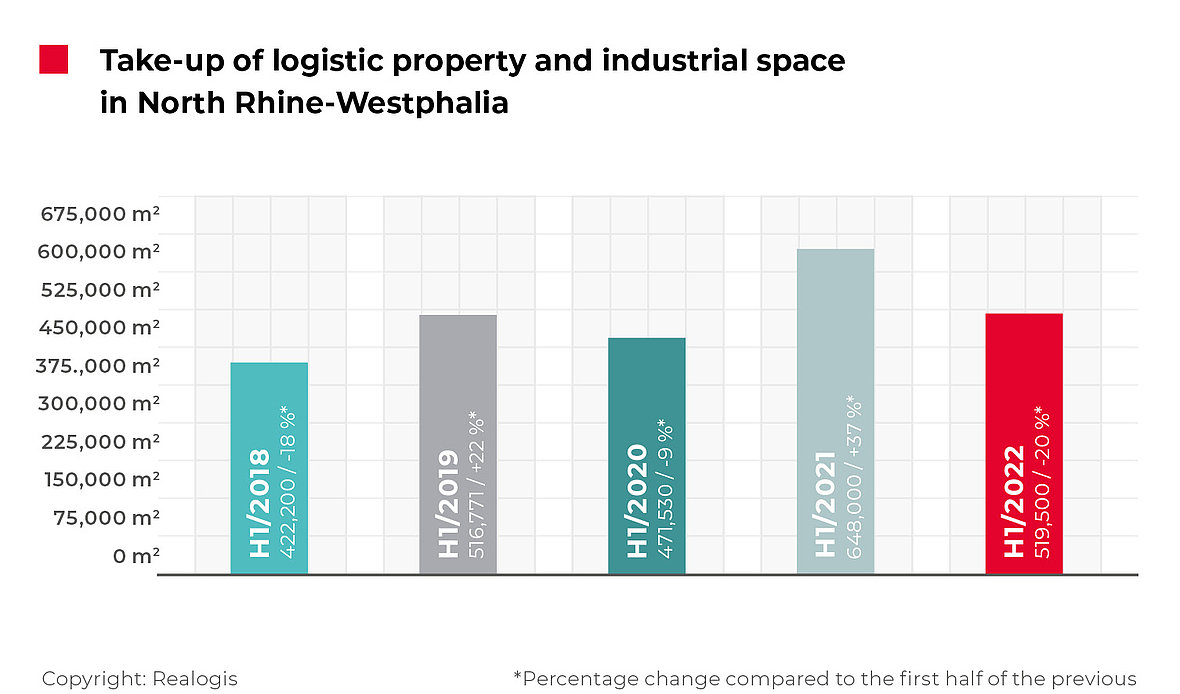

The North Rhine-Westphalia market for rental and owner-occupied industrial and logistics properties and business parks has suffered a severe setback compared to the previous year’s record levels in the first six months of the current year. According to our data, take-up by all market participants on the top markets of Düsseldorf, Cologne and the Ruhr area in the first half of 2022 adds up to a total volume of 519,500 m².

After the record 648,000 m² in the same period of the previous year, the best half-year ever on our books, take-up was down by 19.8% in the first half of 2022 and all sub-markets reported losses. However, the current result is still the second-best half-year over the past five reporting periods. This is also reflected by the five-year average, which is 515,600 m² and was even topped by 0.8% in the current period.

