HOCHWERTIG | 650 m² HALLE | 800 m² AUSSTELLUNG

ID: 998947DetailsGarching, repräsentatives Produktionsgebäude mit hochwertigen Büroflächen

ID: 93135Detailsca. 400 m² große, ebenerdige Lager-Produktionshalle mit Meisterbüro in Top Lage

ID: 1036679DetailsDirekt am Autobahnkreuz Ulm/Elchingen - Neubau multifunktionaler Logistik- und Produktionsflächen

ID: 994300DetailsLOGISTIK | RAMPEN | FREIFLÄCHE

ID: 1008605DetailsLager-/Logistik | Neubau | Rampen | teilbar | ebenerdig

ID: 1016255DetailsGEWERBEPARK | ERSTBEZUG | TOP-LAGE

ID: 996681DetailsBremen, ca. 1.300 m² Lager-/ Logistikfläche zu vermieten

ID: 1032273DetailsMünchen - Nord, Hallen- und Freiflächen in Bestlage zu vermieten

ID: 101077DetailsPROVISIONSFREI | GEWERBEPARK | FLEXIBEL

ID: 1000973DetailsArnsdorf | ca. 9.000 m² | Lager & Logistik | Betonrampe & ebenerdig | teilbar ab 2.000

ID: 1009874DetailsRepräsentativer Gewerbepark

ID: 1005086Detailsca. 1.350 m² große, ebenerdige Hallenfläche mit Büro

ID: 1035432DetailsPRODUKTION | LAGER | RAMPE

ID: 991522DetailsHochwertige Hallenfläche | ebenerdig | Neubau

ID: 1028652DetailsGarching, Neubau von ca. 8.000 m² Lager-,Forschungs- und Bürofläche

ID: 1030576DetailsMunich-North, warehouse and office spaces for rent

ID: 1033335DetailsMunich-North, warehouse and office spaces for rent

ID: 1024609DetailsMunich-North, warehouse and office spaces for rent

ID: 1034331DetailsMunich-North, warehouse and office spaces for rent

ID: 1002692DetailsMunich-North, warehouse and office spaces for rent

ID: 1034768DetailsMunich-North, warehouse and office spaces for rent

ID: 1034670DetailsMunich-North, warehouse and office spaces for rent

ID: 1034767DetailsMunich-North, warehouse and office spaces for rent

ID: 1025539DetailsMunich-North, warehouse and office spaces for rent

ID: 1010949DetailsMunich-North, warehouse and office spaces for rent

ID: 1032598DetailsAugsburg, site with about 2.500 sqm for rent

ID: 9040DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031912DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031769DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1031836DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1028145DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030724DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1030615DetailsAugsburg, site with about 2.500 sqm for rent

ID: 1023871DetailsGladback, warehousing space for wholesale or retail for rent

ID: 95769DetailsGladback, warehousing space for wholesale or retail for rent

ID: 1013489DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1025426DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1026621DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1022435DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1023380DetailsDüsseldorf Stadtmitte | ca. 462 m² Lagerfläche | Büro | ebenerdig

ID: 1014315DetailsNeuss, approx. 1,295 sqm warehouse space in a business park for rent

ID: 997156DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1017665DetailsBERLIN-FRIEDRICHSHAIN | ca. 1.560 m² | EXKLUSIVE MIETFLÄCHE IM ZENTRUM

ID: 1019585Details

Do you have a question? Leave your contact details here and we will call you back!

