HOCHWERTIG | 650 m² HALLE | 800 m² AUSSTELLUNG

ID: 998947DetailsGarching, repräsentatives Produktionsgebäude mit hochwertigen Büroflächen

ID: 93135Detailsca. 400 m² große, ebenerdige Lager-Produktionshalle mit Meisterbüro in Top Lage

ID: 1036679DetailsDirekt am Autobahnkreuz Ulm/Elchingen - Neubau multifunktionaler Logistik- und Produktionsflächen

ID: 994300DetailsLOGISTIK | RAMPEN | FREIFLÄCHE

ID: 1008605DetailsLager-/Logistik | Neubau | Rampen | teilbar | ebenerdig

ID: 1016255DetailsGEWERBEPARK | ERSTBEZUG | TOP-LAGE

ID: 996681DetailsBremen, ca. 1.300 m² Lager-/ Logistikfläche zu vermieten

ID: 1032273DetailsMünchen - Nord, Hallen- und Freiflächen in Bestlage zu vermieten

ID: 101077DetailsPROVISIONSFREI | GEWERBEPARK | FLEXIBEL

ID: 1000973DetailsArnsdorf | ca. 9.000 m² | Lager & Logistik | Betonrampe & ebenerdig | teilbar ab 2.000

ID: 1009874DetailsRepräsentativer Gewerbepark

ID: 1005086Detailsca. 1.350 m² große, ebenerdige Hallenfläche mit Büro

ID: 1035432DetailsPRODUKTION | LAGER | RAMPE

ID: 991522DetailsHochwertige Hallenfläche | ebenerdig | Neubau

ID: 1028652DetailsGarching, Neubau von ca. 8.000 m² Lager-,Forschungs- und Bürofläche

ID: 1030576DetailsMunich-North, warehouse and office spaces for rent

ID: 1033335DetailsMunich-North, warehouse and office spaces for rent

ID: 1024609DetailsMunich-North, warehouse and office spaces for rent

ID: 1034331DetailsMunich-North, warehouse and office spaces for rent

ID: 1002692DetailsMunich-North, warehouse and office spaces for rent

ID: 1034768DetailsMunich-North, warehouse and office spaces for rent

ID: 1034670DetailsMunich-North, warehouse and office spaces for rent

ID: 1034767DetailsMunich-North, warehouse and office spaces for rent

ID: 1025539DetailsMunich-North, warehouse and office spaces for rent

ID: 1010949DetailsMunich-North, warehouse and office spaces for rent

ID: 1032598DetailsAugsburg, site with about 2.500 sqm for rent

ID: 9040DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031912DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031769DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031836DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1028145DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030724DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030615DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1023871DetailsGladback, warehousing space for wholesale or retail for rent

ID: 95769DetailsGladback, warehousing space for wholesale or retail for rent

ID: 1013489DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1025426DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1026621DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1022435DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1023380DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1014315DetailsNeuss, approx. 1,295 sqm warehouse space in a business park for rent

ID: 997156DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1017665DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1019585Details

Do you have a question? Leave your contact details here and we will call you back!

Market report Frankfurt full year 2022

- About the logistics market in the economic region

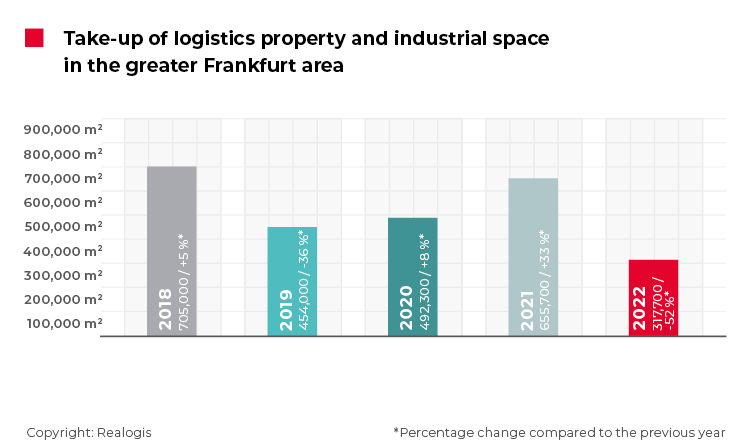

Frankfurt market for logistics, warehousing and industrial space halves

According to our latest analysis, the market for logistics, warehousing and industrial space in Frankfurt has halved. The total take-up of rental space by all market participants came to 317,700 m² in 2022. Compared to the previous year’s result of 655,700 m², this represents a decrease of 51.5%, the biggest ever recorded since 2014. It also fell short of the current five-year average of 524,940 m² by a substantial 39.5%.