Facts

Take-up down by approximately 20% – five-year average nonetheless topped

Approximately two thirds of all rentals occurred in existing space

More than 90% of take-up occurring in third-party properties

Big box logistics responsible for more than 50%

Sector ranking: Retail now only in second place

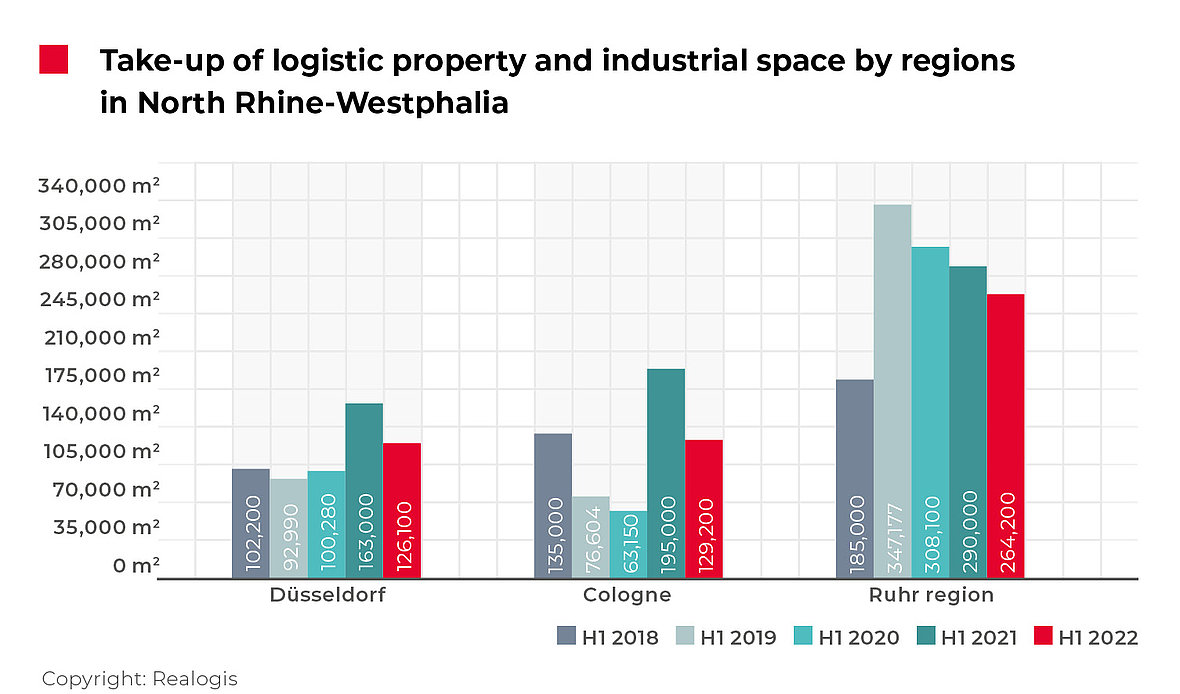

In total, 126,100 m² (24 %) of NRW’s total take-up relates to Düsseldorf, 129,200 m² (25 %) to Cologne and 264,200 m² (51 %) to the Ruhr area. The biggest contracts in H1 2022 were in the Ruhr area: 50,000 m² with ITG, 28,000 m² with JW Fulfillment and 26,900 m² with C&K Logistik. The biggest deal in the Cologne market area was for 30,000 m² with Hammer GmbH & Co. KG, and in the Düsseldorf area this distinction goes to the trading company Picnic at 20,000 m².

In particular, rentals of existing space accounted for most of the half-year’s total volume at 310,600 m² (59.8%), followed by new space at 208,900 m² (40.2%), according to our analysis.

Just two contracts for owner-occupied use

Tenants renting space that they do not own account for the lion’s share at 480,600 m² (92.5%). The only sub-market with contracts for owner-occupied use is Cologne: Moving forward, Siewert & Kau will be using more than 23,000 m² and Offergeld around 14,000 m².

Looking at sub-market take-up for third-party use, the Ruhr area stands out at 264,200 m² (55%), followed by Düsseldorf at 126,100 m² (26.2%) and Cologne at 90,300 m² (18.8%).

Big box logistics responsible for more than 50%

Big box rentals – i.e. large spaces of 10,000 m² or more mainly used for logistics and with a maximum office share of 20% – made a key contribution to total take-up at 348,200 m² (67%), while business parks claimed just 38,700 m² (7.4%). Other space not allocated to either the big box or business park categories accounted for 132,600 m² (25.5%).

The Ruhr area claimed the biggest share of big box rentals at 171,500 m² (49.3%), followed by Cologne at 103,600 m² (29.8%) and Düsseldorf at 73,100 m² (21%). By contrast, Düsseldorf took the lead on business park contracts at 18,400 m² (47.5%), followed by Cologne at 11,100 m² (28.7%) and the Ruhr region at 9,200 m² (23.8%). Other stand-alone space not allocated to either the big box or business park categories accounted for 83,500 m² (63%) in the Ruhr area, 34,600 m² (26.1%) in Düsseldorf and 14,500 m² (10.9%) in Cologne.

Sector ranking: Retail now only in second place

With retail still accounting for one in every two square metres of take-up in the same period of the previous year, the logistics/distribution sector once again secured the majority of all available properties this time and is gaining in significance in both absolute and relative terms (up 28.2 percentage points). At 318,600 m² (61.3%), this sector took almost two out of every three square metres of take-up (H1 2021: 244,420 m², 37.7%). The biggest contracts in this category over the reporting period were with ITG (50,000 m²), Hammer GmbH & Co.KG (30,000 m²), JW Fulfillment (28,000 m²) and C&K Logistik (26,900 m²).

