HOCHWERTIG | 650 m² HALLE | 800 m² AUSSTELLUNG

ID: 998947DetailsGarching, repräsentatives Produktionsgebäude mit hochwertigen Büroflächen

ID: 93135Detailsca. 400 m² große, ebenerdige Lager-Produktionshalle mit Meisterbüro in Top Lage

ID: 1036679DetailsDirekt am Autobahnkreuz Ulm/Elchingen - Neubau multifunktionaler Logistik- und Produktionsflächen

ID: 994300DetailsLOGISTIK | RAMPEN | FREIFLÄCHE

ID: 1008605DetailsLager-/Logistik | Neubau | Rampen | teilbar | ebenerdig

ID: 1016255DetailsGEWERBEPARK | ERSTBEZUG | TOP-LAGE

ID: 996681DetailsBremen, ca. 1.300 m² Lager-/ Logistikfläche zu vermieten

ID: 1032273DetailsMünchen - Nord, Hallen- und Freiflächen in Bestlage zu vermieten

ID: 101077DetailsPROVISIONSFREI | GEWERBEPARK | FLEXIBEL

ID: 1000973DetailsArnsdorf | ca. 9.000 m² | Lager & Logistik | Betonrampe & ebenerdig | teilbar ab 2.000

ID: 1009874DetailsRepräsentativer Gewerbepark

ID: 1005086Detailsca. 1.350 m² große, ebenerdige Hallenfläche mit Büro

ID: 1035432DetailsPRODUKTION | LAGER | RAMPE

ID: 991522DetailsGarching, Neubau von ca. 8.000 m² Lager-,Forschungs- und Bürofläche

ID: 1030576DetailsMunich-North, warehouse and office spaces for rent

ID: 1033335DetailsMunich-North, warehouse and office spaces for rent

ID: 1024609DetailsMunich-North, warehouse and office spaces for rent

ID: 1034331DetailsMunich-North, warehouse and office spaces for rent

ID: 1002692DetailsMunich-North, warehouse and office spaces for rent

ID: 1034768DetailsMunich-North, warehouse and office spaces for rent

ID: 1034670DetailsMunich-North, warehouse and office spaces for rent

ID: 1034767DetailsMunich-North, warehouse and office spaces for rent

ID: 1025539DetailsMunich-North, warehouse and office spaces for rent

ID: 1010949DetailsMunich-North, warehouse and office spaces for rent

ID: 1032598DetailsAugsburg, site with about 2.500 sqm for rent

ID: 9040DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031912DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031769DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031836DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1028145DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030724DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030615DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1023871DetailsGladback, warehousing space for wholesale or retail for rent

ID: 95769DetailsGladback, warehousing space for wholesale or retail for rent

ID: 1013489DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1025426DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1026621DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1022435DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1023380DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1014315DetailsNeuss, approx. 1,295 sqm warehouse space in a business park for rent

ID: 997156DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1017665DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1019585Details

Do you have a question? Leave your contact details here and we will call you back!

