HOCHWERTIG | 650 m² HALLE | 800 m² AUSSTELLUNG

ID: 998947DetailsGarching, repräsentatives Produktionsgebäude mit hochwertigen Büroflächen

ID: 93135Detailsca. 400 m² große, ebenerdige Lager-Produktionshalle mit Meisterbüro in Top Lage

ID: 1036679DetailsDirekt am Autobahnkreuz Ulm/Elchingen - Neubau multifunktionaler Logistik- und Produktionsflächen

ID: 994300DetailsLOGISTIK | RAMPEN | FREIFLÄCHE

ID: 1008605DetailsLager-/Logistik | Neubau | Rampen | teilbar | ebenerdig

ID: 1016255DetailsGEWERBEPARK | ERSTBEZUG | TOP-LAGE

ID: 996681DetailsBremen, ca. 1.300 m² Lager-/ Logistikfläche zu vermieten

ID: 1032273DetailsMünchen - Nord, Hallen- und Freiflächen in Bestlage zu vermieten

ID: 101077DetailsPROVISIONSFREI | GEWERBEPARK | FLEXIBEL

ID: 1000973DetailsArnsdorf | ca. 9.000 m² | Lager & Logistik | Betonrampe & ebenerdig | teilbar ab 2.000

ID: 1009874DetailsRepräsentativer Gewerbepark

ID: 1005086Detailsca. 1.350 m² große, ebenerdige Hallenfläche mit Büro

ID: 1035432DetailsPRODUKTION | LAGER | RAMPE

ID: 991522DetailsGarching, Neubau von ca. 8.000 m² Lager-,Forschungs- und Bürofläche

ID: 1030576DetailsMunich-North, warehouse and office spaces for rent

ID: 1033335DetailsMunich-North, warehouse and office spaces for rent

ID: 1024609DetailsMunich-North, warehouse and office spaces for rent

ID: 1034331DetailsMunich-North, warehouse and office spaces for rent

ID: 1002692DetailsMunich-North, warehouse and office spaces for rent

ID: 1034768DetailsMunich-North, warehouse and office spaces for rent

ID: 1034670DetailsMunich-North, warehouse and office spaces for rent

ID: 1034767DetailsMunich-North, warehouse and office spaces for rent

ID: 1025539DetailsMunich-North, warehouse and office spaces for rent

ID: 1010949DetailsMunich-North, warehouse and office spaces for rent

ID: 1032598DetailsAugsburg, site with about 2.500 sqm for rent

ID: 9040DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031912DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031769DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031836DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1028145DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030724DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030615DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1023871DetailsGladback, warehousing space for wholesale or retail for rent

ID: 95769DetailsGladback, warehousing space for wholesale or retail for rent

ID: 1013489DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1025426DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1026621DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1022435DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1023380DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1014315DetailsNeuss, approx. 1,295 sqm warehouse space in a business park for rent

ID: 997156DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1017665DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1019585Details

Do you have a question? Leave your contact details here and we will call you back!