Retail, the previous number one, is currently ranked second at 167,800 m² with a share of 32.3% (H1 2021: 336,250 m², 51.9%), a relative decline of 19.6 percentage points. Within retail, e-commerce claimed the biggest share at 127,600 m² (76%), followed by traditional retail at 40,200 m² (24%). The table of top deals in this category is headed by Deichmann (24,226 m²), followed by Siewert & Kau (23,000 m²), Picnic (20,000 m²), Galaxus (14,000 m²) and NSB Polymers (7,000 m²).

The manufacturing sector has no major deals to report, but still managed a take-up of 31,200 m² or 6% of total take-up (H1 2021: 31,490 m², 4.9%). Last place this time goes to the “Other” category with 1,900 m² or 0.4% (H1 2021: 35,840 m², 5.5%).

This might also be interesting for you:

To the market report Germany

Submarket Düsseldorf

Following the strong prior-year result of 163,000 m², take-up by all market participants of industrial and logistics properties and business parks for rental in Düsseldorf in the first half of 2022 has declined by a substantial 22.6% year-on-year. Nonetheless, take-up of 126,100 m² of industrial and logistics properties by all market participants is a good result and the second-strongest since 2018. This is also reflected by the five-year average, which is currently 116,914 m² and was topped by 7.9% in the past six months.

Existing properties account for the largest share of take-up at 96,000 m² or 76.1%, with new build leases accounting for 30,100 m² or 23.9%.

Big boxes – i.e. large spaces of 10,000 m² or more mainly used for logistics and with a maximum office share of 20% – contributed the biggest share to take-up at 73,100 m² or 58%, while business parks contributed 18,400 m² or 14.6% and other (individual) spaces claimed 34,600 m² or 27.4%.

Approximately 7 out of 10 leases have a term of 5–10 years, with only around 10% of all lease terms for 10 years or longer.