Market report Frankfurt for the year 2021

- About the logistics market in the economic region

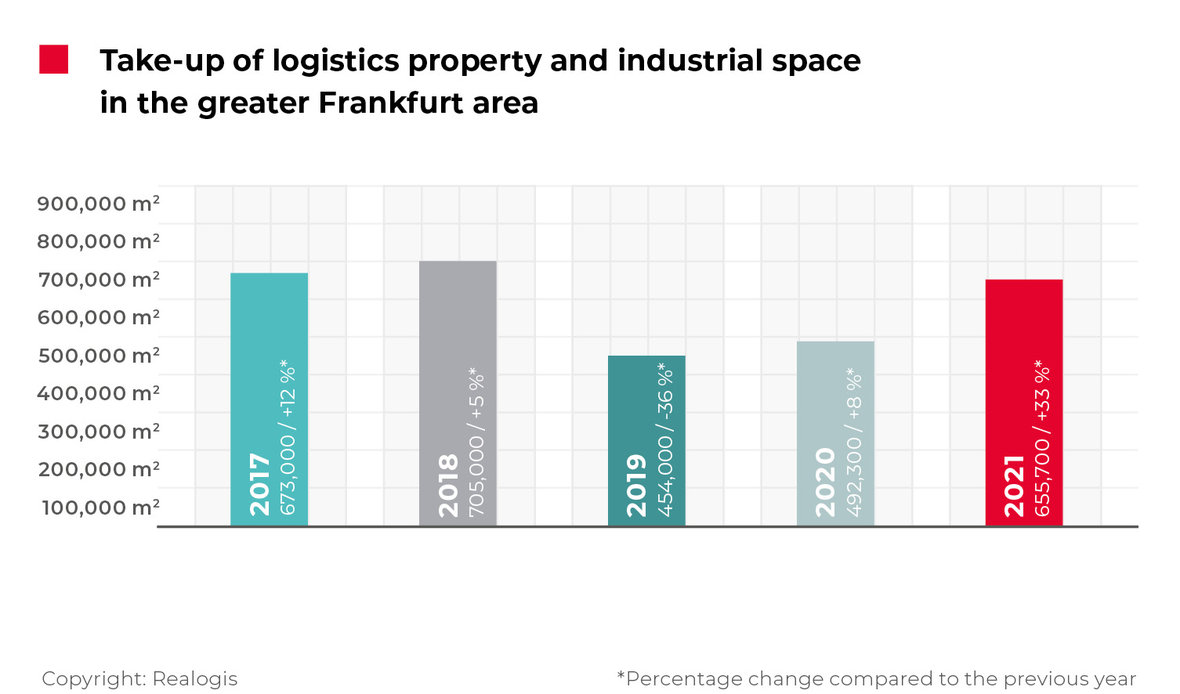

Frankfurt logistics property market back on top in 2021

Take-up for rental and owner-occupied logistics, warehousing and industrial space in the greater Frankfurt/Main area has surged by 33% to 655,700 m² in 2021 (2020: 492,300 m²). This is the third-highest take-up by all market participants and the highest percentage increase since records began. According to our analysis, the massive slump in 2019 and the low growth in 2020 have clearly been overcome.

While take-up had been 22% below the five-year average in 2019, and 16% down in 2020 (578,800 m² and 584,660 m²), in 2021 it was 10% higher again for the first time at 596,000 m².

We registered 113 deals in total by all market participants between January and December 2021. The high number of major deals was a highlight, and the top five deals alone contributed 189,400 m² or 28.9% to total annual take-up.

Facts

Highest percentage growth in five years at 33%

Three mega deals account for more than 40,000 m² each

New players in user groups

Rhine-Main East sub-market riding high

Logistics/ distribution using half of all m²

Approximately 75% of all space relates to one size category

Prime and average rents reach record highs

Forecast: Further rent increases anticipated for sustainable properties

New players in user groups and changing parameters for properties

We had a lot of very similar requests from different food delivery services in 2021. The requests themselves were not unexpected given the pandemic, but their sheer number and their presence as new market participants in this segment was surprising.

This also entails some changes to the parameters for top new logistics buildings. Loading ramps and parking spaces, or open areas, are becoming increasingly important and are in high demand. Express and food delivery services rely on a high volume of fast transport, and property developers are responding to that. As this use is not optimal for developers and owners, we expect to see rents rise for these properties moving ahead.