Market report Stuttgart year 2021

- About the logistics market in the economic region

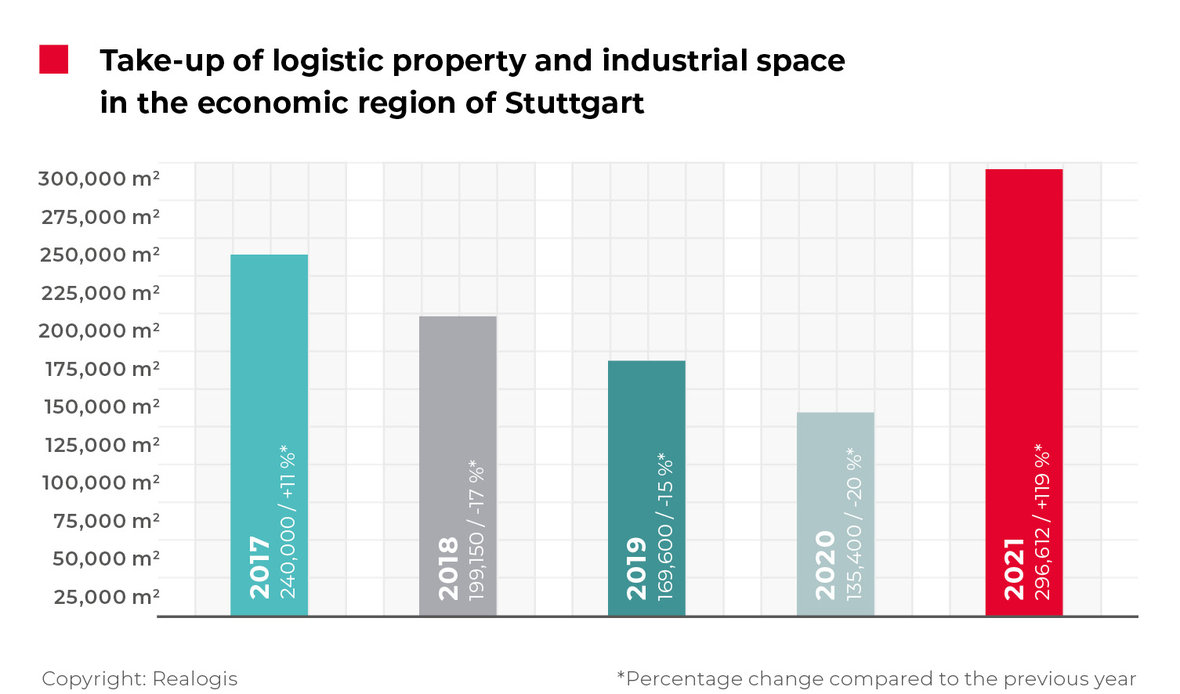

Stuttgart logistics property market doubles take-up in 2021

After three years of declining take-up, the Stuttgart warehouse, logistics and industrial property rental market experienced a significant turnaround by the end of 2021, as we predicted in our half-year market report. The take-up of 296,612 m² achieved by all market participants – a year-on-year increase of 119% – is a new high since records began. The five-year average of 208,152 m² was exceeded by a significant 42% following three years in a row of underperformance.

Thus the previous year’s take-up by all market participants has been more than doubled. With rental take-up of approximately 300,000 square metres, new leases have been signed for almost as much space as in 2019 and 2020 combined.

The volume of take-up in 2021 is mainly due to two factors: Firstly, we have been seeing something of a turnaround in the automotive sector for several years. Production demand was muted in 2019 and 2020 but picked up considerably in 2021. There was also a general restraint because of COVID. But now a lot’s happening again on the market.

Facts

Take-up of rental space rises by 119% to just under 300,000 m²

Up 42% on five-year average

Existing properties account for 84% of all new rentals

Ludwigsburg takes highest market share, Böblingen strongest growth

Logistics/ distribution claim half of all square metres

Areas over 5,000 m² account for two thirds of all take-up

Prime rent rises to highest level to date of EUR 7.00/m²

Forecast 2022: Less available space than ever

Investment market: handful of standalone deal

We expect the demand situation to remain positive in 2022, though with less space available than ever before. 2021 was an exceptional year that more than compensated for 2019 and 2020. While we expect that more new buildings will be developed again in 2022 than in the previous year, they will not be able to satisfy demand by a long way.

Existing properties account for 84% of all new rentals

In total, we recorded 68 deals by all market participants in 2021. The highest share of the current record result – as in the previous year – went to existing properties at 84% or 250,368 m² (2020: 94% or 127,300 m²). Existing space thus almost doubled its absolute take-up compared to the previous year. New properties accounted for 14% or 41,744 m² in 2021 (2020: 6% or 8,100 m²); brownfield sites were barely relevant at 2% or 4,500 m².

Lessors with highest take-up

Porsche, Ludwigsburg, approx. 23,000 m² (New build), Manufacturing

Yahee GmbH, Ludwigsburg, approx. 20,804 m² (Existing property), Retail

HTL, Ludwigsburg, approx. 15,000 m² (Existing property), Logistics/ distribution

Krannich, Böblingen, approx. 15,000 m² (Existing property), Logistics/ distribution

Of the top four lessors with highest take-up, three went for existing properties. These are Yahee in Ludwigsburg at 20,804 m², HTL in Ludwigsburg at 15,000 m² and Krannich in Böblingen at 15,000 m².

The biggest deal in the past year was by Porsche in Ludwigsburg for an area of 23,000 m², though this was the only major take-up in the new build category. It is also the biggest deal for the whole of the period under review and accounts for more than half of new-build take-up (55%).

