HOCHWERTIG | 650 m² HALLE | 800 m² AUSSTELLUNG

ID: 998947DetailsGarching, repräsentatives Produktionsgebäude mit hochwertigen Büroflächen

ID: 93135Detailsca. 400 m² große, ebenerdige Lager-Produktionshalle mit Meisterbüro in Top Lage

ID: 1036679DetailsDirekt am Autobahnkreuz Ulm/Elchingen - Neubau multifunktionaler Logistik- und Produktionsflächen

ID: 994300DetailsLOGISTIK | RAMPEN | FREIFLÄCHE

ID: 1008605DetailsLager-/Logistik | Neubau | Rampen | teilbar | ebenerdig

ID: 1016255DetailsGEWERBEPARK | ERSTBEZUG | TOP-LAGE

ID: 996681DetailsBremen, ca. 1.300 m² Lager-/ Logistikfläche zu vermieten

ID: 1032273DetailsMünchen - Nord, Hallen- und Freiflächen in Bestlage zu vermieten

ID: 101077DetailsPROVISIONSFREI | GEWERBEPARK | FLEXIBEL

ID: 1000973DetailsArnsdorf | ca. 9.000 m² | Lager & Logistik | Betonrampe & ebenerdig | teilbar ab 2.000

ID: 1009874DetailsRepräsentativer Gewerbepark

ID: 1005086Detailsca. 1.350 m² große, ebenerdige Hallenfläche mit Büro

ID: 1035432DetailsPRODUKTION | LAGER | RAMPE

ID: 991522DetailsHochwertige Hallenfläche | ebenerdig | Neubau

ID: 1028652DetailsGarching, Neubau von ca. 8.000 m² Lager-,Forschungs- und Bürofläche

ID: 1030576DetailsMunich-North, warehouse and office spaces for rent

ID: 1033335DetailsMunich-North, warehouse and office spaces for rent

ID: 1024609DetailsMunich-North, warehouse and office spaces for rent

ID: 1034331DetailsMunich-North, warehouse and office spaces for rent

ID: 1002692DetailsMunich-North, warehouse and office spaces for rent

ID: 1034768DetailsMunich-North, warehouse and office spaces for rent

ID: 1034670DetailsMunich-North, warehouse and office spaces for rent

ID: 1034767DetailsMunich-North, warehouse and office spaces for rent

ID: 1025539DetailsMunich-North, warehouse and office spaces for rent

ID: 1010949DetailsMunich-North, warehouse and office spaces for rent

ID: 1032598DetailsAugsburg, site with about 2.500 sqm for rent

ID: 9040DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031912DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031769DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031836DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1028145DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030724DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030615DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1023871DetailsGladback, warehousing space for wholesale or retail for rent

ID: 95769DetailsGladback, warehousing space for wholesale or retail for rent

ID: 1013489DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1025426DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1026621DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1022435DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1023380DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1014315DetailsNeuss, approx. 1,295 sqm warehouse space in a business park for rent

ID: 997156DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1017665DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1019585Details

Do you have a question? Leave your contact details here and we will call you back!