Market report Hamburg year 2021

- About the logistics market in the economic region

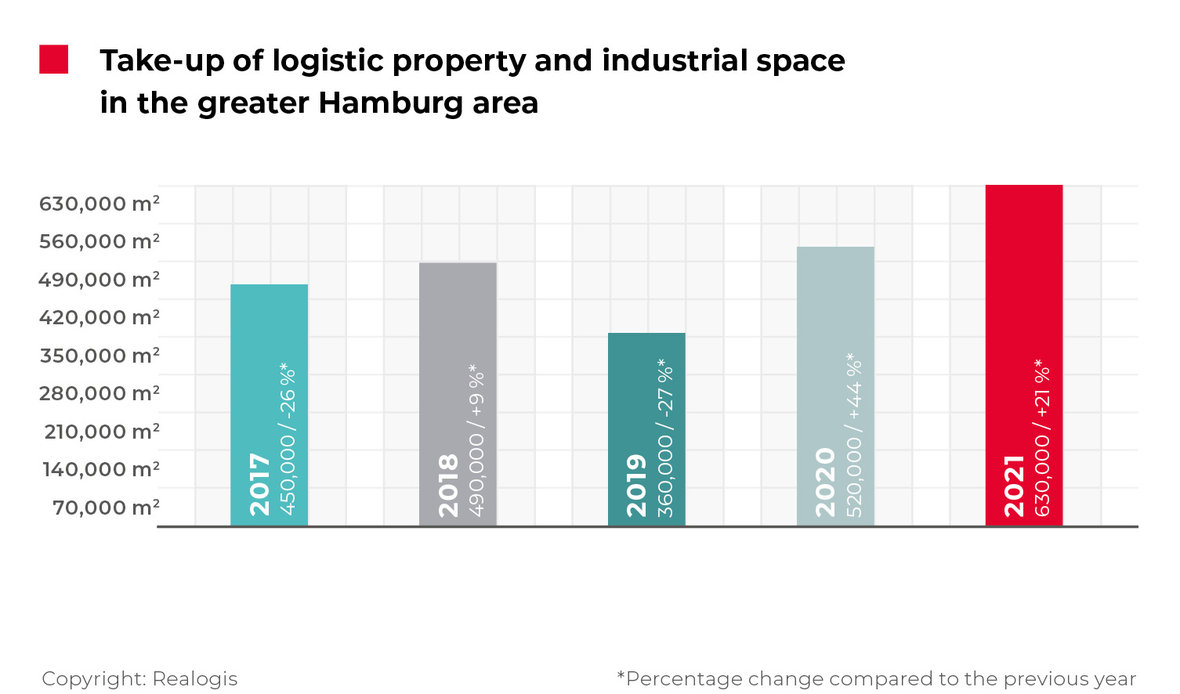

Hamburg logistics property market beats record take-up

With a volume of 630,000 m² generated by all market participants, the Hamburg market for rental and owner-occupied warehouse, logistics and industrial space broke the previous record set in 2016 (610,000 m²). Take-up increased by 21.2% year-on-year (2020: 520,000 m²) and beat the five-year average of 490,000 m² by an impressive 29%.

The top five deals in 2021 alone contributed 131,500 m² or 20% to total take-up in Hamburg. The biggest lease was signed by the retail company Riess Ambiente for a 40,000 m² new build in the region to the north of the city. This was followed by the logistics company Greiwing logistics for you with a 28,000 m² existing property in the Port of Hamburg and Group7 with a 26,000 m² owner-occupied new build in the east of the city. The biggest deals also included a 20,000 m² existing property (retail) in the region to the south of the city for the retail company LFW and a 17,500 m² existing property in the region to the south of the city for the logistics company Ernst Pfaff.

Facts

Take-up rises by 21.2% to 630,000 m²

Southern Hamburg metropolitan area with two major deals

Logistics/ distribution sector doubles take-up

Still almost no space with high suitability for third-party use and new-build quality available in the size category of 5,000 m² and larger