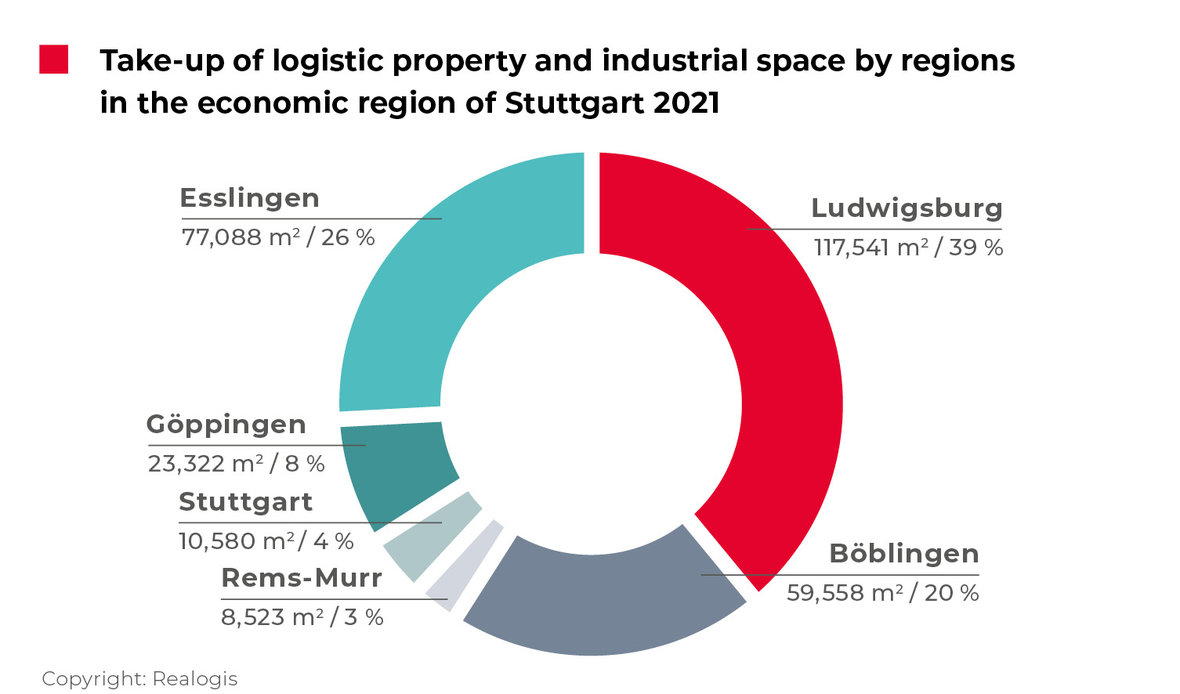

Ludwigsburg takes highest market share, Böblingen strongest growth

The Ludwigsburg district claims the highest market share at 39.6% or 117,541 m². Coming first again as it did in the previous year (2020: 53,000 m² or 39.1%), the region added little in the way of market share at just 0.5 percentage points but more than doubled its area. Three of the four biggest new leases (Porsche, Yahee and HTL) were in this region and contribute around half of its take-up at 50% or 58,804 m².

In second place is the Esslingen region once again with 77,088 m² or 26% (2020: 38,300 m² or 28.3%). It lost 2.3 percentage points of market share, though the absolute take-up in Esslingen more than doubled as well. Third place goes to Böblingen at 59,558 m² or 20.1%. Having ranked last but one in 2020 at 10,400 m² or 7.7%, Böblingen gained the most market share out of all regions at 12.4 percentage points, not to mention the highest absolute growth of all regions at 473%. Its robust result was helped by one of the top deals (Krannich), which accounts for 25% of take-up in this region.

This is followed by the Göppingen district at 23,322 m² or 7.8% (2020: 0 m²), central Stuttgart at 10,580 m² or 3.6% (2020: 17,400 m² or 12.9%, down 9.3 percentage points) and the Rems-Murr district at 8,523 m² or 2.9%. Last year’s number four, the Rems-Murr district had the second-most significant decline in market share after central Stuttgart at 9.2 percentage points (coming from 16,300 m² or 12%, thus halving its standing).

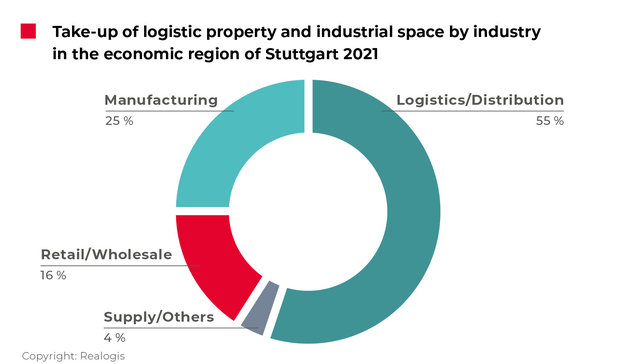

Logistics/ distribution claim half of all square metres

The leading sector since 2015, logistics/ distribution took gold again in 2021 at 162,847 m² or 54.9%, which means it claimed more than half of all square metres taken up. It gained 8.9 percentage points of market share on the previous year, coming from 46% or 62,300 m². Two of the top leases were in this sector (HTL and Krannich), covering 18% of the take-up in this sector.