Market report Munich for the year 2021

- About the logistics market in the economic region

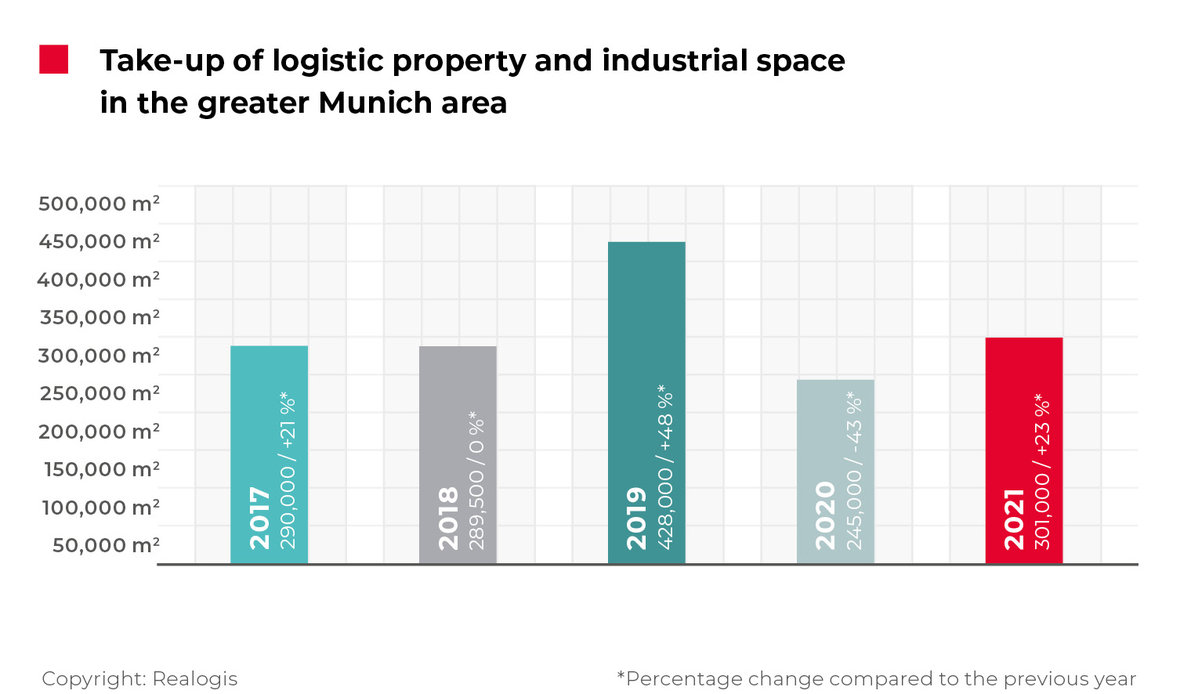

Munich logistics property market breaks past 300,000 mark again

The Munich market for logistics, warehousing and industrial space increased its rental take-up by 22.9% in 2021 to 301,000 m² of newly used space by all market participants combined in the period from January to December 2021. Thus, the Munich industrial and logistics property market has broken past the 300,000 mark again. At the same time, this is the second-best result in the past five years. The current five-year average of 310,700 m² could not quite be reached again yet.

Overall we registered 110 deals by retail companies, manufacturers, logistics specialists and other market participants in the Greater Munich area over the past twelve months, 25 more than in the previous year.

Take-up in the Greater Munich area is dominated by larger spaces. At 157,600 m², more than one in every two square metres taken up was in units of 5,000 m² or more.

Facts

- Take-up moved up by 22.9% year-on-year

- More than three quarters and five of the top seven deals attributable to existing space

- North region still in the lead

- Logistics/ distribution sector accounts for almost a third of all transactions

- Large spaces see high increase in relative share

- Prime rent and average rent remain at highest level to date

- Trend: Five speculative new building projects with around 80,000 m² started

More than three quarters of deals attributable to existing space

Existing space in particular contributed to the strong result. It accounted for 232,100 m² or 77.1% of total take-up (a year-on-year increase of 31.1% in absolute terms).

Five of the top seven deals last year were in existing properties and represented 22% of total take-up at 66,100 m². The biggest lease on the market, at 24,000 m², was concluded by a government authority in an existing property in Kirchheim.

Lessors with the highest take-up in FY 2021

Government authority, Kirchheim (East Munich), approx. 24,000 m² (Existing property), Others

KP Family / Babyartikel.de, Reichertshofen (North Munich), approx. 12,500 m² (New build), e-commerce

Rudolph Logistik, Langenbruck (North Munich), approx. 12,000 m² (New build), Logistics

Government agency, Neufahrn (North Munich), approx. 11,000 m² (Existing property), Others

BTK, Parsdorf (East Munich), approx. 10,400 m² (Existing property), Warehouse

UPS, Kirchheim (East Munich), approx. 10,400 m² (Existing property), Logistics

Dachser SE, Neufahrn (North Munich), approx. 10,300 m² (Existing property), Logistics

New builds accounted for 55,000 m² or 18.3% (a year-on-year increase of 5.8%). Major leases were concluded by KP Family / Babyartikel.de in Reichertshofen at 12,500 m² and by Rudolph Logistik in Langenbruck at 12,000 m².

Brownfield sites contributed 13,900 m² or 4.6% (down 13.1% year-on-year).

Almost 80,000 m² of speculative space under development by 2022-2023

In 2021, construction work began for five project developments. Almost 80,000 m² of speculative space is thus to come onto the market this year and next year. The biggest projects include “Unternehmer Park” by Aurelis at 31,400 m² and “Giesserei” by Beos at 22,000 m². In Kirchheim, the project developer Panattoni is applying its successful “City Dock” concept in Bavaria for the first time.