Lessors with highest take-up

Hager Group, Hammersbach, approx. 40,000 m² (New Build), Retail

ID Logistics, Kleinostheim, approx. 40,000 m² (New Build), Logistics

PepsiCo Deutschland GmbH, Hammersbach, approx. 40,000 m² (New Build), Logistics

B+S GmbH, Alzenau, approx. 37,400 m² (New Build), Logistics

DHL, Florstadt, approx. 32,000 m² (New Build), Logistics

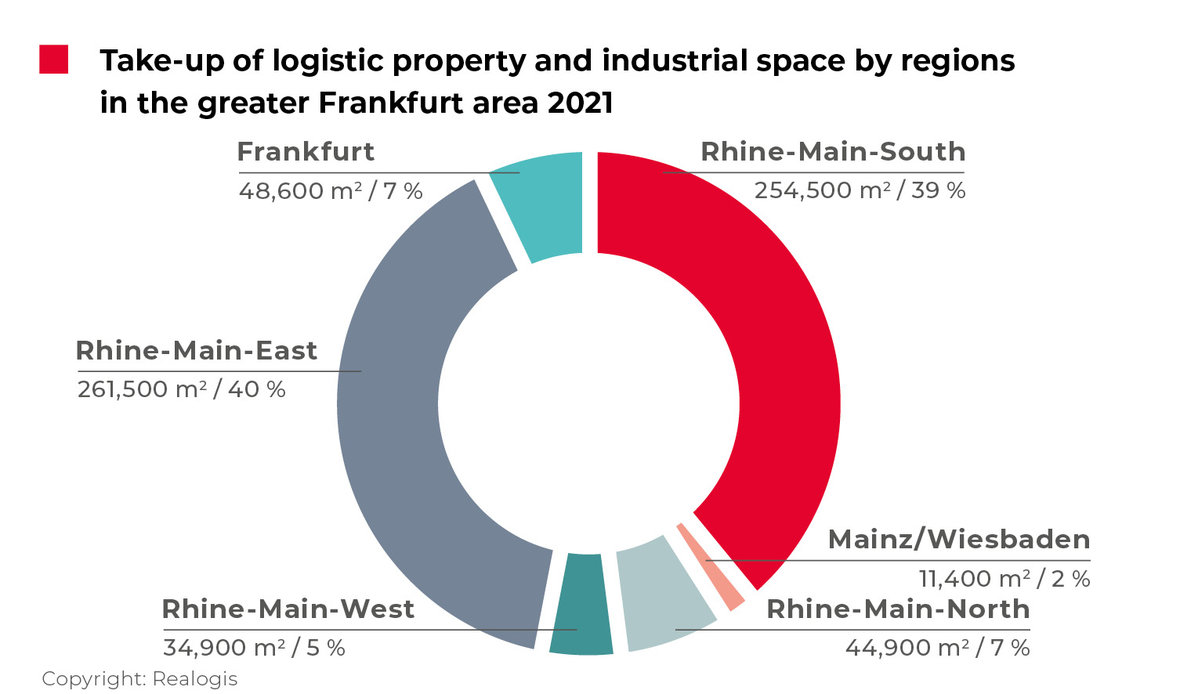

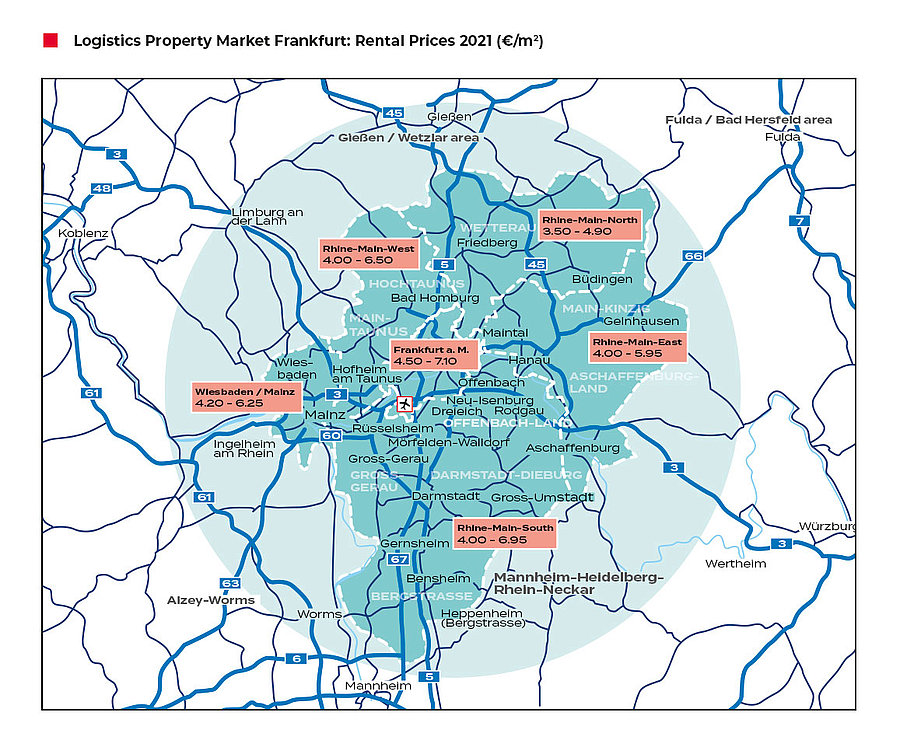

Rhine-Main East sub-market riding high

The biggest region by take-up in 2021 was Rhine-Main East at 261,500 m² or 40%. This region also took the title for fastest rise among all market areas with growth of 9.1 percentage points (2020: 152,200 m² or 30.9%). Four of the top five lessors in terms of take-up – the Hager Group, ID Logistics, PepsiCo Deutschland and B+S – are located here (157,400 m² or 60% of take-up in Rhine-Main East).

Second place goes to last year’s number one, the Rhine-Main South region with 254,500 m² or 38.8%, the biggest faller for take-up in 2021 at 7.9 percentage points (2020: 230,000 m², 46.7%).

The third-biggest region is central Frankfurt with take-up of 48,600 m² or 7.4% of total volume. Central Frankfurt thus more than doubled its absolute take-up and rose by 2.7 percentage points (2020: 23,200 m² or 4.7%).

Rhine-Main North, where the biggest transaction was with DHL for 32,000 m² in Florstadt, accounts for 44,900 m² or 6.8% (up 2.4 percentage points; 2020: 21,800 m² or 4.4%). Rhine-Main West chalked up 34,900 m² or 5.3%, equivalent to a drop of 5.8 percentage points as against the previous year (2020: 54,600 m² or 11.1%). Like last year, last place goes to the Mainz/ Wiesbaden sub-market with 11,400 m² or 1.7% (down 0.4%; 2020: 10,500 m² or 2.1%).