Facts

Take-up down by 22.6%

Big box logistics represents nearly 60%

Prime rent increases by 18.9%

2023: New space completed equals take-up for one year

Every second square metre let to retail

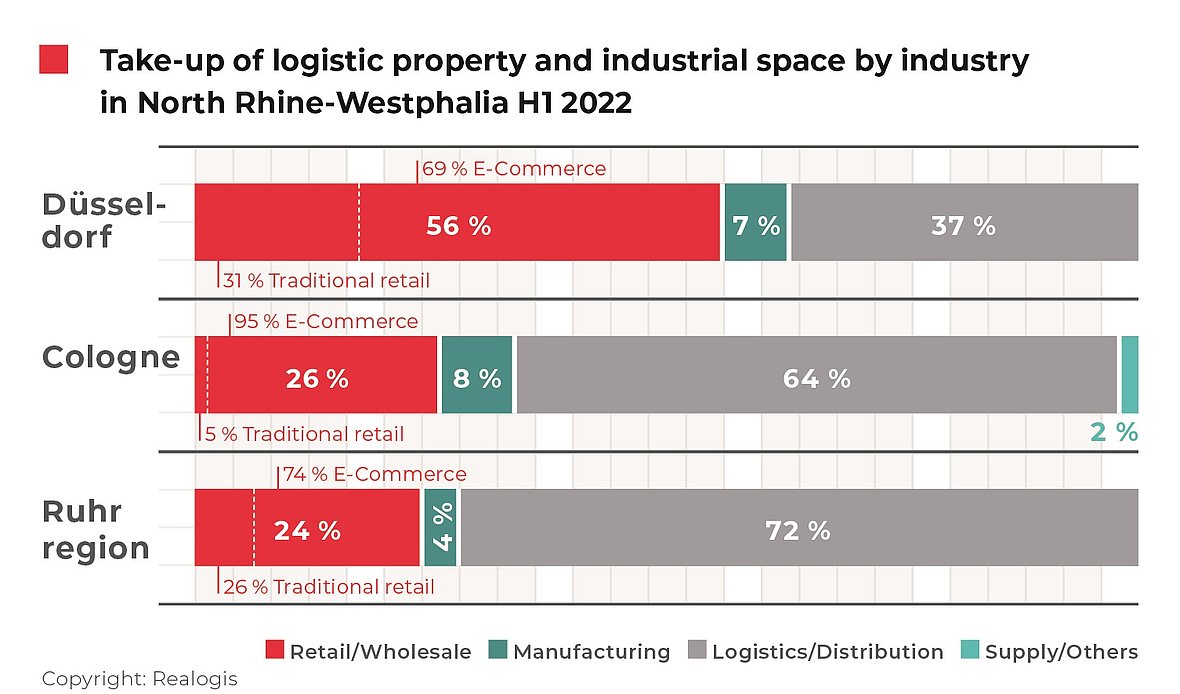

Retail is the leading sector for Düsseldorf’s industrial and logistics property market with a share of 71,300 m² or 56.5% (H1 2021: 48,900 m² or 30%). The sector thus made substantial gains in absolute terms, also increasing its relative importance among all sectors the most significantly with a rise of 26.5 percentage points. Picnic, Galaxus and NSB Polymers represent the three biggest deals signed in the retail sector. Combined, they account for 41,000 m² or 57.5% of the sector.

Düsseldorf: Lessors with highest take-up

Picnic, approx. 20,000 m² (New build), Retail

Galaxus, approx. 14,000 m² (New build), Retail

Wisag Logistics, approx. 11,500 m² (Existing property), Logistics

Filzhut Lager+Logistik GmbH, approx. 11,000 m² (New build), Logistics

Rhenus, approx. 10,000 m² (New build), Logistics

NSB Polymers, 7,000 m² (New build), Retail

E-commerce is top of the retail category with 49,300 m² or 69.1% ahead of traditional retailwith 22,000 m² or 30.9%.

The logistics/distribution sector takes second place with 46,300 m² or 36.7% (H1 2021: 96,170 m² or 59%), having lost significant ground in terms of absolute take-up and relative importance (decrease of 22.3 percentage points). Three of the top five deals were made in this sector: Wisag Logistics (11,500 m²), Filzhut Lager+Logistik GmbH (11,000 m²) and Rhenus (10,000 m²), representing a combined total of 32,500 m² or 70,2 % of sector take-up.

In third place is manufacturing with 8,500 m² or 6.7% (H1 2021: 13,040 m² or 8%).

Prime rent increases by 18.9%

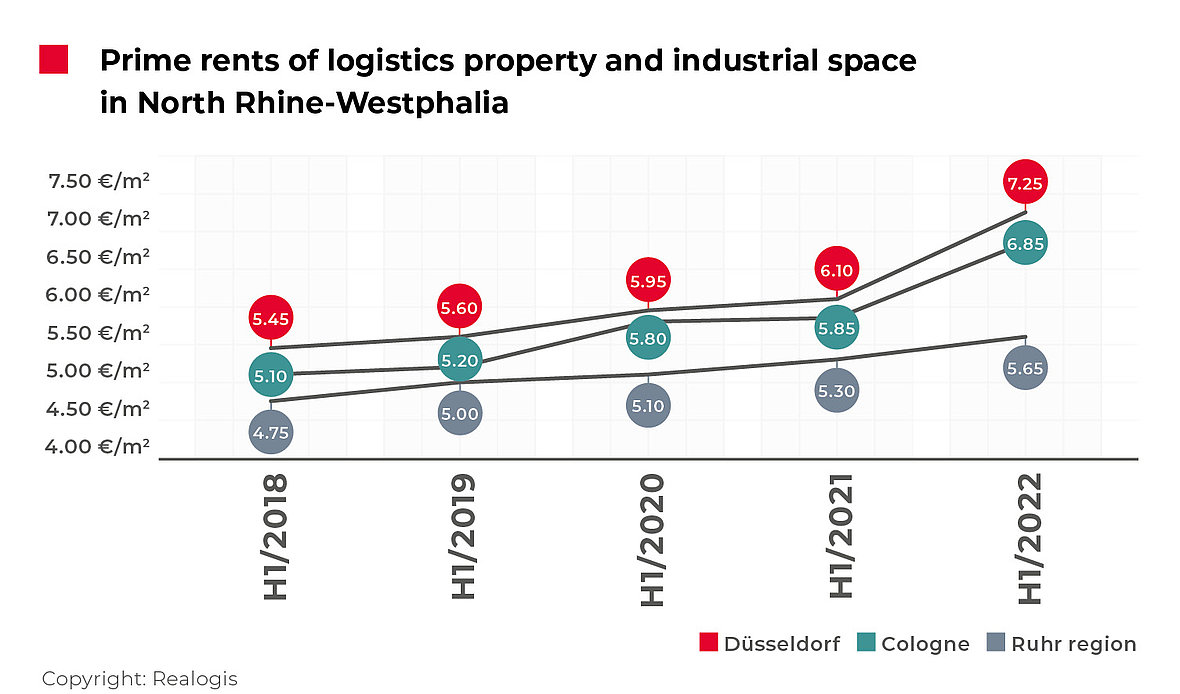

Prime rent for industrial and logistics properties and business parks reached its highest level to date in the first six months of the year with a substantial increase of 18.9% to EUR 7.25/m² (H1 2021: EUR 6.10/m²). According to our data, this is the biggest increase since records began, with the five-year average of EUR 6.07/m² having been exceeded by a whopping 19.4%.