Project developments started in FY 2021

Unternehmer Park by Aurelis, approx. 31,400 m² (speculative), Expected completion around Q2 2023

Giesserei by Beos, approx. 22,000 m² (speculative), Expected completion around Q1 2023

City Dock Kirchheim by Panattoni, approx. 13,300 m² (speculative), Expected completion around Q1 2023

Technologie Park by Aurelis, approx. 9,270 m² (speculative), Expected completion around Q3 2022

multimini Kirchheim by MB Park Deutschland, approx. 3,500 m² (speculative), Expected completion around Q4 2022

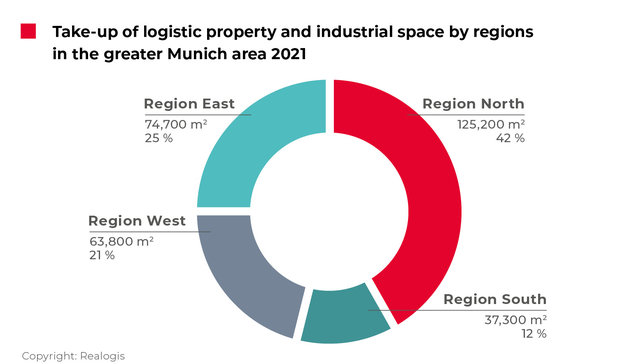

North region still in first place

As in the previous year, Munich North was the leading region with 125,200 m² or 41.6% (2020: 101,000 m² or 41.2%). Four of the top seven deals last year were in this region (45,800 m² or 15.2% of total take-up). In addition to KP Family/ Babyartikel.de in Reichertshofen and Rudolph Logistik in Langenbruck, a government agency in Neufahrn and Dachser SE also chose North Munich.

In second place was the East region, which marked the biggest increase out of all sub-markets with take-up of 74,700 m² or 24.8% (2020: 32,000 m² or 13.1%; relative growth: +11.8 percentage points). It contributed three of the top seven deals, including the biggest lease concluded in the year as a whole by a government agency in Kirchheim. Units measuring 10,400 m² were chosen both by the logistics service provider BTK Befrachtungs- und Transportkontor in Parsdorf and by the global parcel and logistics company UPS in Kirchheim-Heimstetten, which is expanding its floor space locally in an existing property.

The regions with the next highest take-up were the West region with 63,800 m² or 21.2% (2020: 53,000 or 21.6%; absolute growth: +20.4%) and the South region with 37,300 m² or 12.4% (2020: 59,000 m² or 24.1%), which saw the biggest relative decline out of all regions at 11.7 percentage points and was the only region to record an absolute decrease in take-up (-36.8%).