Facts

- Total annual take-up at only 317,700 m²

- A substantial 39.5% short of five-year average of 524,940 m²

- Existing properties responsible for more than two thirds at 238,700 m²

- Regional ranking: Rhine-Main South accounts for half of all new deals

- Prime rent for logistics climbs by 2.8%

According to our observation, the increased shortage of space in the Frankfurt/Rhine-Main market area is taking its toll. In all sectors, take-up declined by roughly half in 2022. Companies from the retail, industrial and logistics sectors would like to locate closer to their sales and production markets, not least to increase employee availability and mitigate the effects of more expensive gasoline prices. However, there is hardly any available space or development sites, forcing users to seek properties outside the market area instead.

The lion’s share of take-up was attributable to the existing properties category at 238,700 m² or 75.2%. By contrast, new-build properties represented only 16.7% of take-up at 53,100 m². Brownfields played a less important role, accounting for 25,800 m² or 8.1% of total take-up. As in other metropolitan regions, brownfields will gain increased significance on the Frankfurt market over the coming years in order to develop new buildings within the market area.

Big-box properties – i.e. properties upwards of 10,000 m² mainly used for logistics and with an office share of no more than 20% – contributed almost a third of total take-up at 98,700 m² or 31.1% in 2022. The business parks category accounted for 130,300 m² or 41%. We define a business park as a contiguous business district that is developed and implemented with a uniform concept and whose infrastructure is used jointly by the companies based there. Other properties, i.e. those attributable to neither big boxes nor business parks, accounted for 88,700 m² or 27.9%.

Biggest deals in full-year 2022

Between January and December, we observed a total of 92 dealsin the logistics, warehousing and industrial space segment. These included five top deals with a combined total of 98,704 m², representing around a third of total take-up.

Top deals

B+S, Rhine-Main east, approx. 39,500 m² (existing property), logistics

Rexel, Rhine-Main south, approx. 26,000 m² (new build), retail

Atrikom, Mainz/Wiesbaden, approx. 12,532 m² (new build), logistics

Grieshaber Logistics, Rhine-Main south, approx. 10,495 m² (new build), logistics

Breitfeld und Schliekert, Rhine-Main east, approx. 10,177 m² (existing property), retail

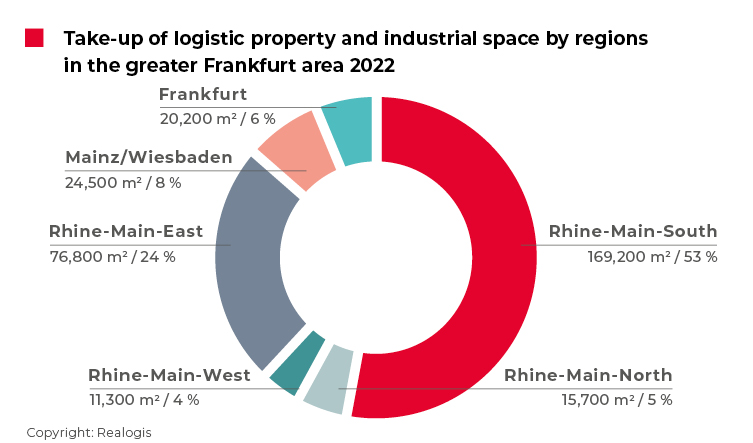

Regional ranking: Rhine-Main South accounts for half of all new deals

Properties in the Rhine-Main South region offered the highest availability in 2022. At 169,200 m², they accounted for more than one in two square metres of total take-up. Although the region thus increased its market share by 14.4 percentage points, it recorded a significant year-on-year decrease of 33.5% in absolute terms (2021: 254,500 m² or 38.8%). The top deals with Rexel and Grieshaber Logistics contributed a total of 36,495 m² or 21.6% of the region’s take-up.