As in the previous year, second place goes to the manufacturing sector at 73,542 m² or 24.8% (2020: 37,900 m² or 28%; down 3,2 percentage points), 31% of which thanks to the Porsche deal. Third place, again like last year, goes to retail at 46,843 m² or 15.8% (2020: 18% or 24,400 m², up 2.2 percentage points).

The miscellaneous category “Other” again brought up the rear with 13,380 m² or 4.5% (2020: 10,800 m² or 8.0%, down 3.5 percentage points).

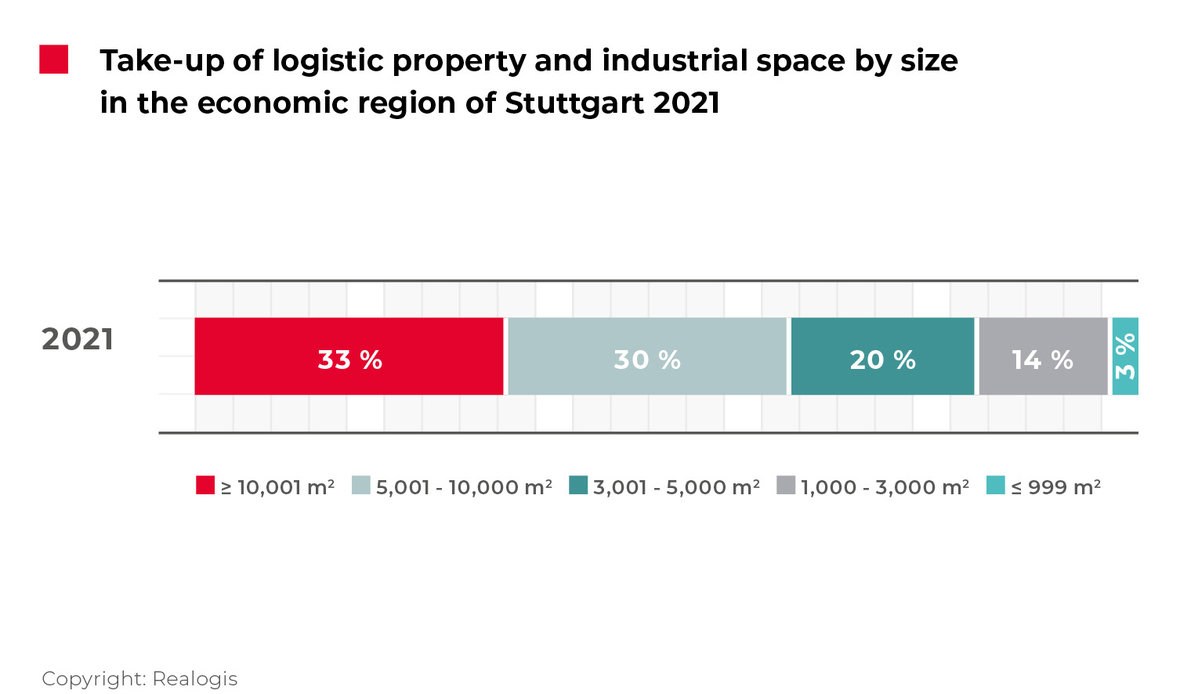

Areas over 5,000 m² account for two thirds of all take-up

As in the previous year, the biggest take-up was contributed by areas of 10,000 m² or more, which accounted for 33.1% or 98,191 m². However, out of all size classes, this one lost the most relative significance at 9.2 percentage points (coming from a share of 42.3% or 57,300 m²). Five of the 68 deals are in this category.

The 5,001 to 10,000 m² category accounted for a share of 30.1% or take-up of 89,291 m², improving its 2020 performance by 8.9 percentage points (21.2% or 28,700 m²). Of all deals 12 were for the account of this segment.

This might also be interesting for you:

To the market report Germany

At 9.5 percentage points, the 3,001 to 5,000 m² size category had the clearest rise in relative significance (2021: 20.4% or 60,507 m²; 2020: 10.9% or 14,700 m²). This result was thanks to 15 of the 68 deals.