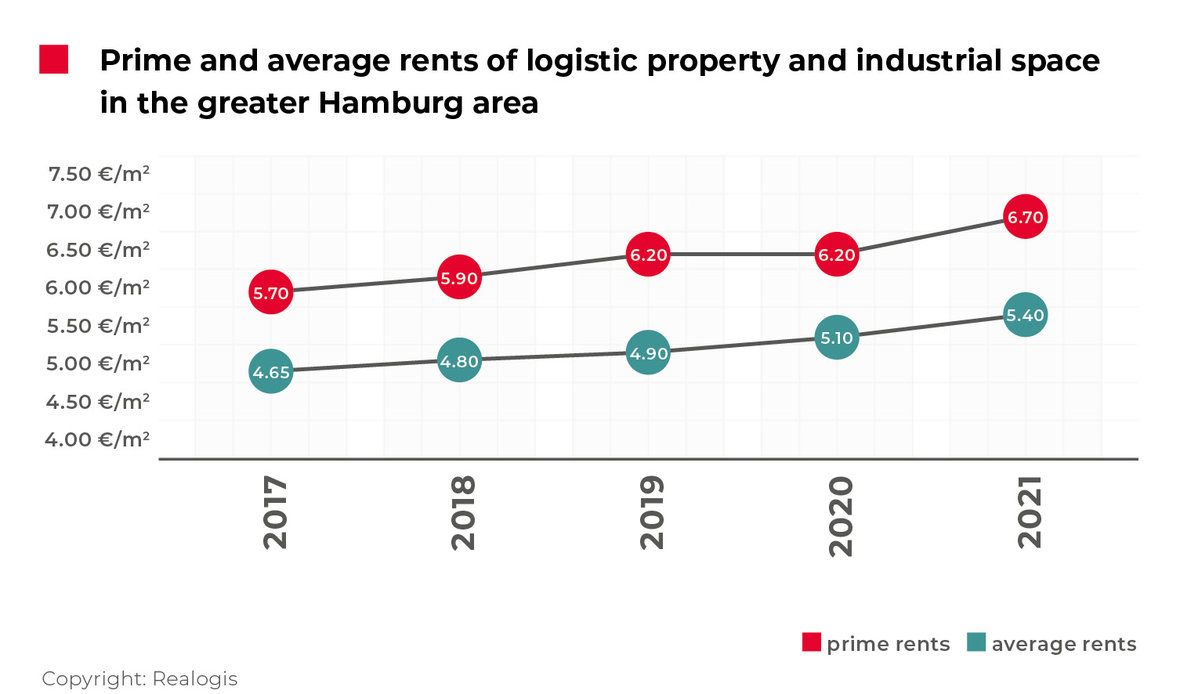

Significant rise in prime and average rents

Outlook for 2022: Sustained high demand, further rent appreciation, trend for two-storey logistics properties to continue, no large-scale sites until 2023

Lessors with highest take-up

Riess Ambiente, HH northern vicinity, approx. 40,000 m² (new build), Retail

Greiwing logistics for you, HH Port, approx. 28,000 m² (existing property), Logistics

Group7, HH East, approx. 26,000 m² (new build), Logistics

LFW GmbH, HH southern vicinity, approx. 20,000 m² (existing property), Retail

Ernst Pfaff GmbH, HH southern vicinity, approx. 17,500 m² (existing property), Logistics