The biggest decline in take-up in the reporting period was in the Rhine-Main East region: After reaching 261,500 m² or 40% in the previous year, it fell by 184,700 m² to just 76,800 m² or 24.2% in 2022 (second place). It also saw the biggest relative decline of 15.8 percentage points. B+S and Breitfeld und Schliekert were the major lessors in the region, accumulating 49,677 m² or 57% of take-up.

In third place was Mainz/Wiesbaden with 24,500 m² or 7.7% after 11,400 m² or 1.7%. Besides Rhine-Main South, this was the only other region to increase its share, in this case by 6.0 percentage points. It was also the only region to augment its take-up in absolute terms, more than doubling this result largely due to the deal with Atrikom.

Frankfurt came in fourth with 20,200 m² or 6.4% (2021: 48,600 m² or 7.4%: decrease of 58.4% in absolute terms and 1.1 percentage points in its relative share). Last but one was the Rhine-Main North region with 15,700 m² or 4.9% (2021: 44,900 m² or 6.8%; decrease of 1.9 percentage points in relative terms and 65% in absolute take-up). With take-up of 11,300 m² or 3.6% (2021: 34,900 m² or 5.3%), the Rhine-Main West region’s relative share shrunk by 1.8 percentage points and its absolute take-up by a substantial 67.7%.

The majority of the weak annual result is attributable to the declines in the two regions of Rhine-Main East and Rhine-Main South. In recent years – as in 2022 – these have always represented between 70% and 80% of take-up of logistics, warehousing and industrial space, although the market in the two regions has declined by 270,000 m².

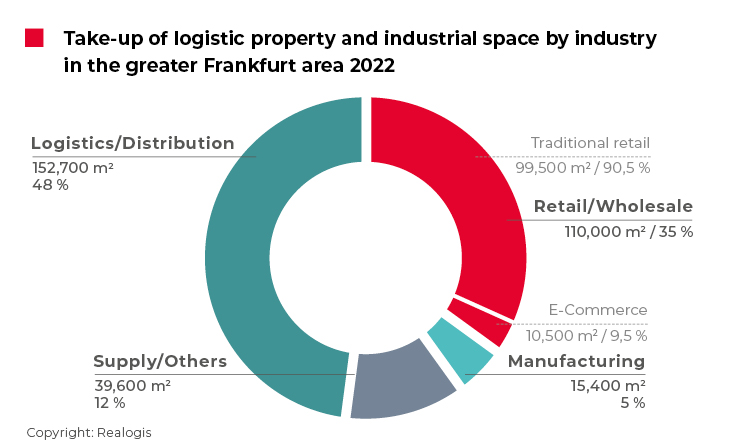

Sector ranking: Logistics/distribution ahead of retail

Logistics/distribution headed the sector ranking in the Frankfurt area again in 2022, with take-up of 152,700 m² or 48.1%. Although logistics/distribution only saw a small decrease of 1.9 percentage points in its relative share, take-up here decreased the most out of all sectors in absolute terms, falling by 53.4% compared to 327,800 m² in 2021. Three of the top lessees – B+S, Atrikom and Grieshaber Logistics – contributed a total of 62,527 m² or 41% of the sector’s take-up.

In second place was retail again with 111,000 m² or 34.6%, after 255,800 m² or 39% in 2021 (decrease of 52.7% in absolute terms and 4.4 percentage points in relative terms). This category included the two remaining top lessees, Rexel and Breitfeld und Schliekert, with a total of 36,177 m² or 30% of the sector’s take-up.

Market activity here was dominated by traditional retail with 99,500 m², corresponding to more than 9 out of 10 square metres taken up in the retail sector, followed by e-commerce with 9.5% or 10,500 m².