In total, 23 leases for areas from 1,001 to 3,000 m² account for a share of 13.5% or 40,083 m² (2020: 18.3% or 24,800 m², down 4.8 percentage points) and 13 leases for the smallest spaces of less than 1,000 m² for 2.9% or 8,540 m² (2020: 7.3% or 9,900 m², down 4.4 percentage points).

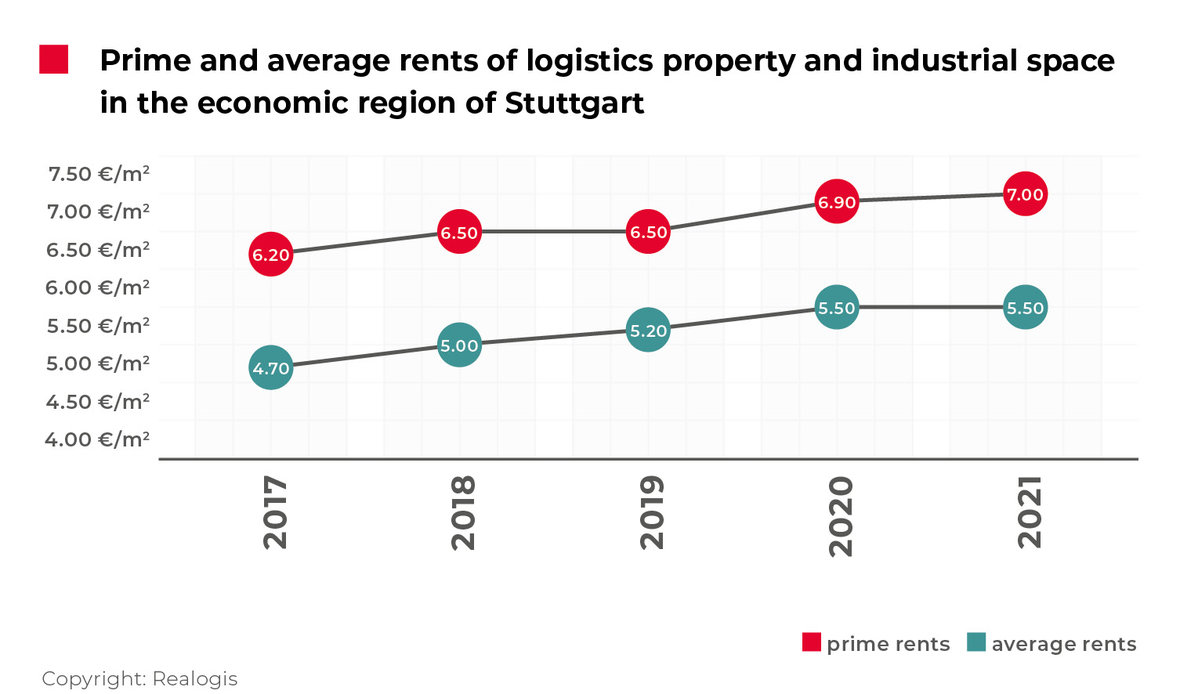

Prime rent rises to highest level to date of EUR 7.00/m²

The rising trend in prime rents for logistics properties over the past five years (since 2017) is continuing, with the exception of 2019, though with only marginal appreciation of 1% to the high to date of EUR 7.00/m². 2020 had the most significant increase in the past five years at 6% to EUR 6.90/m². The five-year average of EUR 6.62/m² is now being exceeded by 6%.

Average rents for logistics properties tend to follow the same pattern as prime rents. However, they were flat at the end of 2021 at the high to date of EUR 5.50/m², which was achieved in 2020. The five-year average of EUR 5.18/m² was exceeded by 6% in 2021.

The absolute price gap between average and prime rents has remained largely the same in recent years (difference of around EUR 1.50/m² in the respective years). Prime and average rents are therefore not drifting apart but rather moving in parallel.

Investment market

Stuttgart is still one of the most interesting investment markets for warehouse, logistics and industrial properties in Germany. Private and institutional investors are still keen to acquire properties in the greater Stuttgart area – but there continue to be hardly any investment opportunities at present – including either undeveloped land or existing properties.