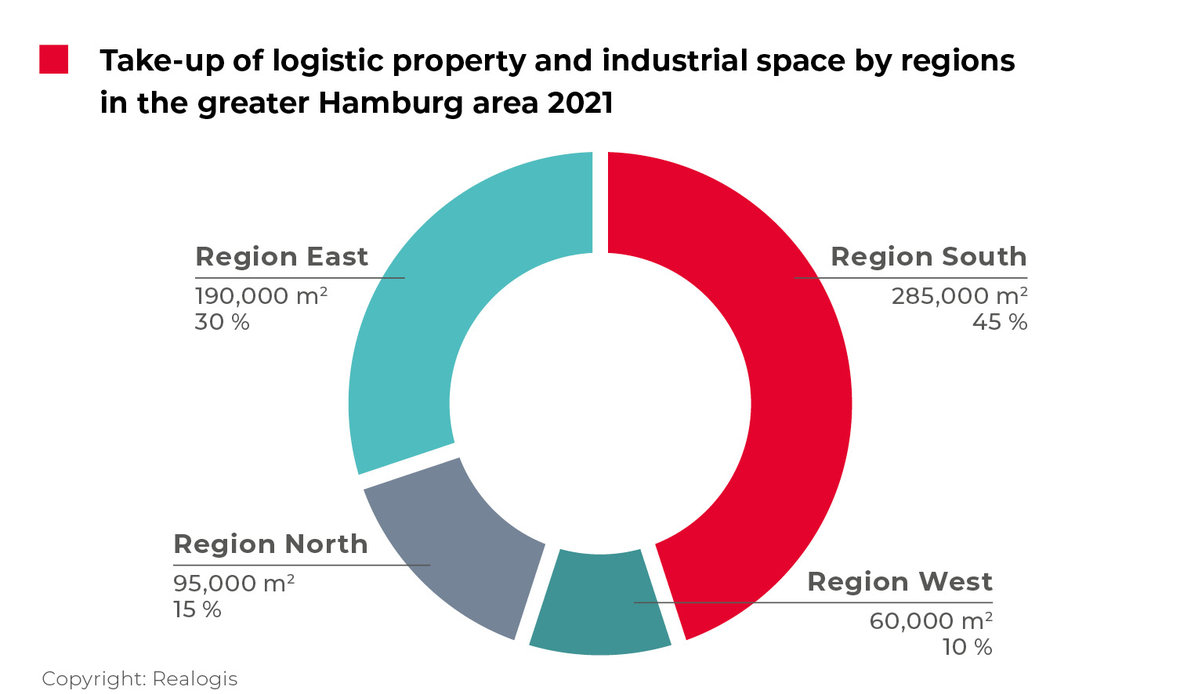

Southern Hamburg metropolitan area with two major deals

As in the previous year, the region with the highest take-up in 2021 was the southern Hamburg metropolitan area with a share of 45.2% or 285,000 m² (2020: 202,800 m², 39 %), meaning that it accounted for almost one in every two square metres brokered. The region increased its absolute take-up by 40.5% and recorded the highest growth among all regions in terms of market share (up 6.2 percentage points). With LFW in Winsen/ Luhe and Ernst Pfaff GmbH in Rade in the fourth quarter of 2021, two of the five biggest deals cumulatively contributed 37,500 m² to this result (13.2% of take-up in the region).

As in the previous year, the East region took second place with a share of 30.2% or 190,000 m² (2020: 34%, 176,800 m²). Although its take-up increased slightly by 7.5%, its market share declined by 3.8 percentage points. The only one of the five biggest deals to take place in this region was Group7 in the east of Hamburg.

Third place was again taken by the North region with a share of 15.1% or 95,000 m², compared with 20% and 104,000 m² in 2020. North saw the biggest downturn in market share of all regions at 4.9 percentage points, while absolute take-up was also down 8.7% on the previous year. The region would have fallen to last place without the major deal for 40,000 m² concluded by Riess Ambiente in the northern vicinity of Hamburg, which accounted for 42.1% of take-up in the region.

As in the previous year, last place was instead taken by the West region at 9.5% or 60,000 m², compared with 7% and 36,400 m² in 2020. The region increased its relative importance, with its market share rising by 2.5 percentage points and absolute take-up rising by 64.8%.

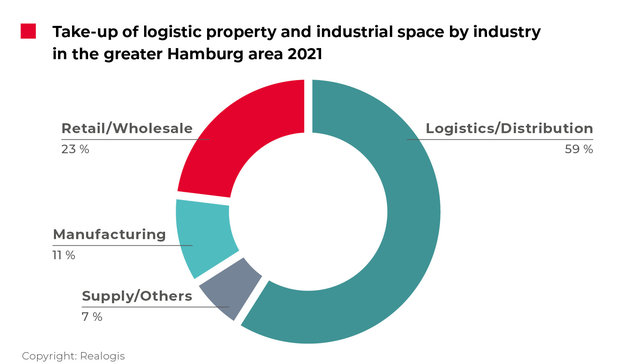

Logistics/ distribution sector doubles take-up

Having ranked second in the previous year, logistics/ distribution recorded strong growth to take top spot in the sector ranking with 59% or 371,700 m² (2020: 30%, 156,000 m²). This meant that take-up more than doubled compared with the previous year. In 2021, logistics/ distribution accounted for almost six in every ten square metres brokered. The sector saw by far the biggest increase in market share at 29 percentage points. Three of the top five deals – Greiwing logistics for you, Group7 and Ernst Pfaff – contributed to the extremely good result in this sector with cumulative take-up of 71,500 m² or 19%.

Last year’s leading sector, retail, took second place with 23% or 144,900 m² (2020: 38%, 197,600 m²). At 15 percentage points, it saw the biggest downturn in market share across all sectors. Absolute take-up in the retail sector declined by a substantial 26.7% year-on-year (from 197,600 m² to 133,400 m²) even though two of the five top deals were attributable to the sector, accounting for cumulative take-up of 60,000 m² (or 41% of take-up for the sector as a whole in 2021) – including the Riess Ambiente deal, which was the biggest in the past year.

Last place was again taken by the miscellaneous category “Other” with a share of 7% or 44,100 m² (down 5 percentage points; 2020: 12%, 62,400 m²).