The miscellaneous category “Other” was in third place again with 39,600 m² or 12.5% after 44,800 m² or 6.8% (increase of 5.6 percentage points in relative terms). Manufacturing played only a minor role in the Frankfurt market area again in 2022 with 15,400 m² or 4.8% (2021: 27,200 m² or 4.2%).

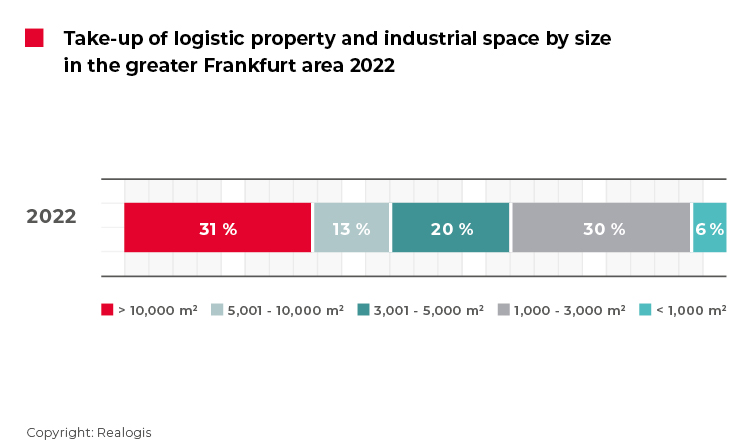

Large spaces responsible for two thirds of take-up

The segment of large spaces of 10,001 m² or more, to which all five top deals were attributable, again had the greatest take-up out of all categories at 98,700 m² and contributed almost a third of take-up on the market as a whole. Compared to the previous year’s figure of 309,900 m², however, this size category saw the biggest decrease in its relative share at -16.2 percentage points and lost 68.2% in absolute terms.

This might also be interesting for you:

To the market report Germany

The category of larger sizes between 5,001 and 10,000 m² contributed 41,200 m² or 13%, putting it in fourth place (2021: 177,900 m² or 27.1%). With a difference of 136,700 m², corresponding to a decrease of 76.8%, this category recorded the second-biggest decline in absolute take-up and a loss in its relative share of 14.2 percentage points.

The category of medium-sized to large spaces between 3,001 and 5,000 m² was in third place with 63,500 m² or 20% (2021: 60,200 m² or 9.2%), having both increased its relative share by 10.8 percentage points and achieved slight growth in absolute take-up of 5.5%.

Spaces between 1,000 and 3,000 m² came to 93,700 m², representing a share of 29.5% (second place). It thus maintained the previous year’s level in absolute terms and gained the most ground out of all categories in relative terms with a 15.2 percentage point increase.

The smallest spaces of less than 1,000 m² came to 20,600 m² or 6.5% of take-up, putting them in last place again (2021: 13,700 m² or 2.1%; increase of 4.4 percentage points in relative share and 50% in absolute terms).

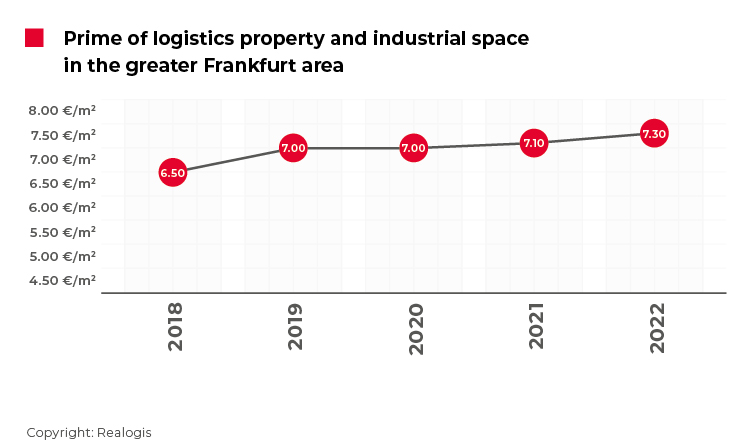

Prime rent for logistics climbs slightly by 2.8%

Despite the shortage of space, the prime rent for logistics properties increasedonly slightly in comparison to other metropolitan regions in Germany by 2.8% as against 2021. In our estimation, the prime rent will also continue to rise in the future as a result of the shortage of space, higher construction costs and interest rate increases.