The seller structure in the Stuttgart region is still dominated by regional private investors and many former entrepreneurs who are having difficulty in disposing of properties – because of the lack of alternative investment options on the finance market and corresponding bank fees for cash assets – even if the high purchase price level would often justify it. In 2021, there was thus only a handful of individual deals in these asset classes again. Investment opportunities are lucky finds. This situation will presumably continue for as long as the financial market is stuck in a phase of zero or negative interest rates.

However, we anticipate that owners have changes and investment headed their way in the area of the energy renovation of older existing properties. Reflecting the future ESG factors of the 2030 agenda, it is becoming increasingly important for users’ properties to become more sustainable. This can include modern utilisation situations, charging stations for electric vehicles, LED lighting and photovoltaic systems. Well-being factors for employees could also become more important as the tense situation on the labour market makes it harder and harder to find staff. We are therefore anticipating a lot of changes to come in the property sector.

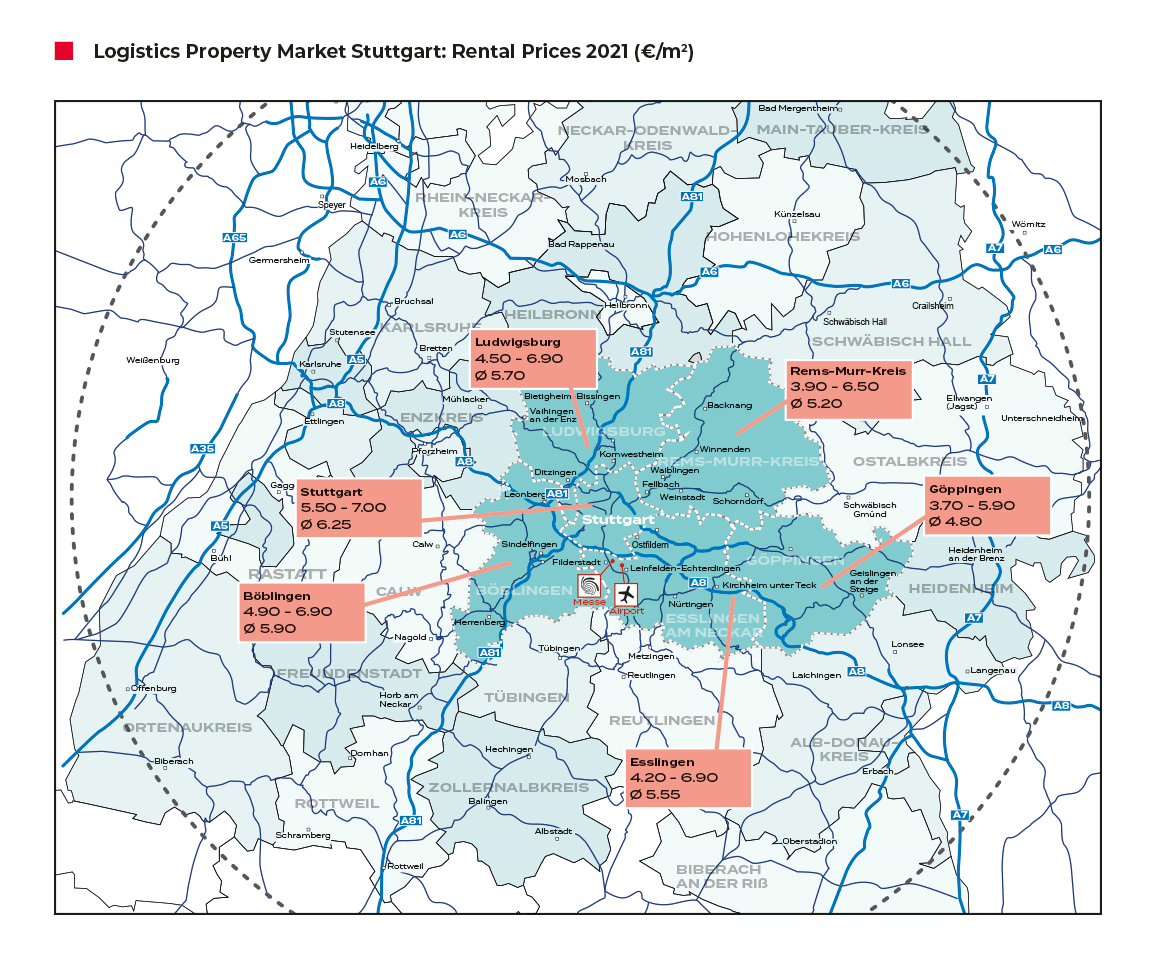

To the rent price maps:

Order the complete market report as PDF

Stuttgart - 2021