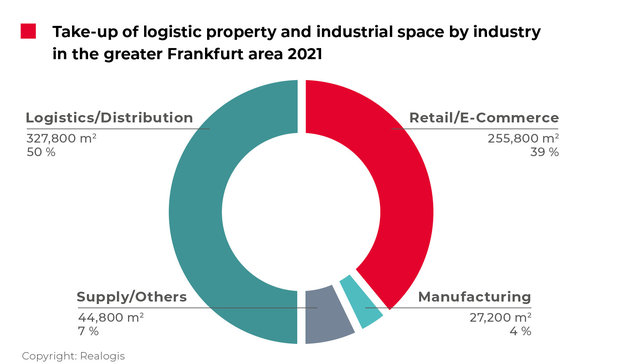

Logistics/ distribution using one in two square metres

Second place in 2020, the logistics/distribution sector accounted for take-up of 327,800 m² or 50% in 2021 – half of all square metres newly occupied. In absolute terms, this sector’s result has virtually tripled and it also had the highest growth in market share at 28.1 percentage points, coming from 21.9% or 108,000 m² in 2020. The sector is the deal leader as well, claiming four of the top five. Together they account for 149,400 m² or 45.6% of the sector’s take-up and make a significant contribution to its good performance.

In second place is retail, down from number one with a share of 39% or 255,800 m². While it improved slightly in absolute figures, retail slipped 8.8 percentage points in significance year-on-year, coming from 47.8% or 235,200 m². This segment landed one of the top deals with 40,000 m² in a new property in Hammersbach (Hager Group).

Retail is followed by the “Miscellaneous” category at 6.8% or 44,800 m² (down 3.5 percentage points; 2020: 51,100 m² or 10.4%) and – the biggest faller from last year – manufacturing, down by 15.7 percentage points from third place (4.2% or 27,300 m²; 2020: 19.9% or 98,000 m²). After accounting for almost one in five square metres in 2020, in 2021 it took only around one in 25 with an absolute slump in take-up of approximately 72%.