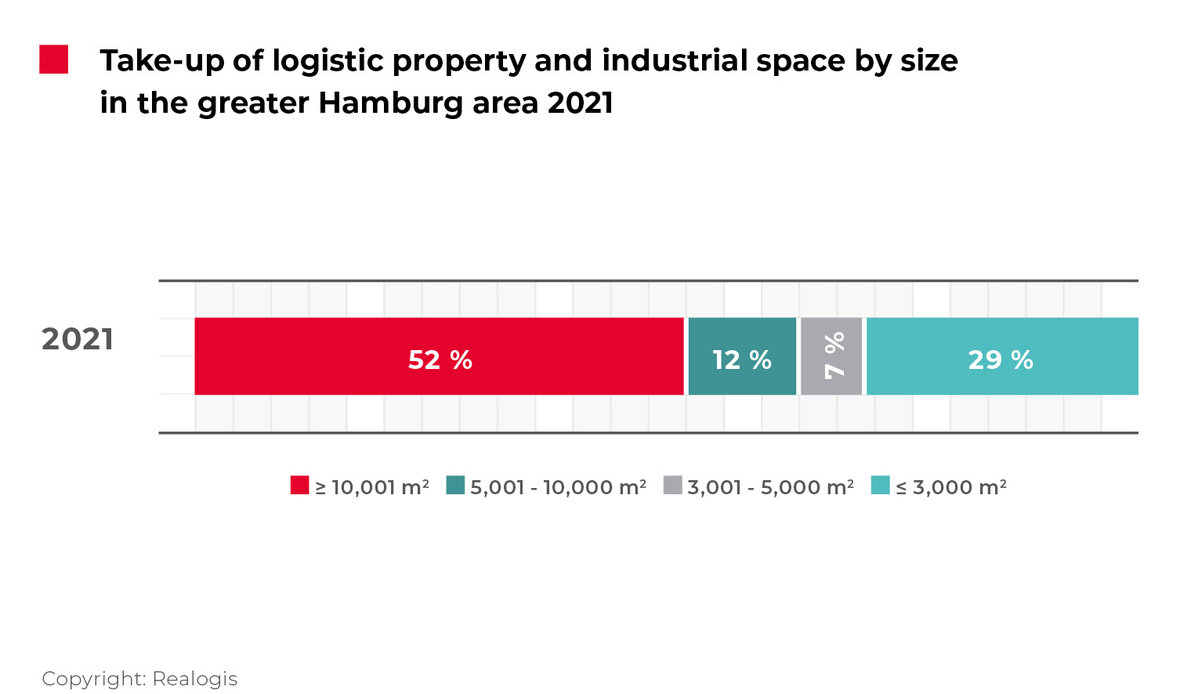

Large spaces of 10,000 m² or more account for half of take-up

As in the previous year, large spaces of 10,000 m² or more accounted for the biggest market share at 52% or 327,600 m² (2020: 57%, 296,400 m²). All five of the biggest deals took place in this category. With cumulative take-up of 131,500 m², they represented 40% of the result in this segment. Along with the next-smallest size category, spaces of 10,000 m² or more saw the biggest downturn in market share at 5 percentage points.

This might also be interesting for you:

To the market report Germany

Spaces of between 5,001 and 10,000 m² came in third at 12% or 75,600 m². Market share in this category also fell by 5 percentage points, having amounted to 17% or 88,400 m² in 2020.

As in the previous year, last place was taken by spaces of between 3,001 and 5,000 m², which accounted for market share of 7% or 44,100 m² (2020: 9%, 46,800 m²). The biggest winner was the smallest size category, spaces of 3,000 m² or below, which placed second in 2021 with market share of 29% or 182,700 m². This meant that market share in the category increased by 12 percentage points, while take-up doubled in absolute terms.

Significant rise in prime and average rents

Prime rent hit a new provisional high of EUR 6.70/m². With an increase of 8.1% compared with EUR 6.20/m² in 2020 and 2019, prime rent saw its biggest rise in the last five years and exceeded the five-year average of EUR 6.14/m² by 9.1%.

Average rent also climbed faster than at any other point in the past five years, rising by 5.9% to a new high of EUR 5.40/m² in 2021. This is 8.7% above the five-year average of EUR 4.97/m².

With demand from the logistics and retail sectors remaining strong and land prices and construction costs continuing to rise, we expect prime rent to see further growth over the coming months.

Outlook for 2022/2023

The trend towards a lessor’s market in Hamburg will continue in 2022. Tenants’ credit ratings will remain an extremely important factor for developers, particularly when it comes to the first-time occupation of new builds.