Outlook for 2023:

120,000 m² of new space under development

Just under 120,000 m² of new space is currently being developed by various project developers in the Düsseldorf market area.

All new space in the Düsseldorf market area will be completed next year on a speculative basis – in itself bringing a high volume of state-of-the-art properties onto the market in addition to existing space that will become vacant.

Düsseldorf: Major developments

BEOS, approx. 50.000 m² (speculative), Q1 2023

LogProject, approx. 30.000 m² (speculative), Q3 2022

Panattoni, approx. 17.000 m² (speculative), Q1 2023

Hagedorn/Dietz, 11.000 m² (speculative), Q1 2023

Aconlog, 9.000 m² (speculative), Q1 2023

Submarket Cologne

The market for business parks and industrial and logistics properties in the Cologne metropolitan region has failed to match the strong figures for the first half of the previous year. We saw a decline of 33.7% to 129,200 m² of rental and owner-occupancy space in the first half of 2022.

The half-year result achieved by all market participants is nonetheless a good result following the absolute record in the previous year. Within the last five comparative periods, the take-up achieved between January and June 2022 is only just behind H1 2018’s 135,000 m², and thus the third-strongest of the past five first half-years. This is also shown by the five-year average of 119,791 m², which this time was topped by 8%.

Rentals and owner-occupancy in new buildings account for the biggest share of the current result at 77,900 m² (60.3%), followed by rentals in existing properties at 51,300 m² (39.7%).

Among the three top NRW markets, only Cologne had any owner-occupancy deals: Siewert & Kau has taken up 23,000 m² for development and use, and the logistics company Offergeld has taken up around 14,000 m². More than 90,000 m², and thus approximately 70% of all new use in the Cologne market area, is taking place in properties owned by third parties.

Facts

Rental and owner-occupancy market down 33.7%

More than 60% of all new contracts for new buildings

Cologne the only market in NRW with two owner-occupancy contracts

Sector ranking: Commerce crashes

Big boxes – i.e. large spaces upwards of 10,000 m² mainly used for logistics and with a maximum office share of 20% – made the biggest contribution to total take-up at 103,600 m² (80.2%), while business parks are responsible for 11,100 m² (8.6%). Leases for standalone or partial areas not located in either big boxes or business parks account for 14,500 m² (11.2%).

Like on other top NRW markets, most of the contracts in Cologne have terms of between five and ten years (70% of the total number of contracts). Around a seventh (approximately 15%) of deals were for terms of either one to four years or more than ten.

The largest project development is in Düren, where Logic Green is speculatively developing 30,000 m², which is expected to be finished in the first quarter of 2023. This space has already been let by us to the user Hammer GmbH & Co. KG.

Logistics/distribution overtakes retail

Unlike in the same period of the previous year, retail is no longer the top-ranking sector, this honour instead goes to logistics/distribution. With a share of 82,300 m² (63.7%), it dominated take-up in the first half of 2022, coming from second rank with 40,950 m² (21%). It is therefore currently gaining most impressively in relative significance (up 42.7 percentage points). Four of the top five deals counted towards this. Together, they account for take-up of 82,300 m², alone responsible for 82% of take-up in the logistics/distribution sector.

Cologne: Lessors with highest take-up

Hammer GmbH & Co. KG, approx. 30,000 m² (New build), Logistics

Siewert & Kau, approx. 23,000 m² (New build), Retail

Offergeld, approx. 14,000 m² (New build), Logistics

Gras Spedition, approx. 13,750 m² (Existing property), Logistics

Astral, approx. 9,909 m² (Existing property), Logistics

Retail claimed 34,000 m² and thus 26.3% of total take-up in the first half of 2022. It has plummeted year-on-year, losing 100,000 m² of take-up in absolute terms or a relative share of 46.7 percentage points. The biggest contribution within the sector came from e-commerce with 32,300 m² (95%), while conventional retail lost took up just 1,700 m² (5%).