At the end of 2022 it came to EUR 7.30/m², its highest level to date, after EUR 7.10/m² in 2021. This was 2.8% higher than the five-year average of EUR 6.98/m².

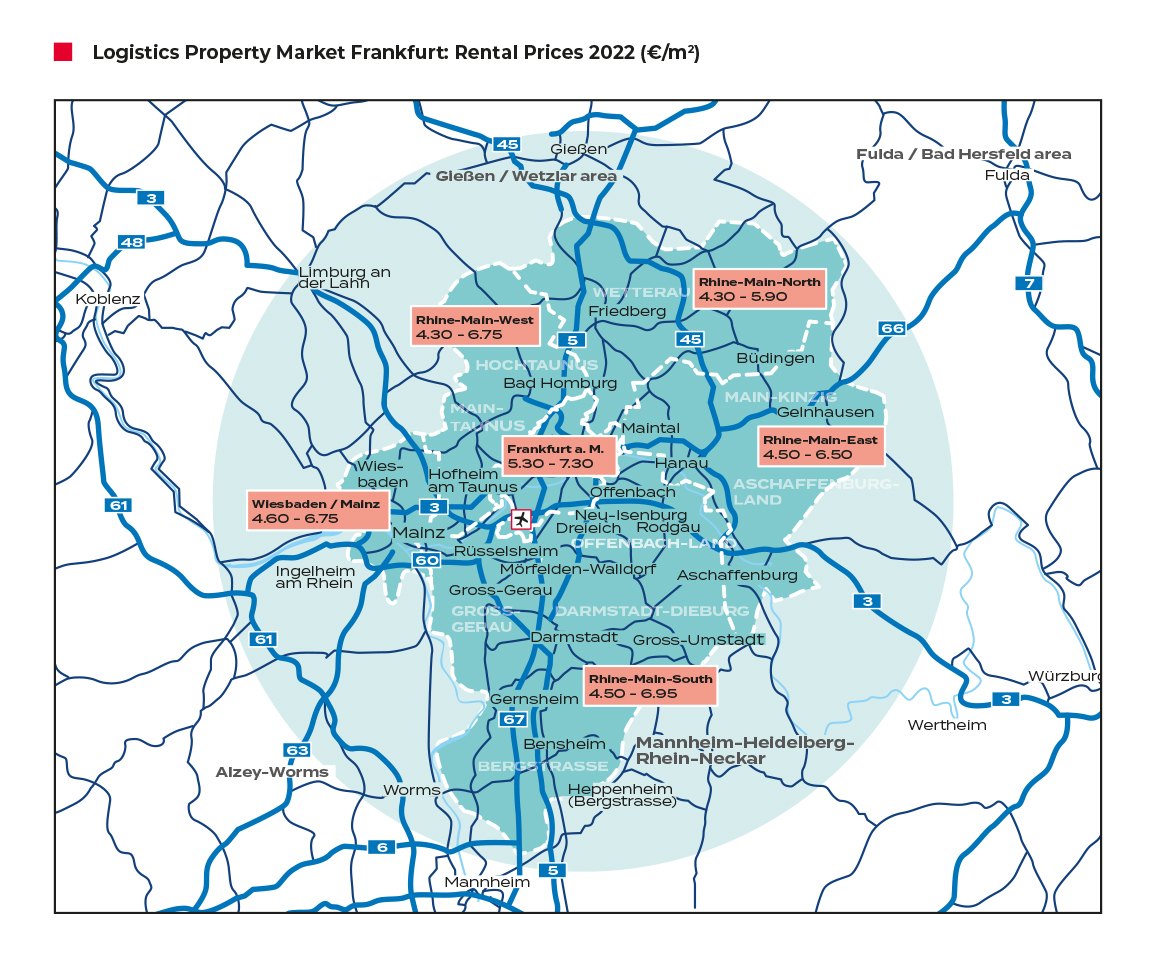

To the rent price maps:

Order the complete market report as PDF