There is still almost no space with high suitability for third-party use and new-build quality available in the size category of 5,000 m² and larger. The next large-scale development projects are not expected to hit the Hamburg logistics market until 2023.

We anticipate sustained strong demand in the Hamburg market area in 2022 as well. However, the shortage of available products, particularly when it comes to spaces of 10,000 m² or more, means the 2021 result will not be repeated. We expect to see total take-up of around 500,000 m² across the year as a whole.

Furthermore, the trend for two-storey logistics properties is set to continue as a result of the broad unavailability of land near the city centre. High land prices coupled with increased construction costs are forcing developers to build upwards.

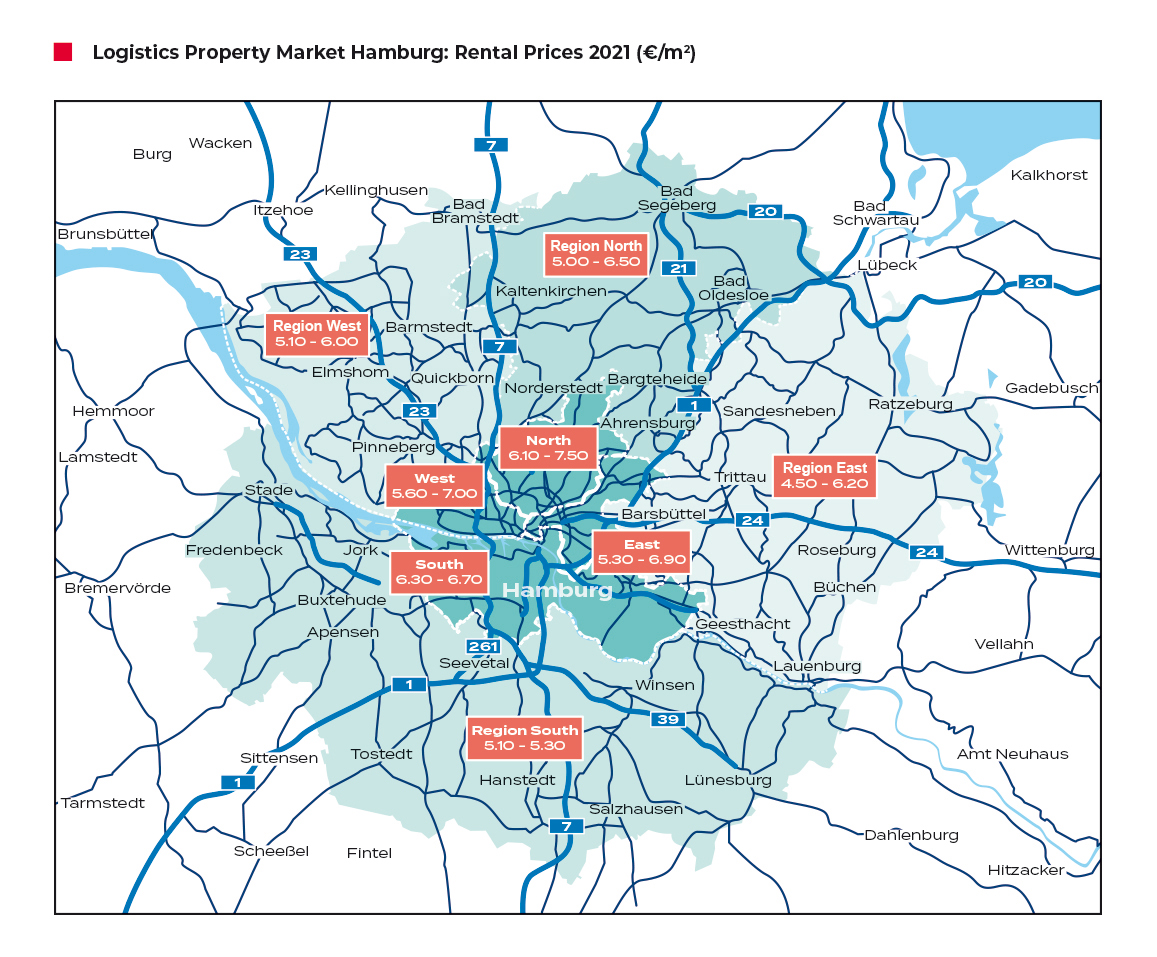

To the rent price maps:

Order the complete market report as PDF

Hamburg - 2021