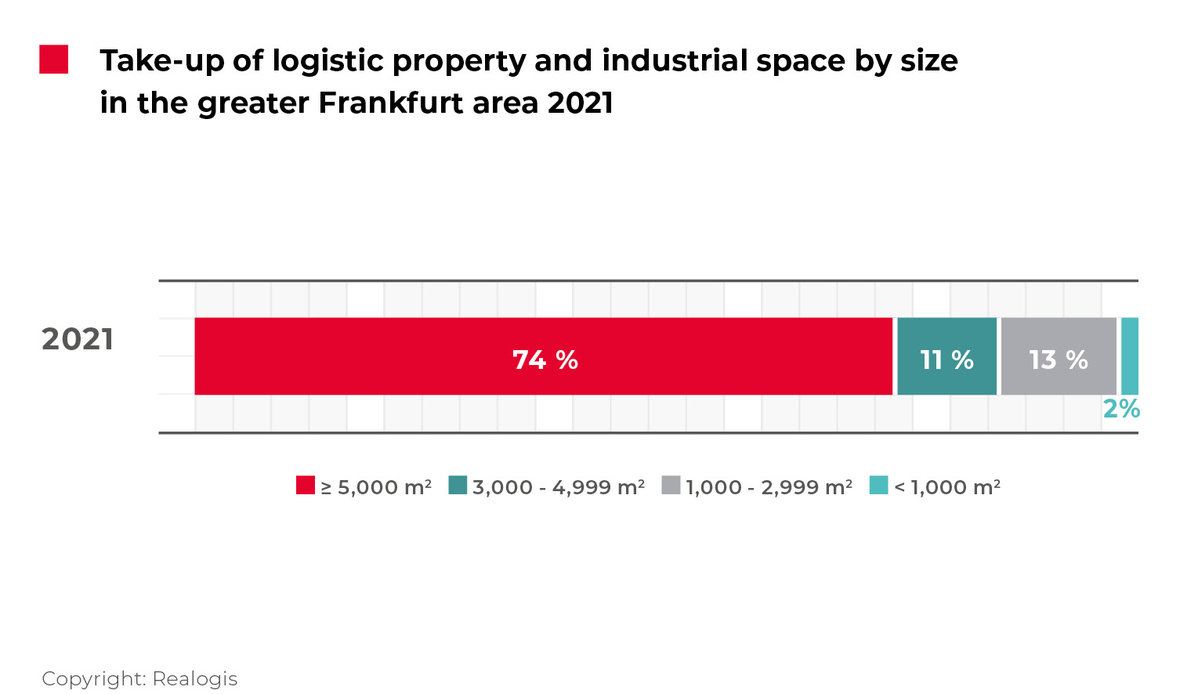

Approximately 75% of all space relates to areas of 5,000 m² and up

The trend towards large areas continued in 2021. Areas of 5,000 m² and up were an easy winner in 2021 with a share of 74.4% or 487,800 m². This category had ranked first in the previous year as well, with a share of 68.9% or 339,400 m², and this year had the highest growth among all size segments (5.5 percentage points). 30 of the 113 deals on record were in this category, including all of the top five transactions, which together contribute 189,400 m² in total (or 38.8% of the take-up in this size class).

This might also be interesting for you:

To the market report Germany

The 3,001 to 5,000 m² group accounted for an area of 70,100 m² or 10.7% in 2021, down 3.4 percentage points year-on-year (2020: 69,300 m² or 14.1%). This category had 18 deals.

The segment between 1,001 and 3,000 m² had the highest number of contracts in 2021 at 45, and took second place with an area of 84,100 m² or 12.8% (down 2.0 percentage points; 2020: 73,200 m² or 14.9%). There were 20 deals for small areas of less than 1,000 m² for a cumulative total of 13,700 m² or 2.1% of all space.