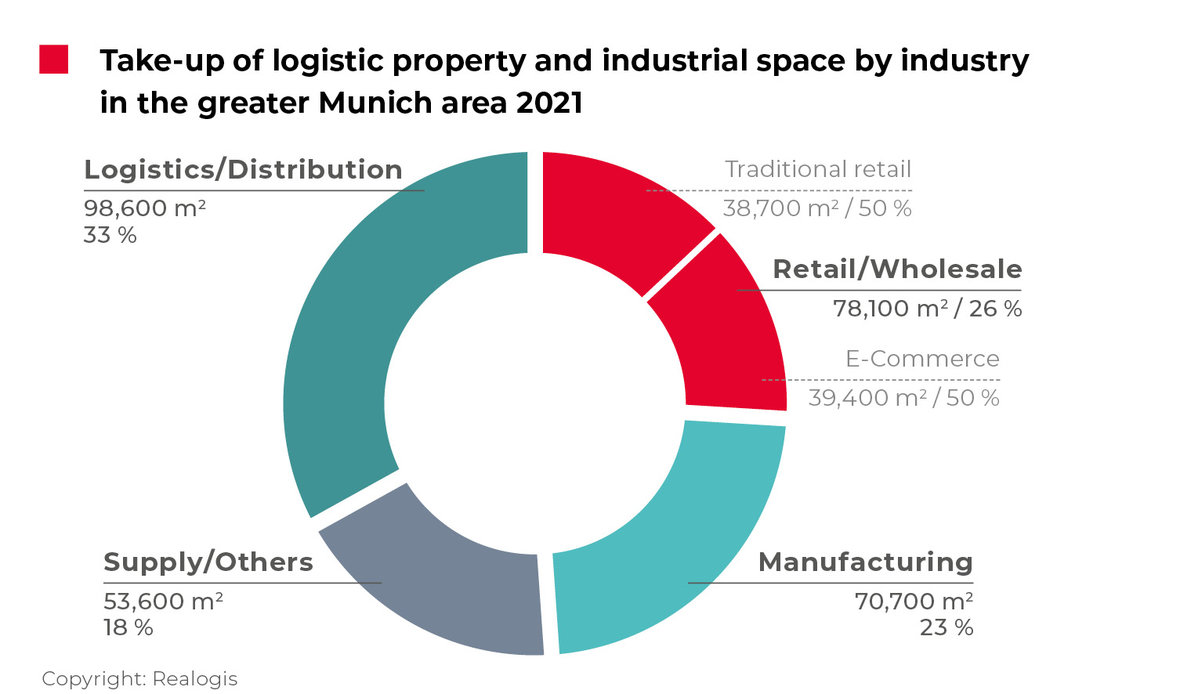

Logistics/ distribution sector accounts for almost a third of all transactions

Comparing the sectors by take-up, logistics/ distribution is in the lead again with 98,600 m² or 32.8% (2020: 90,000 m² or 36.7%). However, the sector saw a decrease of 4 percentage points as against the previous year. 37 of the total 110 transactions were attributable to this segment.

This might also be interesting for you:

To the market report Germany

In second place is retail with a share of 25.9% or 78,100 m² (2020: 30.2% or 74,000 m²). The sub-categories of traditional retail (49.6% or 38,700 m²) and e-commerce (50.4% or 39,400 m²) were almost level pegging in 2021. According to Realogis, retail companies concluded 34 of the total 110 leases, with 26 attributable to traditional retail and eight to e-commerce.

In third place is the manufacturing sector with a share of 23.5% or 70,700 m² of total take-up (2020: 32.2% or 79,000 m²). It saw the largest decline in its relative share at 8.8 percentage points and was the only sector to record an absolute decrease in take-up (-10.5%). 23 of the 110 deals were recorded in this category.

Last place was taken by the miscellaneous category “Other” with a share of 17.8% or 53,600 m². As a result of two unusually large leases for warehouse space for government authorities, it saw the biggest gain in market share out of all sectors at 17 percentage points (as compared to 0.8% or 2,000 m²) and multiplied its take-up by a factor of 27 in absolute terms. 16 of the 110 deals – 14 more than in the previous year – were attributable to this segment.