In third place is manufacturing with currently just 11,000 m² or 8.5% (H1 2021: 9,750 m² or 5%). In last place is the miscellaneous “Other” category with 1,900 m² (1.5%).

Prime rent increases by 17%

Following the extremely moderate increase in prime rent in the previous first half-year of 0.9% to EUR 5.85/m² in H1 2021, the prime rent has risen faster than ever before over the past half-year. It has increased by 17% to the current high-to-date of EUR 6.85/m². The five-year average of EUR 5.76/m² has also been topped by a significant 18.9%.

Submarket Ruhr Region

Like other top markets in North Rhine-Westphalia, the Ruhr region once again recorded losses in the letting and owner-occupancy of logistics and industrial space and business parks in the first half of 2022. According to our data, the market was unable to match the previous year’s level of 290,000 m² and declined by 8.9% to take-up of 264,200 m² by all market participants in the first half of the current year.

This represents the second-weakest figure in the history of the first halvesof the past five years. Only H1 2018 was lower by around 30% at 185,000 m². However, it is only around 5% below the current five-year average of 278,895 m².

Demand for space among manufacturers, retailers and their logistics providersremains undiminished. However, there is a lack of available space and project developments.

All take-up was in third-party properties, i.e. the market did not record any owner-occupancy deals.

According to our analysis, the majority of take-up is attributable to big boxes with 171,500 m² or 64.9 %, We define this category as large spaces of 10,000 m² or more, with logistics as the main type of use and an office share of no more than 20%. Business parks account for only 9,200 m² or a share of 3.5%. A total of 83,500 m² or 31.6% of all space was rented in other free-standing properties that cannot be classified as either business parks or big-box properties.

65% of deals with a term of 5 to 10 years

Most leases for industrial and logistics properties and business parks in the Ruhr region were concluded with a term of 5 to 10 years. Around 25% were attributable to terms between 1 and 4 years, while very long-term leases of 10 years or more accounted for around 10%.

Sector ranking: logistics ahead of retail again

In the Ruhr region, logistics/distribution was the leading sector again in the first six months of the year with 190,000 m² or 71.9% (H1 2021: 107,300 m² or 37%). It thus marked the biggest relative increase year-on-year at 34.9 percentage points. The top deals included ITG at 50,000 m², followed by JW Fulfillment at 28,000 m², C & K Logistik at 26,900 m² and JD.com at 16,147 m².

Ruhr region: Lessors with the highest take-up

ITG, approx. 50,000 m² (New build), Logistics

JW Fulfillment, approx. 28,000 m² (Existing property), Logistics

C & K Logistik, approx. 26,900 m² (New build), Logistics

Deichmann, approx. 24,226 m² (Existing property), Retail

JD.Com, approx. 16,147 m² (New build), Logistics

In second place with 23.7% or 62,500 m² was the retail sector, which had come first in the same period of the previous year. Compared to 145,000 m² or 50% in H1 2021, it lost considerable ground in both absolute and relative terms (down 26.3 percentage points). The biggest contribution came from e-commerce with 46,000 m² or 73.6%, followed by traditional retail with 16,500 m² or 26.4%. With the Deichmann deal for 24,226 m², one of the top deals was attributable to the overarching category of retail and accounted for 38.8% of total take-up in this category.

In third place is the manufacturing sector with 11,700 m² or 4.4% (H1 2021: 8,700 m² or 3%).

Prime rent increases by 6.6%

Looking at the prime rent, we registered a rising trend from the first halves of the previous years. Rent for modern logistics properties is becoming more expensive and has risen by 6.6% – a moderate rate compared to other markets in North Rhine-Westphalia – to its high to date of EUR 5.65/m², although it remains well below the prime rents in Düsseldorf (EUR 7.25/m²) and Cologne (EUR 6.85/m²). The five-year average for the first half of the year of EUR 5.16/m² is exceeded by 9%.

Outlook:

124,000 m² of new space under development

In the coming year, we anticipate a total new construction volume of more than 120,000 m² in the Ruhr region in four different markets alone. This is a good sign for companies that are focussing on the A1 and A2 transport hubs with their logistics locations or wish to locate north of Duisburg in 2023.

Ruhr region: Major developements

Hagen, approx. 45,000 m² (BTS), Q4 2023

Dortmund, approx. 35,000 m² (Speculative), Q1 2023

Voerde, approx. 30,000 m² (Speculative), Q1 2023

Gladbeck, approx. 14,000 m² (Speculative), Q2 2023

To the rent price maps:

Order the complete market report as PDF