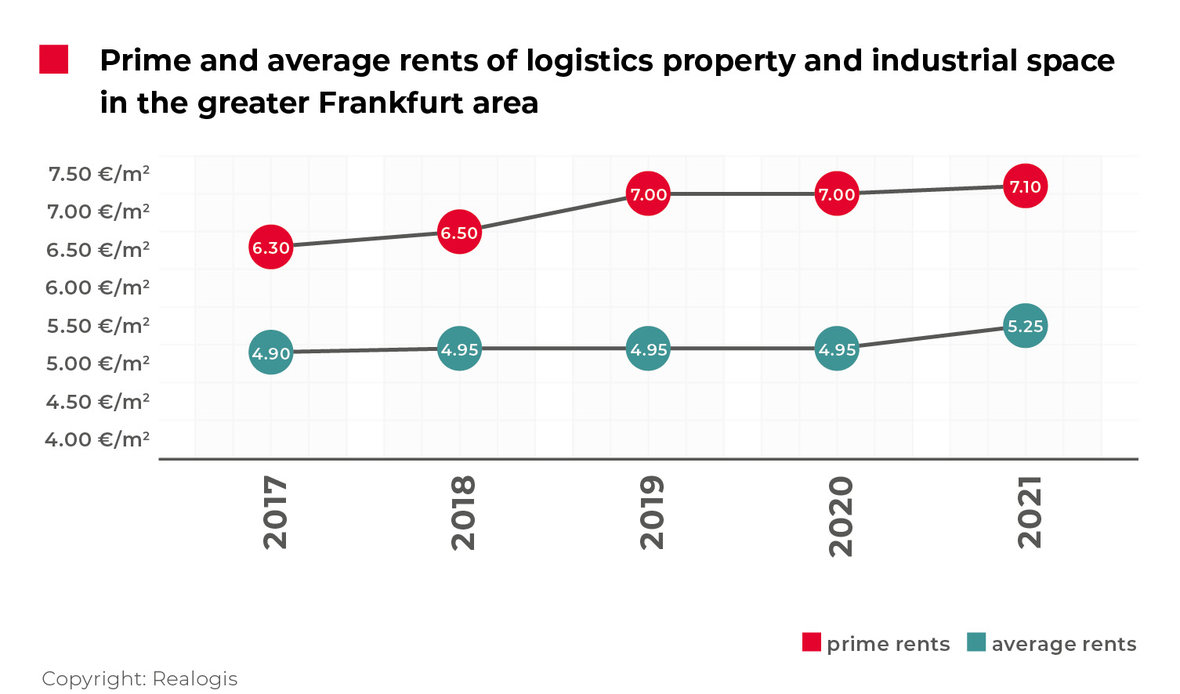

Prime and average rents reach record highs

According to our analysis, prime rents for industrial and logistics properties in the greater Frankfurt/Main area climbed by 1.4% to a provisional high of EUR 7.10/m² in 2021. At the same time, this is 4.7% higher than the five-year average of EUR 6.78/m².

Average rents rose to a new provisional high of EUR 5.25/m². The increase of 6%, up from EUR 4.95/m² in 2020, marks the fastest rise in the past five years.

After virtually matching the five-year average of EUR 4.91/m² in the previous year, average rents are now 5% higher than the five-year average of currently EUR 5.00/m².

Average and prime rents have recently grown closer: At the end of 2020 the gap between prime and average rents in the greater Frankfurt area was still EUR 2.05/m², compared to EUR 1.85/m² at the end of 2021.

Price increases anticipated for sustainable properties in Rhine-Main area

For years now, high-quality logistics properties have mostly been built to DGNB silver or gold standard. With prime rents of EUR 7.50/m², an even higher platinum sustainability certificate would mean another price hike. We assume that tenants will increasingly become interested in sustainable building concepts and that they will therefore become more willing to pay higher rents. Ultimately, this means value added for both sides.

More and more attention is being paid to ESG factors when searching for the right properties. We are mainly seeing this among larger companies and corporations. However, we can well imagine that ESG criteria will play an ever greater role for smaller businesses as well.

To the rent price maps:

Order the complete market report as PDF

Frankfurt - 2021