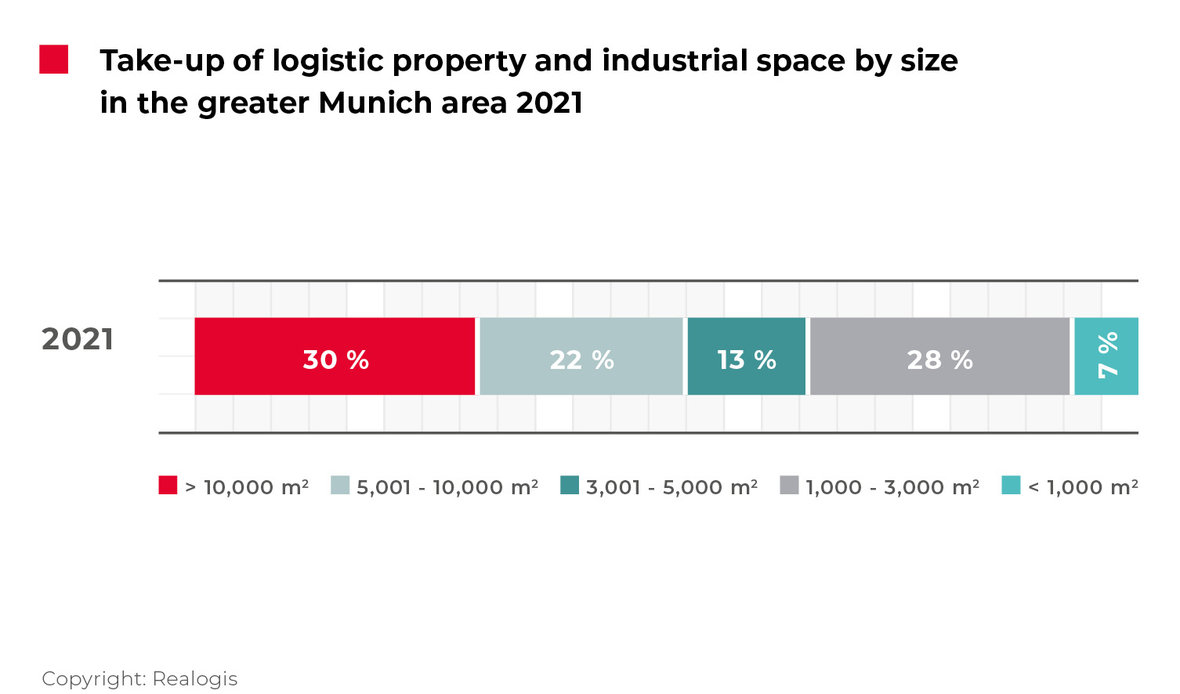

Large spaces see high increase in relative share

With accumulated take-up of 90,600 m² or 30.1%, spaces measuring 10,000 m² or more contributed the largest share out of all segments in 2021 as a whole. This result represents a large increase in their relative importance, as they had been in second-to-last place in the previous year. Large spaces thus marked an increase of 20.6 percentage points (2020: 23,200 m² or 9.5%) and almost quadrupled their absolute take-up. All of the top seven deals were in this category and also accounted for the entire result in this size segment.

Spaces between 5,000 and 9,999 m² accounted for 11 of the new leases and took third place with 67,000 m² or 22.3% (2020: 35.6% or 87,300 m²; down 13.4 percentage points).

Medium-sized spaces between 3,000 and 4,999 m² saw 11 deals and were responsible for a share of 13.3% or 39,900 m², putting them in fourth place. Coming from second place, they lost the most ground in relative terms out of all size categories with a decline of 14.3 percentage points (2020: 67,500 m² or 27.6%; they also decreased significantly by 40% in absolute terms).

Smaller spaces between 1,000 and 2,999 m² reached a share of 27.4% or 82,400 m² with 48 leases. The smallest spaces of less than 1,000 m² are in last place again with a share of 7% or 21,100 m² (2020: 6% or 16,100 m²). However, the second-highest number of deals – 33 out of 110 – relate to this category.

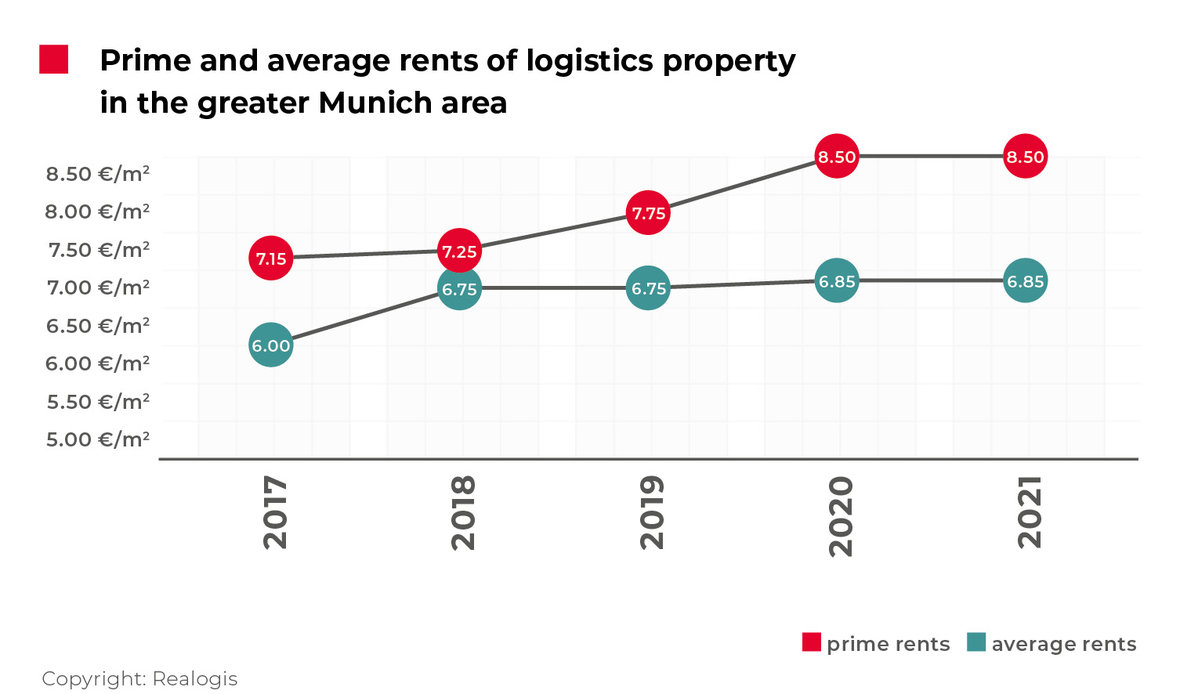

Prime rent and average rent remain at highest level to date

Prime rent remained at its high to date from the previous year of EUR 8.50/m², thus exceeding the five-year average of EUR 7.83/m² by 8.6%. Looking at the past five years, it rose in four out of the five, most recently by 9.7% from EUR 7.75/m² in 2020, which represented the highest year-on-year increase.

Average rent also did not change from the previous year’s level, remaining at its high to date of EUR 6.85/m² but only exceeding the five-year average (EUR 6.64/m²) by 3.2%. Its biggest year-on-year increase was recorded in 2018, when it rose 12.5% to EUR 6.75/m².

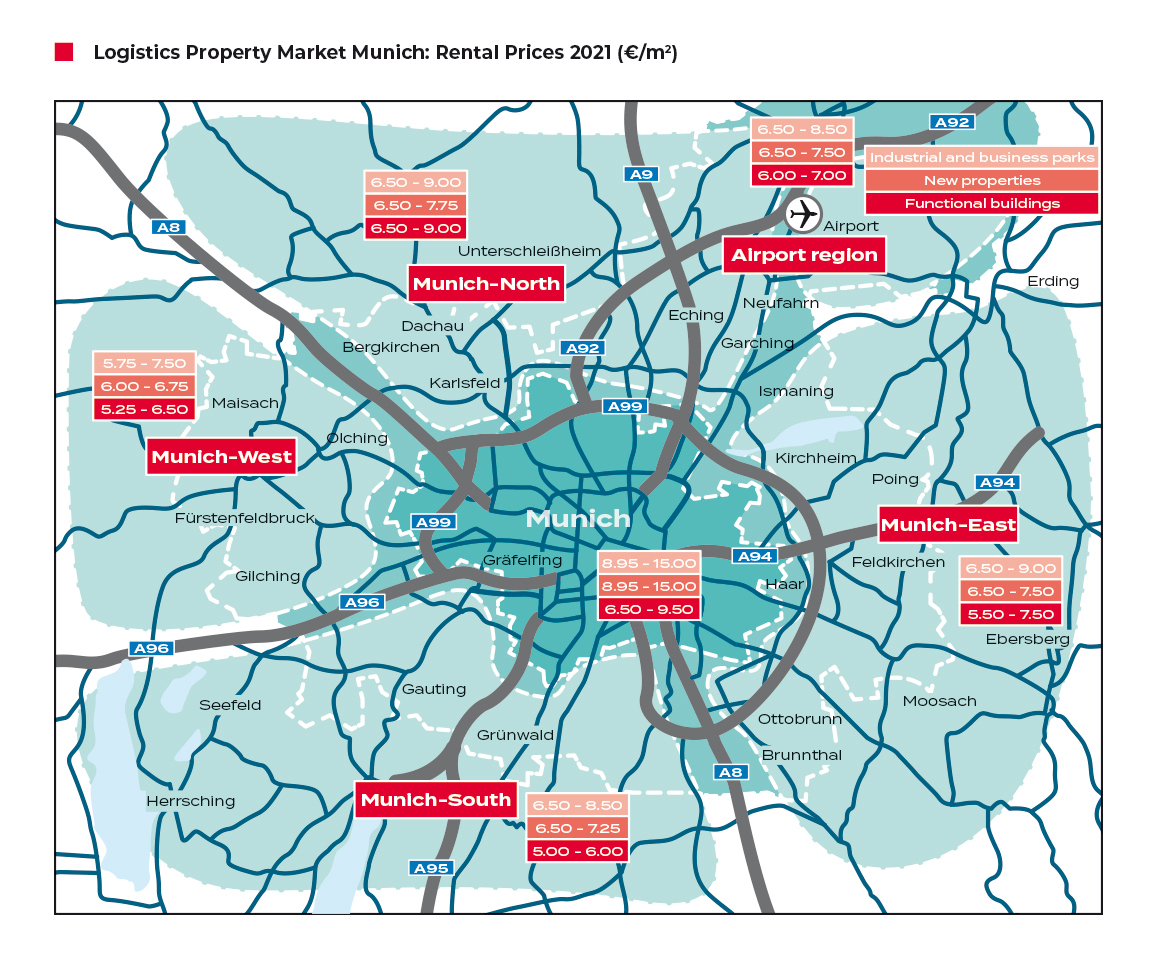

To the rent price maps:

Order the complete market report as PDF

Munich - 2021